Inside The Stock Market ...trends, cross-currents, and outlook

Too Early For Curve Watching?

Last month, we published a table showing where we thought a variety of economic and financial-market measures lay along the economic recovery “continuum.” Although the upturn has officially entered just its 22nd month, the bulk of those measures looked “late cycle” in nature.

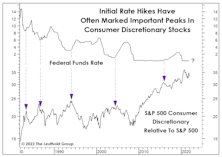

Danger For Discretionary?

It’s been so long since investors have faced a serious Fed tightening episode that they may have forgotten a helpful rule of thumb: An initial hike in the fed funds rate is usually a good excuse to dump some Consumer Discretionary stocks.

Still An Uptrend… According To This

In an effort to manage stock market risk, we monitor reams of data relating to the economy, earnings, Fed policy, and investor sentiment, along with technical indicators of all stripes. But for the rare occasions when upside price action seems practically uncapped, it’s hard to beat pure price action if one is inclined to play along.

Beware The Hot Air...

Mask mandates are back in vogue, and it’s investors who should be the first to welcome them: They’ll protect us from January’s blast of “thermal pollution,” when Wall Street prognosticators expel large volumes of hot air with prophesies for the new year. We have no problem with the exercise—so long as full-year forecasts (including one’s own) aren’t taken too seriously. “Forecasts are for show,” Steve Leuthold would always say.

Weigh Those Bags Before Checkout

You’ve likely heard of “shrinkflation,” the practice in which a package of M&M’s is reduced from 40 pieces to 32, while the price per bag is unchanged. Publicly-traded companies have been engaged in similar schemes for awhile.

A Dose Of Hindsight For 2022...

Speaking ill of the NASDAQ is like taunting Tom Brady; it’s hard to remember a good outcome. Still, we must dutifully report a new finding that QQQ owners won’t like.

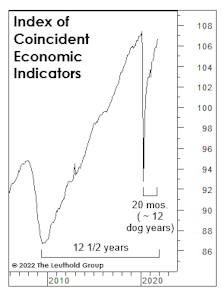

Carbon-Dating The Recovery

If January is the 21st month of the recovery, then time has elapsed in “dog years.” And that might put this “canine” recovery at around 12 years—just shy of where we might be had COVID never occurred!

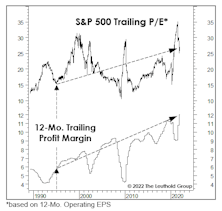

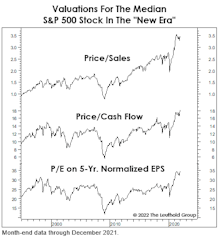

New-Era Profits, New-Era P/E Multiples

The current mania won’t last forever. But our use of the “New Era” label in describing the last-quarter century or so of stock-market dynamics is still useful—in part because it highlights fundamental developments that simply cannot be repeated indefinitely.

Fat Profit Margins? Thank Your Grandkids!

Future generations are now footing the bill, not only for today’s entitlement recipients, but for record corporate profits as well! (Consider a gift of QQQ shares to help them pay for it all.)

Even “True Believers” Should Read This

Consider it a sign of the times: Here is the most bullishly slanted version of our “Estimating The Downside” exercise we’ve ever put in print (and likely ever will).

Time Cycles Say There’ll Be Better Times Than 2022

Numerologists will be disappointed to learn that longer-term time cycles don’t line up for a prosperous 2022 for stocks. However, the historical “hit rates” aren’t high enough to justify running for cover if you have no other fundamental stock-market worries.

The “Star” Is Not Aligned For 2022

When we entered the business in 1990, our grandmother mailed us a decades-old clipping from a Minneapolis newspaper featuring a columnist’s cryptic take on a hand-rendered chart. He coyly claimed to have found it in “an old desk”—and it wasn’t until the internet age that we’d learn of its unattributed source.

A Squandered Small-Cap Opportunity?

We know our view on this is controversial, but we like the relative prospects for Small Caps—even though we still believe the broad stock market is currently the most speculative one in U.S. history.

Asset Allocation: A Rising Tide Lifts Most Boats

Boy, we thought policymakers had thrown the kitchen sink at the economy in 2020. Evidently, the Fed’s Marriner Eccles building has two kitchens, because they were able to do it again in 2021: M2 grew 13%, the Fed’s balance sheet swelled19%, and the 2021 federal deficit will come in at 12% of GDP.

Rewarding “Perfect Foresight”

Remember, the All Asset No Authority Portfolio assumes complete naïveté on the part of the portfolio manager. That’s one extreme of the asset allocation continuum—although few allocators would admit that such an approach might be viable, despite its respectable history.

Momentum: Not Just For Stock Pickers

For those not blessed with clairvoyance, we’ve developed an asset selection strategy that’s done very well, historically, compared to the “naïve” AANA Portfolio and even against the almighty S&P 500. We’re not implying that investors dump their valuation models, economic forecasts, or their intuition. But they should recognize that price momentum tends to persist—not just among stocks and industry groups—but at the asset-class level as well.

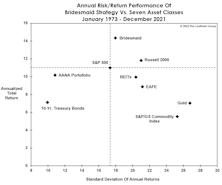

Bridesmaid Strategy Risk/Reward

The “risk-adjusted returns” concept faded further into obscurity in 2021, with the year’s largest drawdown in the S&P 500 a mere -5.2%. But for those who still care about risk, the Bridesmaid strategy—though it often holds highly-volatile stuff like Gold, Commodities, and Small Caps—has been only about 1% more volatile than the S&P 500.

Bridesmaid Track Record

Overall, five of the seven assets available for the Bridesmaid strategy have underperformed the S&P 500 over the long-term, and three (Treasury Bonds, Gold, and Commodities) lagged by 390 basis points or more per year.

Bridesmaid Strategy For Equity Managers

Once again, the idea is to dispense with macroeconomic trends, sector fundamentals, comparative valuations, and to base sector selection solely on the prior year’s total returns.

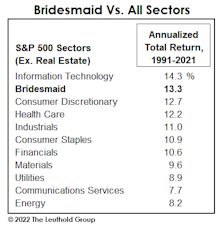

Bridesmaid Sector Track Record

As noted, the Bridesmaid sector strategy has underperformed what has become a more difficult benchmark in five of the last six years. Those poor results have cut the annualized excess return of this approach to just +2.1% since 1991.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue