Articles by Chun Wang Director of Multi-Asset Strategies

Risk Contagion Underway, But There Is A Silver Lining

A Risk Contagion is now underway, and we continue to stay defensive and favor higher quality assets within the fixed income space. A silver lining: When the Risk Aversion Index moves above 1, odds start to favor a decrease in risk aversion going forward. The bulk of the move is probably done.

It Is All About Confidence

As we expected, the U.S. downgrade was digested by the market fairly quickly and attention turned to the economy. This is a bear market in confidence, more than anything else.

It’s The Economy, Stupid

U.S. likely averted worst-case scenario of default, but credit rating downgrade is still likely. Main impact of downgrade is not the increase in interest rates itself, but rather the liquidity risk in all markets that involve treasury securities as collateral.

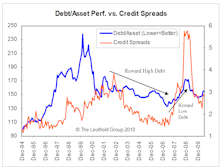

Longer Term Concerns About U.S. Debt And Deficit

$4.8 trillion of the additional $9 trillion in debt that Uncle Sam is expected to incur over the next decade is interest obligation.

Risk Aversion Index Says “Wait And See”

The Monthly Risk Aversion Index edged down slightly in June, pausing for a clearer direction. The biggest contributors of risk are commodities and credit spreads.

Longer Term Concerns About U.S. Debt And Deficit

More than one-half of the U.S. government’s additional $9 trillion in debt expected over the next ten years is projected to be interest. This is a frightening proposition.

Now Entering Increasing Risk Aversion Environment

Risk Aversion Index accelerated in May, making it prudent to favor defensive assets near term. Expect small and gradual increase in long term interest rates.

The Bond Bubble Is Beginning To Deflate… Is This Cheap Money Era Ending?

An orderly decline of the dollar is not necessarily a big concern. On the other hand, a sudden collapse of the dollar, in conjunction with spiking U.S. interest rates, would be a terrible thing. So far this has not been the case.

Monthly Risk Aversion Index (RAI)

This month’s “Inside The Bond Market” presents our new “Risk Aversion Index,” which was developed by Chun Wang to respond to those factors that the bond market is truly worrying about. The Index examines ten factors on a monthly basis to help best position a bond portfolio.

The Bond Bubble Is Beginning To Deflate… Is This Cheap Money Era Ending?

Long term interest rates could continue rising, as inflation expectations increase and investors demand higher yields.

The Bond Bubble Is Beginning To Deflate… Is This Cheap Money Era Ending?

Bond bubble deflating, as investors demand higher yields to compensate for rising inflation and mountain of debt.

Earnings Revisions Stay Positive For Now

Quant implications for earnings revisions. Revisions tend to follow actual earnings, not lead them. Better economy now producing upside surprises, which has good short term implications.

Two Quant Themes With Significant Implications For 2011

Two Quant Themes With Significant Implications For 2011. We revisit studies from the past year that focused on Revenue Growth vs. Earnings Growth, as well as Momentum vs. Value.

The Impact Of Quantitative Easing On Style Factors

Chun Wang examines QE I & II in Japan, along with the initial QE in the U.S., to see how various quantitative factors have reacted in the past. While some factors may prove effective, the main difference between these past QE experience and the latest round is the macro conditions of the market.

Commodities vs. Style Factors: A Risk Perspective

Chun Wang uses the CRB Index as a risk proxy to test the effectiveness of a range of quantitative factors in various environments. Commodity prices have become an increasingly important measure of risk, since higher commodity prices indicate a greater risk appetite and vice versa.

Revisiting Value & Momentum: Sign Of A Top?

Relationship of Momentum stocks and Value stocks has historically demonstrated that at market tops, Momentum does best while Value lags. That pattern is occurring now, but based on prior history the top would not come until Q1 2011.

Go Back To Basics During An Economic Slowdown: Value & Quality

Given the discussion during August of a weakening economy and a potential double dip, Chun Wang looks at which of our quantitative factors do best during a slowdown.

Month In Review: The Quality Trade Returns

Quantitative factor performance throws yet another curve ball. Momentum works with Growth and Profitability for first time this year.

Market Correlation And Group Rotation Strategy

New data series confirms unprecedented correlations in equity markets.

Risk Aversion and “Episodic” Factor Returns: Investors Favoring Conservative Characteristics

We expect risk appetites to remain low and investors to continue to reward conservative stock characteristics over the next 3-6 months.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue