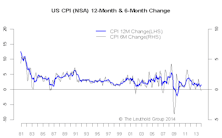

CPI

Twisty Curves

The short end of the yield curve sold-off to price in an earlier-than-expected rate hike, while the long end rallied as the prospect of tightening reduced longer-term inflation expectations.

Have We Seen This Post-QE Movie Before? It’s Still Too Early To Call

We looked at the periods around the end of the three previous easing programs (QE1, QE2 and Operation Twist) and compared those patterns with the current ones for various measures. The current patterns from both an economic and a market front bear enough resemblance to the previous ones to make us a bit uncomfortable. February’s market action was encouraging, but it is still too early to rule out a post-QE fizzle.

Inflation Pressure Anemic

Inflation measures are broadly in line with expectations, and overall inflation pressure is anemic. We maintain our view that inflation will be a non-factor in the first half of 2014, and it might increase moderately in the second half. Inflation on the producers’ level is weak, too and the PPI inflation pipeline doesn’t seem to pose any immediate inflationary threat either.

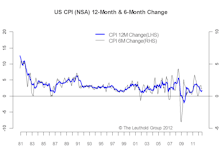

Inflation Lower Still

We maintain our view that inflation will be a non-factor for the next six months but will increase moderately in the following six months.

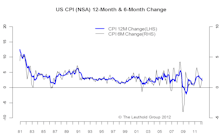

Inflation Still Going Nowhere In The U.S.

Inflation at both consumers’ and producers’ level is still modest. A drawn out government shutdown and debt ceiling debate will hurt the economy, which could further push out the taper timeline.

10-Year: Taper the Taper—Upside Limited

If interest rates keep going higher from here, we would run the risk of derailing a still-fragile recovery. As long as the Fed tapering uncertainty exists, we expect higher volatility on the 10-year yield to persist in the mean time.

"Muddle Through"

The global economy is stuck in a “muddle through” mode with developed and emerging countries showing divergence in terms of leading indicators. Despite this divergence, they share one thing in common: an upturn in inflation. How much more room there is for easing is a key determinant of asset market performance.

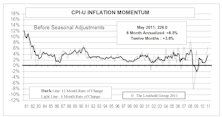

Inflation Slightly Lower Than Expected

The non-seasonally adjusted CPI fell 0.5% from October to November, lower than expected.

No Big Change — Inflation Remains Moderate

The non-seasonally adjusted CPI was essentially flat in October, in line with market expectations.

Inflation Turned Higher In August

The non-seasonally adjusted CPI jumped 0.6% in August, matching the market consensus.

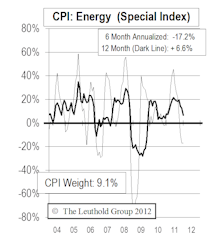

CPI Inflation Dips Lower, But Concerns About Food & Energy Prices Remain

Inflation measures mostly lower than expected in July.

Inflation Pressures Trend Lower

Inflation measures mostly matched expectations in June.

Near Term Inflation Presures Receding

Most inflation measures matched expectations in April.

Inflation Still Below Fed’s Target, Near Term Pressure Is Moderate

Inflation is still below the Fed’s target and near term pressure is only moderate. This gives the Fed some room to ease further if the economy falters.

Falling Commodity Prices Tamping Down Inflation Pressures

Through November, the CPI is now up 3.4% from year ago levels, while the PPI is up 5.7%.

Reported Inflation Should Be Muted In 2012

For 2012, the reported CPI is expected to slip down to the +2% area (although items like lunches, transportation, parking and food may continue rising at close to a 10% rate).

Very Little Price Pressure At Present

It is very difficult to find signs of accelerating inflation in today’s markets.

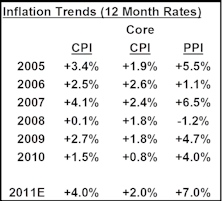

Inflation Pressures Waning

While our 2011 year end inflation projections are still well above the 2010 year end levels, it seems that both the CPI and PPI may have already peaked for the year.

Jumped The Gun With Boost To PPI Estimate

The July reports showed that both PPI and CPI edged downward in June from May readings.

Inflation Pressures Continuing To Heat Up...Boosted Year End Projections

CPI rose 0.5% in May (before seasonal adjustments), down from April’s +0.6% monthly increase.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue