Inside The Stock Market ...trends, cross-currents, and outlook

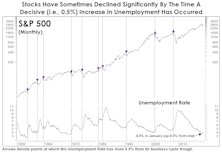

Unemployment And The Point Of No Return

We’ve done extensive work on the yield curve, but until now had entirely overlooked an employment-based recession indicator that’s lately come into focus.

A Scary Chart, Revisited

For a couple years, we’ve labeled the S&P 500 Price/Sales ratio as the scariest chart in the Leuthold database, and last year’s decline did little to improve its intimidating appearance.

Sector Concentration And Effects On Country Performance

Is the performance of certain countries mainly driven by particular sectors? And, does U.S. sector performance drive the performance of other countries? (i.e., when U.S. Financials underperform, do foreign countries with large Financials sector weights underperform?). We did some data crunching to address the second question.

A High-Risk Rally

During the market bounce over the last few weeks, we reminded ourselves and others of the old maxim that “bear market rallies look better than the real thing.” Evidently, the stock market overheard us and took the advice as marching orders.

Did The Doves Swoop In And Save The Day?

Just a few months ago, Fed Chairman Jerome Powell boasted a reputation as a straight-talking, sound-money banker.

It Wasn’t Powell Who Panicked

The Fed’s “Christmas capitulation” seems to get most of the credit for the stock market rebound, but we’re not exactly sure how, or even if, the Fed capitulated at all.

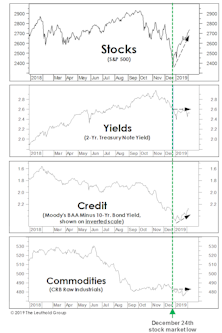

Credit Conundrum

The stock market seems to have concluded that a recession will be averted in 2019, but evidence from other asset markets is less convincing.

What Are Bonds Telling Us?

Corporate bonds aren’t the only asset reluctant to embrace the stock market’s latest “all clear” verdict on the 2019 economy.

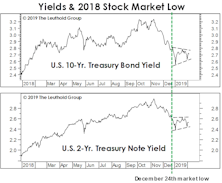

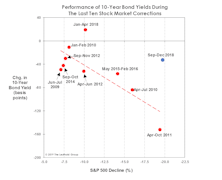

1998 Parallels

There are enough parallels between the 1998 and 2018 market declines that we decided to flesh out the comparison a bit more.

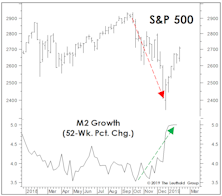

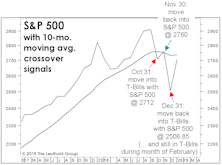

Trend-Following Travails

To recap our allocation moves over the last year: We established an initial equity hedge in tactical accounts very close to the January 2018 highs.

New Year, Old Leadership

We’ve written at length about a bear market’s tendency to catalyze major leadership changes—across sectors, styles, and even geographies.

Sifting Through The Commodity Carnage

Commodities were the worst performer among the major asset classes during 2018, with the S&P/Goldman Sachs Commodity Index losing 13.8% on a total return basis.

Are New Lows The Key To New Highs?

Last year’s market decline was one of the largest to have occurred without a lengthy-preceding period in which breadth narrowed and Small Caps significantly underperformed.

The Line Of Least Resistance Is Lower

At some point in his career, famed stock trader Jesse Livermore ceased using the terms bull and bear, opting instead to describe trends in terms of “lines of least resistance.”

Is The “Star” Aligned For 2019?

For those who remain skeptical that more stock market troubles lay ahead, we’ve supplemented the MTI and our other market tools with something truly authoritative: Evidence from a gossip column in a 1958 issue The Minneapolis Star!

About That Great Jobs Report...

The December employment report temporarily eased fears of a severe U.S. slowdown. That’s a mystery to us.

The Market Is Off Its Meds!

While investors obsess over the market level at which a hypothetical “Powell Put” might come into play (or whether such a put even exists), they seem to have overlooked the absence of another such put that proved dependable throughout the cyclical bull market.

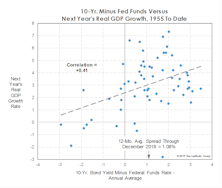

Yields Might Be Throwing A Curve

While the number of recession forecasts is on the rise, there’s a general reluctance among economists to project a downturn in the absence of a yield curve inversion.

The Fed Was Not The Only One To Tighten Last Month

Wage inflation should accelerate in the months ahead, oil could bounce from its oversold low, and college textbooks might double in price before the fall semester. No problem…

December’s Low Didn’t Have The “Right Look”

As the market sunk to a 3% loss on Christmas Eve, we sensed genuine investor panic—at least among the fraction of investors then paying attention.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue