Inflation

2007 Outlook: CPI Tame First Half And Economy Chugging Ahead Slowly

Expect economic recovery to pick up a little steam in early 2007, before slowing down in the second half. A 2008 recession is a possibility.

Inflation Still A Potential Threat

Looking ahead, CPI twelve month rate of inflation is likely to be in the +2% area for the first half of 2007.

2007 Outlook: CPI Stabilizing First Half And Economy Chugging Ahead Slowly

Bond yields continue to fall as economic reports have tended to be on the weak side. Massive global liquidity and the search for yield have also helped to push yields lower. We have been way off the mark with our predictions for higher rates.

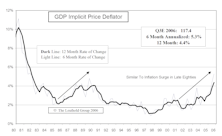

Inflation Concerns

Inflation expectations seem to be on the rise.

Bond Market Correction Did Not Happen In October

Our call for a bond market correction did not pan out in October, but yields did back up in early November as weak productivity and a surprisingly low unemployment rate were released.

Inflation Watch

CPI on a twelve month basis expected to decelerate further over the next month or two. Final two months of the year, however, could be another story, with CPI twelve month inflation reaccelerating.

Inflation Watch

CPI on a twelve month basis is expected to decelerate further over the next two months. The final 3 months of the year, however, could be another story.

Bond Market Overextended...Correction Ahead?

Bond market seems to be anticipating three key developments: Fed’s stance could switch from tightening to easing, the economy is slowing significantly, and inflation is licked.

Commodity Inflation = OWN MATERIALS STOCKS; Commodity Deflation = OWN MATERIALS STOCKS!!

There remains considerable macro support for industrial commodities.

Inflation Watch

CPI on a twelve month basis still expected to decelerate over the next three months. The final 3 months of the year, however could be another story, with CPI twelve month inflation accelerating.

Economic Outlook

Continue to project higher interest rates over the next six months, particularly longer maturities. Short rates could begin to decline by early-mid 2007, after Fed finishes tightening and economy slows.

View From The North Country

Half time update. Leuthold looks back at December 2005 predictions. Additional comments on Inflation, Corporate Earnings, The Dollar, Oil Prices, Gold, and Federal Budget Deficit.

Inflation Watch

CPI still expected to decelerate over the next four months as current readings get compared to above average readings a year ago. The final three months of the year, however, could be another story.

Inflation Watch

Raised our 2006 CPI estimate (mid-May) to +4.5% from initial projection of +4.0% or less.

Inflation Watch

The Major inflation concerns are rising wages, low unemployment, a continued strong economy, and additional pass through of higher energy prices.

PPI Remains Above CPI: Bad Omen For Profits?

PPI rate of change exceeds the CPI at present, and has been higher since late 2003. Could be a bad omen for corporate profits.

Inflation Watch

Inflation, particularly wage inflation, continues to accelerate. Wage inflation is now at its highest level since 2001.

Inflation Watch

The major inflation concern is to what degree significantly higher energy costs will be passed through, even if energy prices stabilize or decline.

Economic Outlook

It may be difficult for the economy to prolong its expansion, with the auto and housing sectors weakening and consumer spending a big question mark.

Inflation Watch

Expecting economy to slow in 2006, with possibility of recession developing late in the year. Energy prices remain a wild card.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue