Fed Policy

Enjoying It While It Lasts

We don’t think the current stock market upleg is over.

Stock Market Observations

The S&P 500 has labored beneath its March 1st bull market high for the last two months while underlying breadth and leadership trends have remained mostly favorable.

Why The Treasury Department Should Watch The Tape

In recent years the Fed has been more forthright than ever about the importance of the wealth effect as a transmission mechanism of monetary policy. But this (or any) policy effect hardly exists in a vacuum, and the Fed would do well to recognize that stock market swings have played an increasingly important role in the country’s fiscal balance.

Policymakers’ Shell Game

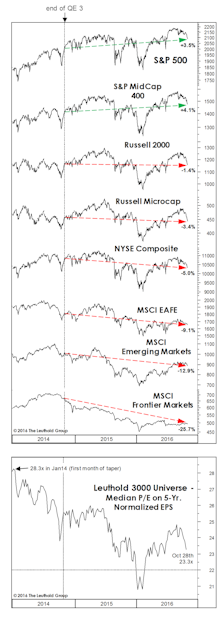

We considered the launch of the QE tapering program in January 2014 as the formal onset of the Fed’s tightening campaign, and that view seemed to be on the mark when High Yield bonds, and then stocks, unraveled over the next couple of years—although the final losses in the DJIA and S&P 500 fell short of what we expected.

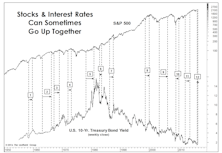

Rising Rates: Not Always A Death Knell

While the Dow Jones Bond Indicator has stood the test of time, history shows that rising bond yields are not always a bearish stock market phenomenon.

Putting “Our Spin” On The Positive Spin

Bull markets seem to create their own moods that lead to fundamental developments being viewed in a mostly favorable light.

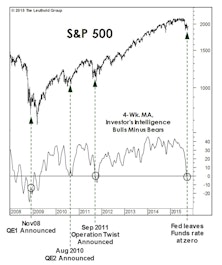

Has The Fed Already Hit Stocks?

One never appreciates what he or she has until it’s gone. In our case, during the many years it was freely available, we failed to appreciate the zero interest rate. Now that it’s gone, we already feel pressured to join a game where we (and very few others) have any edge: Fed-watching. Our real edge is that we recognize this.

Goodbye ZIRP, Hello WIRP

Allow us to put forth yet another theory for this season’s plummet in NFL television ratings: Fed watching is back!

Rate Hike In Limbo—Positive For Risk Assets

Whether rates hike in September or December, we know the Fed will be very supportive of the market and the biggest beneficiaries will likely be EM and higher-yielding assets.

The Policy Conundrum

Over the last eight years, policymakers around the world have held interest rates at unimaginably low levels, run persistently large fiscal deficits, and (in some cases) engaged in outright money-printing via quantitative easing programs.

The Fed’s Capitulation To The Dovish Side— A Win-Win For EM & U.S.

We have mentioned a number of times that China had experienced a very unpleasant “second-hand” tightening due to its peg to the dollar. Its trade competitiveness has suffered tremendously. With a weaker dollar the Chinese Yuan can re-gain some of its competitiveness while maintaining its peg to the dollar. A rare win-win in today’s convoluted world of finance.

Big U.S. Banks: We Have A Motion, Is There A Second?

YTD the S&P 500 has fallen 2% while the S&P 500 Banking industry group is down over 12%—a shortfall that has the attention of value investors and contrarians seeking a chance to buy high-quality banking franchises at fire-sale prices.

Was That All There Was To It?

As quantitative investors, the disciplines of the numbers trump stories—even our own. But we’re struck that the stories depicted by our Major Trend Index and other market tools over the past two years are entirely logical and sequential. Unfortunately these stories rhyme with those of past market cycles.

How Much Slack?

By now it’s consensus that the Fed missed the ideal window for the first rate hike (if one ever existed) by at least a year and a half. We don’t disagree…

Too Early To Dethrone Dividend Stocks?

In the context of a low growth/low inflation environment, with the Fed taking its time to guide rates upward, fixed income type of investments may pale by comparison to dividend paying stocks.

Fed Tightening: The Two-Year Anniversary?

We’ve long argued that this tightening cycle began in January 2014, the month of the first of seven tapering moves which occurred through October of that year. There’s both economic and market evidence to back up this claim.

Sentiment, The Economy & The Fed

We wrote in the January book that 2015 would serve up no shortage of excuses for the Fed to hold off on tightening all year. Whatever window the Fed may have had is now closed.

Fed Watching For The 21st Century

Deteriorating stock market breadth and worrisome leadership trends both suggest liquidity has already tightened; whether the Fed follows suit in September may now be just a formality.

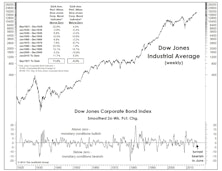

A Venerable Monetary Indicator Turned Negative

The smoothed, 26-week rate-of-change in the DJ Corporate Bond Index, a reliable indicator of monetary conditions over many different market and economic cycles, turned negative in mid-June.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue