Interest Rates

How Much Slack?

By now it’s consensus that the Fed missed the ideal window for the first rate hike (if one ever existed) by at least a year and a half. We don’t disagree…

Fed Tightening: The Two-Year Anniversary?

We’ve long argued that this tightening cycle began in January 2014, the month of the first of seven tapering moves which occurred through October of that year. There’s both economic and market evidence to back up this claim.

2016 Time Cycle—Not Likely To Be A Typical Year

The 2016 pattern looks good on paper, but if the excitement in the first week of the year is any indication, we highly doubt 2016 will turn out to be another typical election year.

Three Questions & One Answer: From Divergence To Convergence

1) Why The Big Sell-Off In Stocks? 2) Why Didn’t Interest Rates Go Lower? 3) Why Was The Dollar Weaker?

Interest Rates And Credits: At A Crossroads

The U.S. 10-year yield looks ready to re-test the ceiling of the previous downtrend...The recent weakness in oil prices brought back some very unpleasant memories from 2014. Implications for breakeven rates and credits are not so sanguine...We are at a crossroads and a cautious stance is warranted.

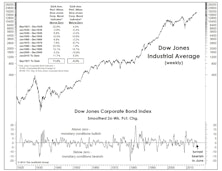

A Venerable Monetary Indicator Turned Negative

The smoothed, 26-week rate-of-change in the DJ Corporate Bond Index, a reliable indicator of monetary conditions over many different market and economic cycles, turned negative in mid-June.

Navigating The First Rate Hike

Our current view is the lift-off will be December or later. Assuming inflation will pick up and the Fed hikes the rate by the end of 2015, stocks will perform relatively well, with international stocks a better bet than U.S. stocks.

Don’t Fight The Fed?

While our stock market disciplines (including the Major Trend Index) are nominally bullish, we’re mentally gearing up to do something in the near future that was once considered ill-advised: Fighting the Fed.

U.S. Interest Rates & Credits—Keep An Open Mind

The ease with which the 10-year yield broke the strong 185 bps barrier was simply too hard to ignore. This tells us interest rates will likely go lower before going higher. The current active range is 140-185.

U.S. Interest Rates And Credits—Expect The Unexpected

We expect much higher volatility in interest rates this year as the market grapples with the prospect and timing of the Fed’s first rate hike. Our base case is for the Fed to raise rates in the third quarter. There are various reasons for the Fed to be patient. Inflation will be the biggest one. The threat of oil-related risk contagion is certainly real. We are concerned that equities have not fully priced in this threat.

Interest Rates & Currencies: It’s Complicated

The recent sudden strength in the dollar is mostly attributable to the divergent central bank policies. This supports a bullish dollar outlook over the medium term.

10-Year Yield: More Downside

We expect the 245-250 barrier to be tested, and if it is decisively broken, much lower yields could be in the cards.

Data Dependency—September Taper Still Likely

More upside surprises are still likely and, despite the disappointing jobs report, the overall economic picture still supports a September taper. The improving economic picture is not just happening within the U.S., but in other major countries. We still believe the upside for the U.S. 10-year is limited.

The Dollar: Upside Limited In The Near Term

A closer look at the dollar’s two main counterparts, the euro and the yen, reveals a regime shift in both cases, but for different reasons.

10-Year: Taper the Taper—Upside Limited

If interest rates keep going higher from here, we would run the risk of derailing a still-fragile recovery. As long as the Fed tapering uncertainty exists, we expect higher volatility on the 10-year yield to persist in the mean time.

Rising Stocks And Rising Rates: It’s Not Uncommon

Today may feel different, but it isn’t. The past 13 months’ trading action in the U.S. is the second example of this phenomenon in the current (2009-to-date) cyclical bull market. We focus on 11 previous episodes for perspective. Plus we clarify recent thoughts on interest rates and stock market valuations.

Timing The “Taper”

The new debate over the QE “taper” erupted at the same time that a long-reliable Fed-tracking tool is telling us it’s time to ease.

Of Special Interest: Valuing The Stock Market - Do Interest Rates Matter?

Models based on so-called relative valuations have a poor track record in practice, having misled investors at several historic inflection points. Interest rates have virtually no impact on stock market valuations, but they may have transitory effects on stocks in the short term.

The State Of Interest Rates

We think interest rates will stay low for an extended period of time, so the key question is, when will rates start rising?

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue