Market Action

Powell’s Dovish Accomplice

.zip.jpg?fit=fillmax&w=222&bg=FFFFFF)

Last week we argued that U.S. money growth remains way too high to reasonably expect a peak in consumer price inflation during the next few months. At the peaks of the last five bouts of inflation of 5% or more, real growth in the M2 money supply had turned negative in four cases and had slipped to less than 1% in the other one. Today, real M2 is growing at nearly a 7% rate.

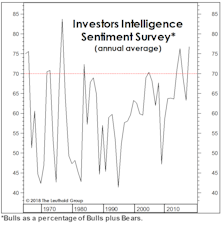

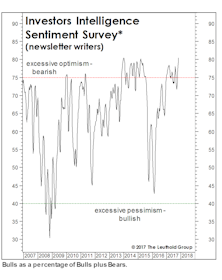

A Long-Term Take On Sentiment

We impatiently published this study two months ago instead of properly waiting for full-year numbers.

A Longer-Term Take On Sentiment

Stock market bears had a field day when the latest Investors Intelligence sentiment survey (Chart 1) saw the percentage of bullish newsletter writers spike to its “highest level since 1987.”

Lack Of Confidence Has Been Greatly Exaggerated

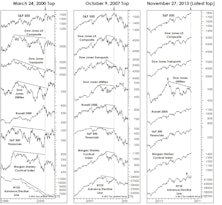

While this 7 1/2-year bull market has failed to give rise to anything resembling the equity culture of the late 1990s, we think it’s a stretch to claim—as dozens of commentators over the past five years have—that this bull is “the most hated” in history.

Fed Watching For The 21st Century

Deteriorating stock market breadth and worrisome leadership trends both suggest liquidity has already tightened; whether the Fed follows suit in September may now be just a formality.

A Page For The Bulls

One could conceivably argue the market is still “cohesive” enough to hold together for awhile longer. June 23rd saw closing bull market highs in the NASDAQ, Mid Caps, Small Caps (both the S&P 600 and Russell 2000), and the critical KBW Bank and NYSE Arca Broker/Dealer Indexes.

Another Upleg?

The stock market generated enough positive evidence by the second week of February to knock us from our comfortable perch on the fence. We covered a portion of our equity hedges on February 12th, bringing net equity exposure in the Core and Global Funds up to 58% from the 50% level that had prevailed since November.

Stuck In Neutral?

Extreme market viewpoints get the headlines, but it’s baked into our disciplines that we will (occasionally) be noncommittal.

Stock Market Observations

Market gains have been less broad than in 2012 and 2013; market direction and leadership have been mismatched; and quantitative factors have been choppy.

A Quick Technical Take

If a bear market is imminent, it will unfold with less “internal” forewarning than any cyclical decline since the late 1930s.

Stay Bullish

It’s April once again… Are we due for yet another market top? Some perspectives on the possibility of attaining a new all-time market high in the current cyclical bull, and what may drive the upside.

Stock Market Observations

Under the “principle of alternation”—in which price patterns vary from cycle to cycle for the sole purpose of fooling market participants—the bull market is (in my view) unlikely to top out in the spring or winter of 2012.

Markets (Mostly) In Gear

Market in gear, with almost all market indices hitting new highs in tandem. Would be unusual for a market correction with this type of uniformity.

A Mid-Term Exam: What The Upcoming Elections Could Mean For The Stock Market

Prompted by a client request, Eric Bjorgen examines the impact of mid-term elections on the stock market.

Stocks And Economy Joined At The Hip… For Now

Economic indicators are hypersensitive to even small changes in the data, and investors are hypersensitive to the indicators themselves.

2009: Not Monotony, But Close

The 2008 worst performers shot to the head of the class in 2009. History however shows it doesn’t usually pay to buy the prior year’s laggards in hopes of hitting it big the next year.

January Market Action

Uncertainties are running high, and the stock market continues its struggle with a complex array of cross currents.

December Market Action

2008 is over. We expect 2009 to be better since worst-case scenarios now seem less likely to play out.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue