Inflation

Longer Term Concerns About U.S. Debt And Deficit

The kneejerk reaction to worries about excessive sovereign debt has been to bail out of the European sovereign debt and pile into U.S. sovereign debt. Unless the U.S. can get its own fiscal act together, we may face this same panic reaction farther down the road.

Mild Inflation, But No Deflation In 2010

We are maintaining our 2010 CPI estimate of +1.2%. (Core CPI +0.9%.)

Are We In A Bond Bubble?

Bond bubble continues to inflate, much like money pouring into tech stocks at the height of the internet bubble.

Year End Twelve Month CPI Deflation Reading Unlikely

Looking ahead to 2011, we are keeping a close eye on Housing, Food and Wages, which all could be bottoming out.

Longer Term Concerns About U.S. Debt And Deficit

A mountain of new debt, a balloon of short term borrowing due near term, and the likelihood of higher interest rates are big hurdles.

Inflation Tame

Looking ahead to 2011, we are keeping a close eye on Housing, Food and Wages, which all could be bottoming out.

CPI Tame For Now, 2011?

Gently rising CPI inflation at present can be best characterized as normal business cycle inflation.

Longer Term Concerns About U.S. Debt And Deficit

A mountain of new debt, a balloon of short term borrowing due near term, and the likelihood of higher interest rates are big hurdles. Moody’s says U.S. debt could test its AAA rating.

Mild CPI Inflation Expected In 2010

The greatest danger in late 2010 and 2011 is monetary debasement inflation, not demand based inflation.

Longer Term Concerns About U.S. Debt And Deficit

A mountain of new debt, a balloon of short term borrowing due near term, and the likelihood of higher interest rates are big hurdles. Moody’s says U.S. debt could test its AAA rating.

Mild CPI Inflation Expected In 2010

The greatest danger in late 2010 and 2011 is monetary debasement inflation, not demand based inflation.

Mild CPI Inflation Expected In 2010

Mild CPI Inflation Expected In 2010 (+3.2%); Higher PPI Inflation (+6.0%)

Commodities… And The “Old Normal”?

A loss in leadership by commodity-oriented stocks could be the big surprise for 2010. Commodity sentiment is elevated, and the sector should feel the after-effects of a capacity building binge from late last decade. Rising inflation—if it’s the monetary debasement variety—won’t lift the sector.

Weak Dollar Could Continue To Contribute To Higher Commodity Prices

U.S. commodity prices are again trending higher, like they did in 2002, as the U.S. economy recovered. The weak U.S. dollar helped, and recent rally might not last.

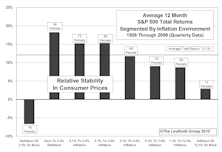

Rising Inflation: Not Always Bad For Stocks… Especially Small Caps

A look at stock performance in various inflation environments would seem to predict below average performance in 2009, but threat of monetary debasement inflation in 2011 and beyond could set the stage for poor performance.

Leuthold Commodity Diffusion Index Remains Negative

Like they did in 2002, as the U.S. economy recovered, U.S. commodity prices are again trending higher.

Mild Inflation Next Twelve Months

This transition from deflation to mild inflation will be a “numbers game” as late 2009 readings are compared against late 2008’s strong deflationary readings, driving the twelve month rate up.

Commodity Diffusion Index Now Signaling Rising Inflation

Commodity Diffusion Index hit 75%, an indication of rising inflation pressures. Moves above 70% in this inflation gauge have served as a pretty good sell signal for stocks.

Mild Inflation Next Twelve Months

By year end 2009, we expect the twelve month PPI to be back up in mildly inflationary territory.

Countering The Consensus Gloom

There’s an overwhelming consensus that the U.S. economy has slipped into a long-term phase of declining growth in real GDP and chronically higher unemployment. Here’s a dissenting opinion from a client, along with Steve Leuthold’s response.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue