Factors

Extreme Factor Dispersion

Dispersion remains elevated among factors, with growth selling off and momentum turning in extreme performance spreads. Low-volatility names finally did well after a long stretch of underperformance.

Factor Tilt Regime—October 2023

The dominating and overwhelming gains by the Magnificent Seven have made it nearly impossible for most traditional equity factors to excel. Only two styles have managed to surpass the S&P 500’s YTD return: Growth and Quality—and both have healthy exposures to the Magnificent Seven.

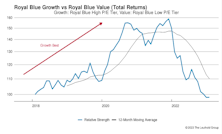

Growth vs. Value vs. Cyclicals

Both Growth and Value Small-Cap style boxes gained 10% in January’s rally. However, SC Growth remains well in the rearview mirror since its relative strength peak in September 2020: Small Cap Growth +8% versus Small Cap Value +60%.

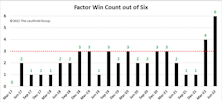

Factor Returns And A Basket Of EGGs

Equity factors are characteristics that have historically generated excess returns relative to the universe of stocks. However, in recent years factor returns have been underwhelming, causing investors to wonder if factors have become too popular, too crowded, or just plain obsolete. Then came the second quarter of 2022, when all six major factors outperformed the S&P 500, a feat only accomplished in four quarters over the last 27 years!

Research Preview: Factor Cyclicality

In Q2, all six major style factors outperformed the market. Those results are especially remarkable considering that factor excess returns the past few years have been underwhelming to the point that some investors began to wonder if they still work.

Factors Reverse Alongside Market

With equities rallying off bear market lows, factors also reversed during July. Except for Profitability, every factor category performed inversely to their year-to-date results. Momentum and Low Volatility were the biggest losers, while Growth was the biggest winner.

Tis The Season For Factor Tilting

Factor investing has gained wide popularity in recent years, enabled by a proliferation of smart-beta ETFs coming to market, which opened new opportunities for tactical investors. In 2018, we launched our Factor Tilt ETF strategy, and here we discuss how we’re now enhancing it by adding Seasonal Cyclicality to our analytical toolbox for evaluating factor conditions.

Factors: Ain’t Misbehavin’

Investment styles and factors are generally interpreted as having an inherent preference for either bullish or bearish market environments. The theoretical tilt of each style is based on its design and its sensitivity to economic, profit, and valuation cycles. However, theory and practice do not always agree, and we must look to actual performance to confirm our impressions.

Research Preview: Factor Standings For 2020

As we review factor and style returns for 2020, it occurs to us that the “whole” is much less interesting than the sum of its parts. Many factors are considered to be either bullish or bearish in temperament, and last year’s round-trip offers an opportunity to test the reliability of those characterizations.

Podcast #25 - Anything But Growth

Driven by massive government stimulus, an imminent vaccine rollout, and the expectation of record earnings in 2021, investors seem to be on the verge of embracing a move away from Large Cap Growth stocks in earnest. The leading candidates offered as broad-based alternatives to Large Growth (LG) include Value, Small Caps, and Emerging Markets.

Leuthold Factor Tilt Update

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Factor analysis is a point of emphasis in Leuthold’s tactical research activities, and this note summarizes our Factor Tilt outlook going into the fourth quarter. Factors are return drivers such as Value, Momentum, and Quality, and research has found that factor results vary over time—but that does not mean they are random.

Siege Protocol

This study examines the traditional protocol for bear markets to find which tactics worked as expected and which were caught misbehaving. Overall, we conclude that investors were not ready to commit to a full leadership rotation.

Factor Failure: Don’t Blame FANMAG

_Page_1.jpg?fit=fillmax&w=222&bg=FFFFFF)

Our recent commentary “1” For The Record Books noted that just one of seven S&P smart beta factors was able to outperform the S&P 500 last year, even though each style basket limits its holdings to constituents of the parent index.

“1” For The Record Books

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Dark energy makes up 68% of the universe, yet astrophysicists are having a devil of a time explaining what it is, why it is, or how it works. Quant investors are facing their own dark-energy mystery in understanding style returns of 2019.

The Case Of The Flipping Factors

Equity market themes have been boringly consistent of late; growth beating value, large beating small, and domestic beating international. In the factor world, Momentum and Low Volatility have been investor favorites for most of 2019 while Value resided in last place – the same old, same old. Then, something remarkable occurred on September 9th.

The Odd Couple

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The Momentum style—in which investors buy what has been going up recently—represents an optimistic, hopeful, “I’ll take some of that” mentality. The Low Volatility factor entails a pessimistic, fearful outlook in which investors want (or need) to stay invested in stocks but desire downside protection in case the market performs badly.

Horse Trading In The Factor Zoo

Smart beta ETFs have become an immensely popular investment tool, attracting billions of dollars in AUM by providing investors with targeted exposure to factors such as Value, Momentum and Quality. Characteristics such as these have been shown to generate alpha over time, and investors understandably wish to have focused positions in these return-generating styles.

Factor Trade-Offs

A major difficulty in picking stocks based on quant factors is the need to make trade-offs. A company that looks attractive on one preferred metric will likely look unattractive on another. This study examines the uncomfortable give-and-take that complicates factor investing at the stock level.

Factor Tilts at Mid-Year

_Page_1.jpg?fit=fillmax&w=222&bg=FFFFFF)

Factors provide investors with the ability to shift their portfolio’s characteristics to fit a particular economic and market outlook. Value might look appealing under one set of conditions while Quality might be more desirable in another. We developed a research platform that analyzes various drivers of factor returns, summarized in Exhibit 1.

Can Smart Analysts Generate Smart Beta?

We assess the effectiveness of using Wall Street analyst opinions as factors in a quantitative stock selection model. Watch for the full report coming next week.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue