CPI

Inflation Watch

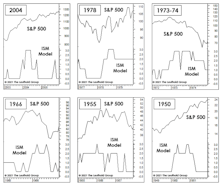

April ISM readings, both for Manufacturing and Services, were hot across the board. That’s good news for a still-recovering Main Street, but it manifested in ways that have frequently caused problems for a famous Street located in Lower Manhattan.

Still Heating Up…

The Fed’s reflationary efforts are showing up everywhere except in the measure that’s engineered specifically to minimize them—the Consumer Price Index. It’s a virtuous circle, until it is not

A 40-Year Inflationary Echo

When measured by the gains in stocks, gold, and house prices, there has been just one other occasion in which asset inflation was as “broad” as today—late 1980. But the differences in underlying fundamentals between then and now couldn’t be more stark.

The Rotation Should Hardly Be A “Surprise”

.jpg?fit=fillmax&w=222&bg=FFFFFF)

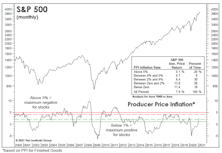

Consumer Price Inflation of 1.2% for the twelve months through October remains way below the Fed’s long-time 2% objective, which is nothing new. But a first step in getting inflation to eventually run a little bit “hot” (the Fed’s new objective) is to break the long-term disinflationary psychology among consumers and investors, and that is clearly happening. In fact, based on the excellent “Inflation Surprise” Indexes published monthly by Citi, the U.S. is now the world’s inflationary hotspot!

Keep An Eye On What Your Stocks Will Buy

.jpg?fit=fillmax&w=222&bg=FFFFFF)

News that the Bureau of Labor Statistics may have undercounted the May unemployment rate by six percentage points should remind investors of the danger of taking government economic reports too seriously. Regardless of the figure, though, unemployment is no doubt near its peak for the downturn.

Stocks Just Delivered A Strong Deflationary Impulse

Investors have just suffered a negative wealth effect that will likely work to tamp down inflation over the next year.

Inflation—Another Small Miss

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The latest CPI numbers missed market expectations. The problem is not with the actual CPI numbers, but merely the fact that market expectations are still a tad too high. More disconcerting is the cool trend in housing inflation.

Keep An Eye On “Relative” Inflation

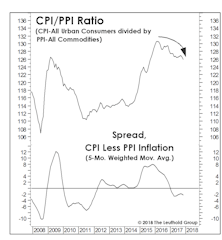

While our Group Selection (GS) framework hasn’t yet warmed up to commodity-oriented industries, our macro work suggests perhaps it should.

Inflation-As Flat As The Yield Curve

The latest Core CPI number disappointed again. The divergence between inflation break-evens and the yield curve is puzzling. Given the lack of inflationary pressure and the Fed’s projected rate path, it would not surprise us to see a flatter curve without the help of fiscal stimulus in the next few months.

Inflation-Yield Curve Too Flat

The latest CPI numbers are in-line with expectations. The divergence between inflation break-evens and the yield curve is worth close monitoring. Given that the global recovery is still intact, we don’t think the current inflation picture justifies the flatness of the yield curve.

Inflation - Goldilocks Still Intact

The latest CPI numbers missed expectations but we consider it a passable reading.

Spoiler Alert! The Bond Bear Is Already Here...

Bond investors residing in the Lower For Longer© camp no doubt feel vindicated by the summer rally that’s taken yields on 10-year Treasury bonds to as low as 2.06% in early September.

CPI Weakness Is Broad-Based

The CPI numbers have disappointed five months in a row. The real bad news for inflation hawks is that the weakness in core CPI is broad-based. There is hope for inflation to stem its recent weakening trend soon as the Chinese CPI has already stabilized and started to turn up.

Inflation Slip Sliding Away

Temporary and transitory? The CPI numbers have come in below estimates four months in a row.

Inflation Disappoints Again

The CPI numbers have disappointed three months in a row. Weak commodity prices do not inspire higher inflation expectations. The global scope of inflation deceleration adds more weight to the recent soft readings. However, lower bond yields relative to nominal growth rate is inflationary and buffers the impact of weak inflation and rate hikes.

Inflation Subpar Again

The latest CPI numbers are slightly weaker than expected. We think expectations for higher inflation are still on the high side. The global scope of inflation deceleration adds more weight to the recent soft readings. Patience is the right approach for the reflation trade at this point.

Inflation-Weaker Sooner Than Expected

The latest CPI is weaker and the softness was sooner than we expected. More alarming is the recent broad-based deterioration in economic data. Lower inflation expectations have flattened the yield curve recently, which hurt Financial stocks. We believe inflation has likely peaked for the time being and patience is the right approach for the reflation trade at this point.

A Dovish Hike--Positive For Inflation

The dovish rate hike is a positive for inflation and credit. A hawkish message right now would have been quite detrimental and self-defeating in terms of realizing two more hikes later this year. We believe achieving sustained 2-3% inflation could be harder than most people expect going forward. Overall, we are encouraged by the dovish hike but we think the real test for inflation is when the base effect starts to wane.

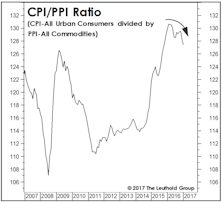

Lo And Behold, Another RATIO!!

For managers who must remain fully invested in equities (or “paid to play,” as we’ve often called it), the level of inflation might prove a less important consideration than its character.

Inflation-All About That Base

CPI numbers were strong and better than expected. A big part of the recent upturn in inflation has to do with the much lower base from a year ago. We are seeing upside inflation surprises on a global basis but wage inflation is still disappointing. We are encouraged by the general uptrend in inflation data but we think the real test comes after the positive base effect subsides.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue