Inflation

Mild Deflation Short Term… Mild Inflation Next Twelve Months

This transition from deflation to mild inflation will be a “numbers game,” as 2009 readings are compared against 2008’s second half deflation, driving current twelve month readings up

Mild Deflation Short Term… Mild Inflation Next Twelve Months

The greatest danger in late 2010 and 2011 is monetary debasement inflation, not demand based inflation. Trillion dollar deficits (or higher) may be acceptable shorter term (2009), but unless our government and politicians provide strong evidence of fiscal responsibility, the dollar’s respectability could be undermined, with foreign lenders and investors going elsewhere.

Mild Deflation Short Term… Mild Inflation Next Twelve Months

The greatest danger in late 2010 and 2011 is monetary debasement inflation, not demand based inflation. Trillion dollar deficits, and higher, may be acceptable shorter term (2009), but unless our government and our politicians provide strong evidence of fiscal responsibility, the dollar’s respectability could be destroyed with foreign lenders and investors going elsewhere.

Expect To See Rising CPI/PPI Inflation As Economy Recovers

Rising food and energy prices will more than offset deflationary CPI housing subset, ultimately driving the twelve month CPI rate to +3.6% by mid 2010.

Deflation To Reflation… Give It Some Time!

Expectations for broad leadership from inflation-beneficiary sectors of Materials and Energy tell us that investor obsession seems to have shifted too rapidly from deflation to “reflation”.

Expect To See Rising CPI/PPI Inflation As Economy Recovers

As the global economy recovers in 2010, we expect the PPI twelve month rate to accelerate to +5% as commodity prices continue to rise.

Fall To Deflationary Territory Should Be Short Lived

As first half of 2009 readings compare against inflationary 2008 first half readings, the twelve month rate will sink further into deflationary territory, probably to around –6%. But the second half of 2009 will be a different story, as commodity prices could continue to rebound or at least stabilize (anticipating economic recovery).

Fall Into Deflationary Territory Should Be Short Lived

CPI/PPI inflation readings are expected to dip into deflationary territory in the first half of 2009.

Fall Into Deflationary Territory Should Be Short Lived

Compared against very deflationary readings in the second half of 2008, PPI could finish 2009 up +2.0%. The worst of the commodity price downdraft should be behind us.

Decline Into Deflationary Territory Could Be Short Lived

2008 was a deflationary year for the PPI (–1.2%). 2001 was the last calendar year with deflation (-1.8%), and it was also a recession year.

Recent CPI and PPI Readings Declined By Largest Percentages In Over 60 Years

Currently declining energy and other commodity prices are producing some significant “down” months for CPI and PPI.

Deflation… What If? (Part II)

Once again, this month’s “Of Special Interest” examines deflation but employs a longer time horizon. We also contrast the deflationary environment in Japan versus current U.S. conditions.

Outlook: Weak Economy, Inflation Decelerating

The consumer is in the worst shape that we can remember. September job loss was the highest in five years.

Deflation….What If?

Mild deflation is nothing to fear: An environment of 0% to 2.4% deflation has proven to be one of the more conducive environments for stocks.

Outlook: Weak Economy, Inflation Decelerating

Revised Q4 real GDP confirms what we’ve been saying for quite some time...the U.S. economy began contracting in Q4 2007.

Portraits Of Declining Inflation

Jim Floyd and Steve Leuthold believe that U.S. consumer price inflation has peaked and is headed for the +3% level by mid-2009. With current headline inflation running at +5.4%, that implies there is plenty of disinflation in the pipeline.

CPI Expected To Decelerate

CPI inflation measured on a twelve month basis has probably peaked. Looking ahead, inflation should cool off in the first half of 2009 (+3%). Here’s why....

CPI Expected To Decelerate To +5% By Year End

CPI Inflation measured on a twelve month basis may be close to a cyclical peak.

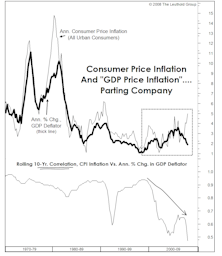

The GDP Report: “Exhuming McCarthy”

Significant disconnect between GDP Deflator and CPI. Recent GDP report implies a 1.1% inflation rate. It is ridiculous to assume the inflation rate is that low with the CPI at +5.5%.

CPI Expected To Peak Near +5.5%

Inflation should be cooling off as the U.S. economy contracts and global economies show signs of slowing.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue