Articles by Chun Wang Director of Multi-Asset Strategies

Inflation Surprised On The Upside

Inflation beat expectations and higher prices were seen across the board. As we expected inflation has been a non-factor in the 1st half of 2014, but will increase moderately in the second half. We expect the Fed to be reactive, instead of pre-emptive, when it comes to inflation, which means the Fed’s tone will remain dovish until inflation becomes a real concern. Inflation at producers’ level seems to be trending moderately higher too.

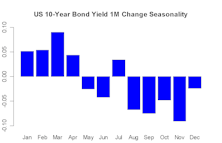

10-Year Yield: Back in 250-280 Range

In the very short term, excessive bearish positions have been reversed so there is less downside pressure on interest rates. Over the intermediate term, incredibly low yields in the Euro-zone help cap the U.S. yield.

Credit Conditions Still Good But Less-Easy Than Pre-Taper

With the Taper underway and the back-up in interest rates over the last year, credit conditions have become less-easy for some consumers and small businesses.

Risk Aversion Index - New Higher Risk Signal

Surprising strength in the Yen, a drop in commodities, and slightly wider credit spreads pushed up the index. An increase in risk aversion becomes more likely at the current extremely low level. Caution is warranted.

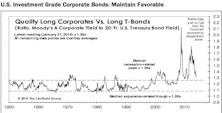

US Bond Market

Although the overall picture remains favorable for high grade credits, the increased exposure to interest rates with an ever thinner spread cushion does concern us. We will monitor closely for potential downgrades.

Inflation Beats Expectations Again

Inflation is at the highest level in the last nine months. Without wage inflation, it’s hard to see substantially higher inflation in the near future. Inflation will be a non-factor in the 1st half of 2014, but will increase moderately in the second half. Inflation at producers’ level seems to show some signs of revival.

10-Year Yield: More Downside

We expect the 245-250 barrier to be tested, and if it is decisively broken, much lower yields could be in the cards.

Sell in May

This does not only apply to stocks, it applies to just about all risky assets.

Inflation Beats Expectations

Inflation increased and beat expectations. Capacity utilization increased more than expected too, a sign that the slack is being worked off. A much more persistent trend in wage inflation is necessary for a sustained inflationary environment and we are still not there yet. Inflation will be a non-factor in the 1st half of 2014. Inflation on the producers’ level is still well contained in a narrow range.

Twisty Curves

The short end of the yield curve sold-off to price in an earlier-than-expected rate hike, while the long end rallied as the prospect of tightening reduced longer-term inflation expectations.

RAI Lower - Stays on "Lower Risk" Signal

Risk assets continued to perform well in March, and our monthly Risk Aversion Index (RAI) fell to near record low levels. We continue to favor high quality credits within fixed income.

Inflation Still Modest

Inflation is still modest and in line with expectations. Hourly earnings rose, but wage inflation probably has to go much higher to make its impact felt. The U.S. has been importing disinflation from the rest of the world and the import prices reflect that. Inflation will be a non-factor in the 1st half of 2014. Inflation on the producers’ level is modest too despite the recent surge in Crude Materials PPI.

RAI Falls Sharply—New “Lower Risk” Signal

This closed out the one month old “Higher Risk” signal. We continue to favor high quality credits within fixed income.

Have We Seen This Post-QE Movie Before? It’s Still Too Early To Call

We looked at the periods around the end of the three previous easing programs (QE1, QE2 and Operation Twist) and compared those patterns with the current ones for various measures. The current patterns from both an economic and a market front bear enough resemblance to the previous ones to make us a bit uncomfortable. February’s market action was encouraging, but it is still too early to rule out a post-QE fizzle.

Inflation Pressure Anemic

Inflation is modest and broadly in line with expectations. Labor costs have stabilized, but the global disinflationary trend has not changed. We maintain our view that inflation will be a non-factor in the first half of 2014, but it might increase moderately in the second half. Inflation on the producers’ level is weak, too and the PPI inflation pipeline doesn’t seem to pose any immediate inflationary threat either.

U.S. Bonds

Given the higher volatility and increased risk aversion, high grade credits are attractive as the negative relationship between rates and credit spreads dampens the volatility of this asset class.

Risk Aversion Index Turns Higher, New “Higher Risk” Signal

We are turning defensive within fixed income and recommend moving up the quality scale.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue