Inside The Stock Market ...trends, cross-currents, and outlook

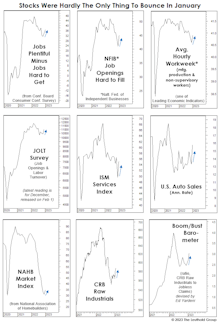

The Economy Rallied In January, Too

The narrative for January’s strong stock market bounce is that not all key economic releases looked to be forecasting a recession. However, one must consider that this was only true for coincident and lagging data series.

Is Good News Ultimately “Bad News?”

Let’s momentarily imagine that both the Index of Leading Economic Indicators and the yield curve “fail,” and a recession in 2023 is sidestepped. What might the GDP growth outlook be in that scenario? It wouldn’t be good, and (ironically) that’s because of strong labor market conditions on which the economic bulls now rest their case!

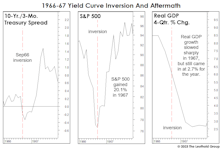

1966-67: When The Yield Curve “Failed”

Given the tendency of economists and strategists to dismiss the message of an inverted yield curve, it’s surprising there’s been no scrutiny of the “dog that didn’t bark”—the inversion of 1966. That’s the last time an inverted curve did not lead to a recession.

Valuations: What Bear Market?

If the October S&P 500 low holds, the normalized P/E ratio of 22.7x on that date will signify the priciest bear market bottom in history; in fact, it is exactly the same level reached as at the August-1987 bull market high. Since October, the normalized P/E multiple has grown to 25.5x—higher than all but three previous bull market peaks.

VLT Update

The progression of bullish technical evidence since October’s S&P 500 low is compelling, though not overwhelming. With that low now almost four months behind us, the VLT Momentum oscillator for the S&P 500 probably “should” have already triggered a new BUY signal. Yet, both the S&P 500 and NASDAQ Composite are still holding out.

Emerging Markets: Watching Closely

Foreign stocks have been leaders off last fall’s lows, but not by a big enough margin to flip our Emerging Market Allocation Model to a bullish stance. The model factored into our general avoidance of EM equities the last several years; now January’s action has us on alert that the outlook may soon shift.

In No Hurry To Nowhere

With the stock market horrors of 2022 already well-lamented by others, we tried hard to a come up with a longer-term, cheerier take on the recent state of things. We’ll confess... it was challenge.

A “Curve”-Ball We Didn’t See Coming...

Market veterans know there’s just one thing more probable than a recession after the yield curve inverts: Yield curve denial among a large group of sell-side economists and market strategists! Indeed, the earliest of those dismissals occurred last March—a month before the first of more than a dozen iterations of a yield curve inversion.

The Yield Curve And The Problem Of Timing

Frequently, there’s money to be made in the stock market in the months following the initial curve inversion. After the inversions of August 2006 and June 2019, the S&P 500 rallied another 23% and 19%, respectively, into its final bull market high. If this cycle plays out in textbook fashion, the business-cycle peak would arrive in September.

A One-Hundred-Year Market Echo

Hopes that this decade might see a repeat of the “Roaring Twenties” took a hit last year. But there’s plenty of time to recover, and bulls will be encouraged to learn that cumulative stock market performance for this decade, thus far, is better than at the same point in the Roaring 1920s.

A 2023 Forecast… From 1875!

Our grandmother mailed us the accompanying clipping from a Minneapolis newspaper when we entered the investment business in 1990—just as she’d done for our uncle when he became a securities analyst 20 years earlier.

VLT: “A Swing” And “A Miss”

We suspected November’s “low-risk” VLT Momentum BUY signal on the Dow Jones Industrials might turn out badly, and we were right: The Dow’s decline last month was enough to cause VLT to roll back over, which officially “rescinds” that signal.

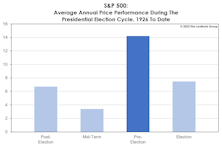

2023 Time Cycles: Two Outta Three Ain’t Bad

2022 was a nasty year for the stock market, but a wonderful one for market numerologists. This year is a different story. Two of the three calendar patterns are bullish, including the one in which we put the most stock (pun intended): The Presidential Election Cycle.

Another Misfire?

A signal from the newest addition to our Technical category seems to have gone awry. On November 30th, the percentage of S&P 500 stocks trading above their 50-day moving average topped 90%, thereby issuing the second “breadth-thrust” signal in four months.

2022 Asset Allocation Review

We’ve heard for eons that “Low bond yields justify high equity valuations.” Value-conscious investors might have described this conundrum another way: “Low future returns in one asset class justify low future returns in another.” (Mysteriously, only the first rendition became a CNBC catch-phrase.)

Calling “Bull” On Calls For A New Bull

Seriously, another “new bull”—coming so quickly after this summer’s “new bull?” We’ll see. We’re not ones to dismiss price action, because stock prices, in and of themselves, are an important “fundamental.”

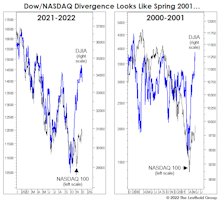

But we’ve seen the Dow go rogue like this once before, and it didn’t end well.

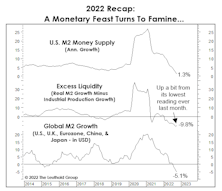

Illiquidity Rules The Day

Nearly everyone would cite high inflation as the dominant theme of 2022. But we think that the evaporation of a one-time ocean of liquidity better explains the horrendous backdrop for stocks and bonds. High inflation sped up the rate of evaporation, but it was going to occur anyway.

Don’t Trust The Thrust…

Jay Powell’s speech on November 30th triggered a 1,000-point intraday reversal on the DJIA and left us wondering who might have slipped the Chairman a recent copy of the Green Book.

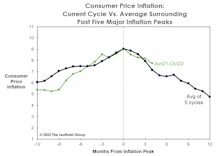

Goodbye Inflation, Hello Recession?

Unlike the five prior cycle peaks, this year’s inflation peak materialized during an ongoing economic expansion. That implies the “post-peak” monetary policy has never been tighter than today—making a soft landing even more improbable.

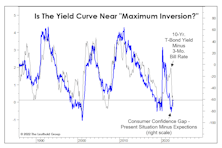

The Inversion Before The Inversion

We found the spread between the “Expectations” and “Present Situation” series (the “Confidence Gap”) has historically moved almost in lockstep with the yield curve. As the Confidence Gap plummeted throughout 2021, the implication was the yield curve would soon follow. After some initial resistance, it did.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue