Articles by Chun Wang Director of Multi-Asset Strategies

Risk Aversion Index—Fell Sharply But Stayed On “Higher Risk” Signal

We are leaning towards a more favorable outcome for risky assets but staying alert.

U.S. Interest Rates & Credits—Keep An Open Mind

The ease with which the 10-year yield broke the strong 185 bps barrier was simply too hard to ignore. This tells us interest rates will likely go lower before going higher. The current active range is 140-185.

EU QE - Success Highly Uncertain

We rely on past experiences in Japan, the U.K., and the U.S. to give us clues about the future path of the EU QE.

Risk Aversion Index—Stays On “Higher Risk” Signal

The market is at a critical juncture with oil-related assets very oversold while equities are holding near all-time highs.

Inflation—More Weakness Before It’s Over

We expect the downward pressure on inflation to persist in the next few months. But we think the recent sell-off in all inflation-related assets is a bit over done, however, we will exercise patience to wait for clearer signals. The NFIB actual and future compensation survey continue to offer glimmers of hope. Inflation at producers’ level has more downside too in the near future.

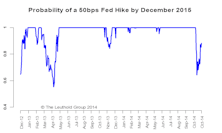

U.S. Interest Rates And Credits—Expect The Unexpected

We expect much higher volatility in interest rates this year as the market grapples with the prospect and timing of the Fed’s first rate hike. Our base case is for the Fed to raise rates in the third quarter. There are various reasons for the Fed to be patient. Inflation will be the biggest one. The threat of oil-related risk contagion is certainly real. We are concerned that equities have not fully priced in this threat.

2015 Time Cycle—Giving The Bull The Benefit Of The Doubt?

We are again impressed by the pattern’s predictive ability as most equity markets tracked their respective patterns quite well in 2014. Another banner year seems to be in store for the S&P 500. The exceptionally favorable pre-election year is the main reason, but we cannot be too complacent.

Risk Aversion Index—New Higher Risk Signal

Despite strong performance for stocks, the RAI ended the year at its highest level. While we are in a very favorable seasonal window, we recommend taking a more defensive stance for now.

Inflation—Transitory?

- We expect the downward pressure on inflation to persist in the near term.

- But we are starting to think the current pessimism about inflation is a bit overdone.

- Wage related indicators, which is by far the most important driver of inflation, have started to point to a rise in wage pressure as the job market gets tighter.

- Inflation at producers’ level has more downside too in the near future.

U.S. 10-Year - All About Inflation

The collapse in oil prices has brought down inflation expectations dramatically. Inflation will likely be the single most important driver of interest rates in the next 6-12 months.

QE Success Limited - A Transmission Channel Check

Perhaps the most important is the credit channel; the substantial curve flattening that happened recently in anticipation of the Fed hike next year has made lending standards tighter for small businesses.

Risk Aversion Index Stays On “Lower Risk” Signal

Continued strength in equities offsets the weakness in credits and commodities to arrive at an essentially flat reading.

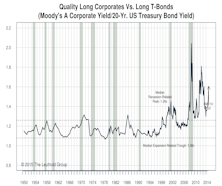

U.S. Investment Grade Corporates: Favorable

Record issuance and oil-related weakness combined to drive the spreads wider but we remain Favorable on these bonds for now.

Inflation—More Downside Threat In The Near Term

Inflation remains weak but is slightly ahead of market expectations. Inflation numbers have not been able to meet the downwardly revised expectations in both developed and emerging markets. The Fed has plenty of room to wait and see and it is in no rush to raise rates until the signs are clear.

Interest Rates Range Bound—Can’t Be Too Bearish

The sell-off in risky assets in early October promptly led to expectations of a more dovish Fed.

Stocks Vs. The Dollar—More Complicated Than You Think

The recent strength in the dollar coincided with a spike in volatility and weakness in risky assets, but the relationship over the last couple years has been tenuous at best.

Risk Aversion Index Fell Sharply—New “Lower Risk” Signal

The dramatic turn-around in risk appetite triggered a new “Lower Risk” signal. It also marks the beginning of a very favorable seasonal window.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue