Articles by Chun Wang Director of Multi-Asset Strategies

U.S. Investment Grade Corporate Bonds: Maintain Favorable

More spread compression is likely ahead.

U.S. Municipal Bonds: Maintain Unfavorable

There is still a lot more room for Munis to underperform Corporate bonds.

U.S. High Yield Corporate Bonds: Maintain Neutral

We will be looking for a good follow-through to consider an upgrade of these bonds.

Inflation Modestly Exceeds Expectations

Inflation met or modestly exceeded expectations. The three key drivers for inflation (oil, the Dollar and the Chinese yuan) continued to improve. But we are not rushing to declare victory on disinflation. “Organic” inflation, such as sustained wage inflation, has been very elusive so far.

New Bond Market Record: G5 10-Year Average Hit All-Time Low

Despite the improvement in market sentiment, U.S. bond yields were dragged lower by their international counterparts.

Muddle-Through Still Has The Benefit Of The Doubt

The market’s latest infatuation with bonds was driven by grave concerns that the weakness in energy and manufacturing sectors might be spreading to the U.S. economy as a whole.

Risk Aversion Index—Ticked Lower But Stayed On “Higher Risk” Signal

We believe a short term rally is more likely and recommend a neutral stance towards credits at this point.

Inflation Surprised To The Upside

Both CPI and PPI surprised to the upside.The three key drivers for inflation (oil, the Dollar and the Chinese yuan) all saw some improvements. Despite the recent improvements, we are still in no hurry to call the bottom in inflation. The downturn in the energy and manufacturing industries has wide-reaching effects. Patience and caution are still warranted.

Market’s Message To The Fed: Stop The Tightening!

We think the Fed’s projection of four more hikes this year is absolutely unachievable, and we are no doubt siding with the market’s current projection of one hike, at most (if any), this year.

The Current State Of Stock-Bond Relationship: Risk-Off

The transition we saw last year from a mostly Risk-On (or Easing) environment to a more challenging Tightening (or Risk-Off) environment has made the relationship especially volatile.

Risk Aversion Index—Moved Up; A New “Higher Risk” Signal

We are aware of the oversold condition in oil but we expect volatility to remain high in the near term. We maintain a defensive stance towards credits at this point.

Inflation Lower Than Expected

Inflation was lower than expected in December. The three key drivers for inflation this year are oil, the Dollar and the Chinese yuan. None of these are helping so far. We have been avoiding inflation sensitive assets and do not see any reasons to catch the falling knife at this point.

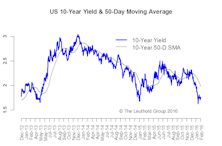

2015 - All Risk And No Reward

The U.S. 10-year yield was quite volatile, fluctuating in a 100 bps range between 160 and 260, and ending up a mere 10 bps higher for the year. But it was still better than most other major asset classes which saw all risk and no reward.

2016 Time Cycle—Not Likely To Be A Typical Year

The 2016 pattern looks good on paper, but if the excitement in the first week of the year is any indication, we highly doubt 2016 will turn out to be another typical election year.

Risk Aversion Index—Moved Up But Stayed On “Lower Risk” Signal

Despite the mechanical “Lower Risk” signal, we are clearly in a risk-off environment. We recommend a defensive stance towards credits at this point.

Inflation Watch-Remains In Line With Expectations

Inflation was largely in line with expectations in November. The impact of lower energy prices seems to have lessened as the year-over-year comparison gets better. We are far from ready to call a return of inflation. The ISM price indexes supported our still cautious view towards inflation.

Impact Of The First Hike - This Time Might Really Be Different

At this point, the worst outcome for the risk markets would be no hike in December.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue