Dollar

U.S. Dollar—Buy The Dip

The U.S. dollar has seen some interesting dynamics this year, so we’ve updated our U.S. Dollar Monitor. Currently, the model implies a higher likelihood of dollar strength, or at least a decent rebound over the next few months.

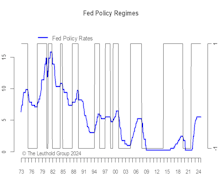

Anatomy Of An Easing Cycle

The economy normally fades heading into a series of rate cuts, with higher unemployment and lessening CPI inflation. Risky assets (stocks and credit) do well, and bond yields move lower. Real assets also benefit (gold in particular). On the whole, an easing cycle is favorable for most assets.

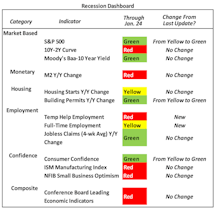

Three Key Themes To Watch—Recession, Inflation & The Dollar

The probability of a soft landing has materially increased, while stronger than expected growth is likely to put a floor on inflation, which challenges the consensus disinflation view. A refresh of our Dollar Monitor suggests a weaker dollar going forward.

Tactical Tools For A Stronger Dollar

The 2022 bear market has been driven by collapsing valuation multiples, particularly for expensive growth stocks and unprofitable companies. Coming into the year, U.S. stocks stood as one of the most egregiously valued equity markets around the world, motivating investors to look elsewhere for more reasonably priced alternatives. Fortunately, international stock markets offered much better valuations that could serve as havens from the coming U.S. valuation collapse. Unfortunately, the strategy of seeking refuge in moderately priced foreign markets was foiled by an unusually strong U.S. dollar, leading us to take a closer look at how moves in the USD affect investment outcomes for domestic investors.

Research Preview: Returns In A Year Of Dollar Strength

The U.S. Dollar Index (DXY) has gained 16.2% YTD, its best performance in almost 40 years. However, a strong dollar is bad for those with international investments, as returns are slashed when translated back into dollars.

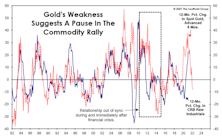

Gold: Still A Useful Dollar Hedge

A stronger U.S. dollar is “supposed” to be bearish for commodities, but it’s been a banner year for most commodities with gold among the few that are down on the year. However, keep in mind that gold tends to be a harbinger of major moves in industrial commodities, with a lead time of about six months—and its year-over-year change is now negative.

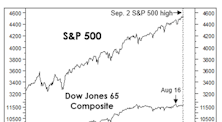

The Stock Market IS A “Fundamental”

The impact of U.S. stock-market “hegemony” extends far beyond currency markets. We believe the mania has progressed to the point where the stock market itself will shape the intermediate-term and even long-term fortunes of the U.S. economy more than it ever has before.

Triggered!?

In recent months, we’ve highlighted some reasons to buy or add to Emerging Market equities, and at year-end received a formal endorsement from our monthly Emerging Market Allocation Model. The signal triggered after a 30-month period in which the model recommended the relative “safety” of the S&P 500—in retrospect, a good call.

Textual Analysis Of Fed Statements—Always Artificial, Sometimes Intelligent

We geek it up a notch and use some of the popular text-processing techniques to quantify the hawkish/dovish sentiment of the latest Fed statement. Some human “coaching” is needed in every step of the process (hence the “artificial” part). But when these tools are used properly for carefully chosen tasks, they can be quite intelligent.

How Much For Your “Free Lunch?”

The 41% S&P 500 rally would be half as large if measured in terms of gold, and a “unit” of the S&P 500 now buys 70% fewer ounces of gold than it did in early 2000. Meanwhile, when denominated in either silver or Bitcoin, the stock market rally has been almost nonexistent.

Keep An Eye On What Your Stocks Will Buy

.jpg?fit=fillmax&w=222&bg=FFFFFF)

News that the Bureau of Labor Statistics may have undercounted the May unemployment rate by six percentage points should remind investors of the danger of taking government economic reports too seriously. Regardless of the figure, though, unemployment is no doubt near its peak for the downturn.

The Decade Of U.S. Exceptionalism & The Year Ahead

Two words sum up the past decade pretty nicely: U.S. Exceptionalism. The superiority of U.S. assets really comes down to the unique combination of growth (U.S. stocks), yield (U.S. bonds), and relative safety (both U.S. stocks and bonds).

1987 Parallels (Part 2)

At the risk of yelling “fire” in a crowded theater, we present a few parallels between recent action and the year leading up to the October 1987 crash.

A Crude Catalyst?

The great mystery behind the trade-weighted dollar’s nearly-10% YTD decline is that it’s failed to fuel further gains (or any gains) in commodity prices in 2017.

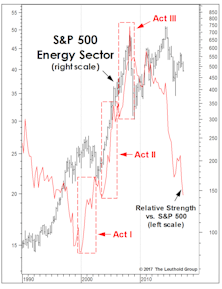

Energy: Too Early To Bottom Fish

The gap between crude oil prices and Energy sector RS is now much wider than seen even at that historic 2014 juncture. The “divergent” weakness in Energy stocks suggests that crude will likely trade lower.

Grappling With A Strong U.S. Dollar Outlook

.png?fit=fillmax&w=222&bg=FFFFFF)

Profitable investing overseas requires not one, but two, successful decisions: 1) select an outperforming asset class; and, 2) be in a currency that provides a favorable foreign exchange impact.

Trump Trade—Pause Before More Gain

The market seemed hesitant to push the Trump trade any farther as new policies have focused on trade renegotiation and immigration, the less positive part of the policy package.

Can The Dollar Save Small Caps?

The dollar’s moonshot in recent months has resuscitated a stock market leadership argument we haven’t heard for a long time.

U.S. Versus Foreign Stocks: More Of The Same

Long before the U.S. dollar began to rebound, the current bull market in global stocks had already favored “provincial” portfolio managers focusing solely on U.S. stocks.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue