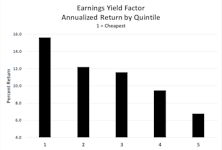

Factors

Factor Frontiers And Investing To The Max

Quantitative investing has taken the industry by storm over the last decade, and smart beta ETFs are pulling in billions of dollars as investors and advisors gravitate to this portfolio management technique.

Momentum Buyers: Beware

Momentum is a smart beta factor that gives investors excellent upside participation in rising markets. Most other smart beta factors are defensive plays, so Momentum is the place to be in strong upward moves. Momentum filled that role admirably in recent years, rising 56% from 2016 to the September top, compared to an average of +26% for the other major factors.

Styles And Factors DeFANGed

Social media, mobile computing, and digital life-in-the-cloud were the dominant storylines for U.S. stocks over the last five years—reaching the apex of popularity following the early-2016 market low.

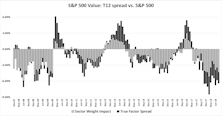

Factors And Sectors: A Curious Entanglement

Portfolio managers who tilt toward Value or Growth stocks have long known that each style carries with it an inherent bias toward some sectors and away from others. Our recent piece, Value Style’s 100-Year Flood, highlighted the significant role that sector weights (overweight Financials and Energy, underweight Technology) played in Value’s decade-long stretch of underperformance.

Research Preview: Sector-Adjusted Factor Returns

This article summarizes our current research into the interaction between factors and sectors. We find that sector weights have a significant influence on some factor results, while the true factor impact is the key driver for others. Watch for our full report coming next week.

EM Country Rotation Based On A Stock Factor Model

Back testing shows stock-level factor alpha can be captured at the country level. With the rapid growth of single-country ETFs, this may prove an efficient, practical alternative to individual stock selection.

The Ups and Downs of 2018

Ten weeks into 2018, we have already seen three mini-cycles in U.S. equities. A rip-roaring surge in January was followed in early February by one of the shortest corrections in history...

Leverage Factor: A Boost For High Quality Stocks?

A review of Quality factors, as well as the lower valuations of High Quality stocks, supports the current High Quality cycle amid rising market volatility. The Leverage factor may provide particularly strong backing for High Quality stocks.

Factor Mapping: The Final Piece Of The Puzzle

This months-long research effort culminates with this commentary as we lay out our thoughts on factor rotation and introduce The Leuthold Group’s recently launched Factor Tilt strategy.

Coming Attractions

With an abundance of year-end updates in this edition of Perception for the Professional, we plan to release the content for this “Of Special Interest” section separately in mid-January.

Sector Rotation: Momentum Versus Valuation Factor

For sector overweight/underweight decisions, applying a Momentum overweight with both EM and DM countries has been most successful.

The Case Of The Disappearing Value Premium

Market history teaches us that investors behave differently in groups than they do as individuals.

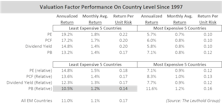

Valuation-Based Country Selection/Rotation

Despite cyclicality, over the longer term, investing in lower valuation countries ekes out better performance in an EM portfolio, and Dividend Yield showed the most consistency in terms of value factor effectiveness.

Momentum-Based Country Rotation: EM Vs. DM

Last month we assessed the effectiveness of using valuation factors as a basis for country allocation. Using 20 years of data, our results showed that they work quite well specifically for Emerging Market (EM) country-rotation, however, the same valuation-based strategy does not appear to be value-added for Developed Market (DM) allocation/rotation.

Valuation-Based Country Rotation: EM Vs. DM

Many studies have evaluated momentum factors for over/underweighting country exposures within a portfolio, but few have considered valuation factors for country rotation within the Emerging Market space.

July Factor Performance

With the exception of Low Volatility and Profitability, all other factor categories produced positive factor performance in July. The month was eventful, however, as Momentum produced a +4% spread through July 12th, only to give up more than half of that advantage as interest rates rolled back over.

Rotation From Info Tech To Financials Drives Factor Performance

Factors were impacted in June by: 1) Information Technology underperformance; 2) Financials’ renewed strength; and, 3) defensive and low volatility stocks lagging.

Dynamic Factor Investing: A Study In Value

Investment factors experience performance cycles just like every other asset and index. The Value factor is robust across definitions, as all eight versions produced positive excess returns under long/short and long-only methodologies.

The Intelligent Use Of Smart Beta

Quantitative investing has become an integral component of professional investment management, and smart beta funds have become popular vehicles for advisors as they assemble actively-managed client portfolios.

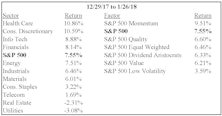

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue