Stock Market Internals Earnings Momentum, Small/Mid/Large Caps, Growth/Value/Cyclicals, and Additional Factors

Small/Mid/Large Caps

Small Caps are selling at a 17% valuation premium relative to Large Caps (19% last month), using non-normalized trailing operating earnings. The Small Cap sell-off over the last three months has pushed us away from the recent peak premium of 23%.

Growth/Value/Cyclicals

Growth outperformed Value in all market cap subsets: Large Cap, Mid Cap, and Small Cap. It also snapped a five month losing streak with Cyclicals. Despite the reversal, Growth is still lagging YTD, and is extremely undervalued compared to Value.

Additional Factors

As the market found a new leg higher the last two weeks of May, the Cap Weighted and Equal Weighted S&P 500 Indexes had uniform advances—just over 2% for the month. The Equal Weighted Index maintains an 80 bps lead YTD.

Earnings Momentum

Initial Q1 Earnings Well Below Average.

Small/Mid/Large Caps

Small Caps are selling at a 19% valuation premium relative to Large Caps (23% last month).

Growth/Value/Cyclicals

In April, Large Cap Value widened its YTD outperformance over Large Growth to 730 bps.

Additional Factors

Market Cap has been slightly better than equal the past two months.

Earnings Momentum

“Three Month” Up/Down Earnings Ratio Ends Q4 With a Whimper.

Small/Mid/Large Caps

Small Cap Premium Bounces Back To 23%

Growth/Value/Cyclicals

Growth Takes It On The Chin In March.

S&P 500 Equal Weight

Cap Weighted Slightly Better In Flat Performance Month.

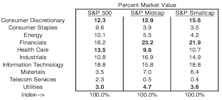

Sector Characteristics of the S&P Indicies

Important characteristics of the broad sectors of the S&P 500 along with the S&P Mid Cap and Small Cap indices.

Earnings Momentum

The second month of Q4 earnings came in with an Up/Down Ratio of 1.54, just above the historical “two month” average of 1.53.

S&P 500: Equal Weighted Index Continues To Excel

As the market rallied in February, the S&P 500 Equal Weighted Index (+5.2%) handily outperformed the Cap Weighted S&P 500 Index (+4.3%).

Growth/Value/Cyclicals

Growth Outperforms Value In February.

Small/Mid/Large Caps

Small Caps are selling at a 20% valuation premium relative to Large Caps (23% last month), using non-normalized trailing operating earnings.

Sector Weightings Adjust To Reflect January Loss Leaders

Consumer Discretionary sector weightings sank among all three market tiers, as this segment led the market lower in January. Health Care and Utilities sector weightings increased, as both outperformed for the month.

S&P 500: Equal Weighted Index Slightly Better in January

.png?fit=fillmax&w=222&bg=FFFFFF)

The Equal Weighted Index has outperformed the Cap Weighted Index in seven of the last nine months.

Growth/Value/Cyclicals

.png?fit=fillmax&w=222&bg=FFFFFF)

Small Cap Growth Outperforms (On Relative Basis) In Down Month

Small/Mid/Large Caps

Small Cap Premium Continues Upward To 23%. Large Caps Lead On The Downside In January

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue