Inflation

Implications Of Low Growth, Low Inflation, Low Rates

The current environment will likely persist longer than most expect which will put further downward pressure on profit margins. As margins come under pressure, companies increase leverage to prop up ROE. However, the market wants higher duration, not higher leverage.

Inflation Modestly Exceeds Expectations

Inflation met or modestly exceeded expectations. The three key drivers for inflation (oil, the Dollar and the Chinese yuan) continued to improve. But we are not rushing to declare victory on disinflation. “Organic” inflation, such as sustained wage inflation, has been very elusive so far.

Inflation Surprised To The Upside

Both CPI and PPI surprised to the upside.The three key drivers for inflation (oil, the Dollar and the Chinese yuan) all saw some improvements. Despite the recent improvements, we are still in no hurry to call the bottom in inflation. The downturn in the energy and manufacturing industries has wide-reaching effects. Patience and caution are still warranted.

2015 - All Risk And No Reward

The U.S. 10-year yield was quite volatile, fluctuating in a 100 bps range between 160 and 260, and ending up a mere 10 bps higher for the year. But it was still better than most other major asset classes which saw all risk and no reward.

Inflation—Expecting More Drag From Oil

With the recent weakness in oil prices and the renewed strength of the U.S. dollar, we would not be surprised to see weaker headline numbers in the next few months. The expectations of a rate hike might actually end up pushing the rate hike further out. We are now less sanguine about a pick-up in PPI in the rest of the year.

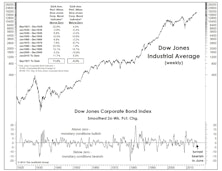

A Venerable Monetary Indicator Turned Negative

The smoothed, 26-week rate-of-change in the DJ Corporate Bond Index, a reliable indicator of monetary conditions over many different market and economic cycles, turned negative in mid-June.

Navigating The First Rate Hike

Our current view is the lift-off will be December or later. Assuming inflation will pick up and the Fed hikes the rate by the end of 2015, stocks will perform relatively well, with international stocks a better bet than U.S. stocks.

End Of The QE Trade? Too Early To Call

The common driver behind the sharp reversal of many recent asset class trends is the unwinding of the ECB QE trade.

Another Take On The Inflation Debate

While there’s understandable obsession over the likely level of inflation (especially with the year-over-year CPI dipping below zero in the past two months), equity managers with no interest or skill in inflation forecasting might be better served by monitoring the character of inflation—i.e., whether it was led by changes in consumer or producer prices.

Inflation & Monetary Policy—A Feedback Loop

Inflation and inflation expectations are key inputs to central banks’ policy decision process. Divergent policies have very different impacts on inflation.

Inflation & The Dollar

Are U.S. markets for labor and capital actually getting tight?

Twisty Curves

The short end of the yield curve sold-off to price in an earlier-than-expected rate hike, while the long end rallied as the prospect of tightening reduced longer-term inflation expectations.

High Correlations And Their Meaning

While our tongue-in-cheek “Correlation Of Everything” measure has retreated from record levels, it remains far above anything seen prior to 2010.

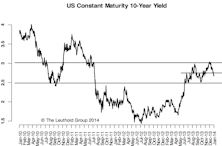

U.S. 10-Year: 245-250 Area A Strong Barrier

We expect the 245-250 area, the upper bound of the previous lower range, to be a strong barrier.

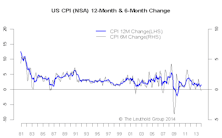

Inflation Pressure Anemic

Inflation measures are broadly in line with expectations, and overall inflation pressure is anemic. We maintain our view that inflation will be a non-factor in the first half of 2014, and it might increase moderately in the second half. Inflation on the producers’ level is weak, too and the PPI inflation pipeline doesn’t seem to pose any immediate inflationary threat either.

A Taper & Hibernating Bears

The rise in interest rates after the taper was on the back of low liquidity around the holidays. 3% is a pretty strong upper bound for the 10-year, and a failure to stay above this level will probably see a re- test of the 275 level in the near term.

The Dual Mandate Presents A Clear Dilemma For The Fed

The “dual mandate,” which means the Fed is paying close attention to both inflation and employment, presents a clear dilemma for the Fed when it comes time to decide on a taper.

Inflation Lower Still

We maintain our view that inflation will be a non-factor for the next six months but will increase moderately in the following six months.

Five Reasons Inflation Is Still Missing

Overall demand slack, stubbornly low velocity of money, an overall stronger dollar, painfully low labor cost inflation and weakness in commodity prices are strong disinflationary forces.

Inflation Still Going Nowhere In The U.S.

Inflation at both consumers’ and producers’ level is still modest. A drawn out government shutdown and debt ceiling debate will hurt the economy, which could further push out the taper timeline.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue