Inflation

Inflation-As Flat As The Yield Curve

The latest Core CPI number disappointed again. The divergence between inflation break-evens and the yield curve is puzzling. Given the lack of inflationary pressure and the Fed’s projected rate path, it would not surprise us to see a flatter curve without the help of fiscal stimulus in the next few months.

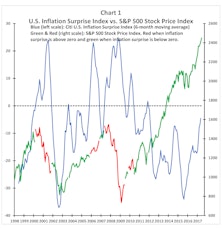

Stocks Versus Your “Personal” Inflation Rate

While the bull possesses a seemingly endless supply of energy, the Leuthold database still houses a supply of measures by which the bull market has fallen short.

Goldilocks—Alive And Well

If we look beyond the daily noise from North Korea, the global macro picture still fits our “Goldilocks” view pretty well.

Where The Bear Lingers

While the next recession could be caused by a variety of factors, we suspect the recovery will eventually end like most post-war expansions, only after a significant rise in interest rates.

Inflation Disappoints Again

The CPI numbers have disappointed three months in a row. Weak commodity prices do not inspire higher inflation expectations. The global scope of inflation deceleration adds more weight to the recent soft readings. However, lower bond yields relative to nominal growth rate is inflationary and buffers the impact of weak inflation and rate hikes.

Inflation Complacency?

Leading inflation indicators have leveled off so far in 2017 after last year’s huge rebound from the deeply oversold readings produced by the 2014-2015 collapse in commodities.

Goldilocks—Enjoy It While It Lasts

The best interpretation of the current cross-asset message is the scenario of goldilocks, and there are reasons to believe this is a possible scenario for the near term.

Inflation-Weaker Sooner Than Expected

The latest CPI is weaker and the softness was sooner than we expected. More alarming is the recent broad-based deterioration in economic data. Lower inflation expectations have flattened the yield curve recently, which hurt Financial stocks. We believe inflation has likely peaked for the time being and patience is the right approach for the reflation trade at this point.

A Dovish Hike--Positive For Inflation

The dovish rate hike is a positive for inflation and credit. A hawkish message right now would have been quite detrimental and self-defeating in terms of realizing two more hikes later this year. We believe achieving sustained 2-3% inflation could be harder than most people expect going forward. Overall, we are encouraged by the dovish hike but we think the real test for inflation is when the base effect starts to wane.

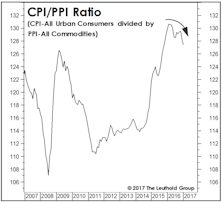

Lo And Behold, Another RATIO!!

For managers who must remain fully invested in equities (or “paid to play,” as we’ve often called it), the level of inflation might prove a less important consideration than its character.

Inflation: Just A Cyclical Uptick

We should emphasize that any inflation pickup is likely to be a traditional, late-cycle phenomenon stemming from rising wage growth and rebounding commodity prices. We do not expect a secular move toward significantly higher inflation rates (say, north of 3.0%-3.5%).

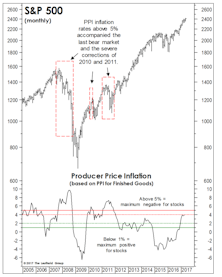

Could Inflation Threaten The Stock Market?

Over the last 70 years, stocks have made no cumulative progress when Producer Price Inflation runs above 4%. Returns have been average when PPI inflation runs between 2% and 4%—where it is today.

Inflation-All About That Base

CPI numbers were strong and better than expected. A big part of the recent upturn in inflation has to do with the much lower base from a year ago. We are seeing upside inflation surprises on a global basis but wage inflation is still disappointing. We are encouraged by the general uptrend in inflation data but we think the real test comes after the positive base effect subsides.

Reflation And Election Year Patterns—Not Much To Lean On

· One bright spot in last month’s lackluster market action was that inflation sensitive assets saw impressive relative returns.

Inflation Remains Largely In Line With Expectations

The latest jobs report disappointed but we think it’s a short term aberration as other data still point to a healthy job market. Some of the key market-based inflation drivers, however, have reversed course a bit in the last couple weeks. Patience is still the right strategy.

Inflation Hindered; Contributing To A Flattening Yield Curve

A stronger dollar and a weaker Chinese yuan dented the prospects for higher inflation in May.

Time For Materials?

The Leuthold Materials sector jumped five spots to #3 in the June Group Selection (GS) rankings, its highest ranking in eight years and the first reading outside of the bottom four in almost four years.

Inflation Exceeded Expectations In April

Inflation exceeded expectations in April. The more durable inflation measures such as wage inflation are also improving. We characterize the recent improvement in inflation as a relief from the threat of deflation but still quite far from being a catalyst for run-away inflation.

Reflation Trade Back In Vogue? We’d Rather Be Late Than Early

Despite recent improvement in some inflation measures, we are not convinced the war against disinflation has been won. The risk of being too early on the inflation call far outweighs the risk of being too late.

Inflation-Patience Recommended

Inflation missed expectations in March. The three key inflation drivers this year - oil, the Dollar and the Chinese yuan, are all going in the right direction. The risk of being too early on the inflation call far outweighs the risk of being too late. Patience is still recommended.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue