Fed Policy

What Should Quants Count?

On May 25th, Fed Chair Jerome Powell promised to pull back emergency support “very gradually over time and with great transparency.”

“Very gradually?” No one doubts that. But “with great transparency?” Not a chance...

More On The “Rate-of-Change” In Rates…

The liquidity and interest-rate backdrop for stocks has been favorable to such an extreme that we’ve cautioned any minor diminution in this condition could trip up the stock market. On that score, the monetary aggregates and the Fed’s balance sheet don’t pose much concern. On the other hand...

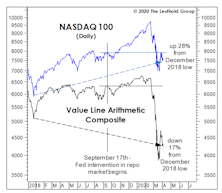

Ruminations On The Fed, Past And Present

If the “Maestro’s” image was dinged from being the “original bubble-blower,” imagine what will happen to Jay Powell’s if stock valuations mean-revert alongside interest rates and inflation over the next few years.

Early-Cycle “Overheat?”

Equities continue to benefit from an odd combination of faith and doubt in the Federal Reserve: Faith that the “Fed put” under financial markets is struck closer to the price of the “underlying” than ever before, and doubt that limitless liquidity will trigger a dangerous rise in consumer prices. In all fairness, this glass half full assessment is hardly a theoretical one, but one based on years of empirical evidence.

A 40-Year Inflationary Echo

When measured by the gains in stocks, gold, and house prices, there has been just one other occasion in which asset inflation was as “broad” as today—late 1980. But the differences in underlying fundamentals between then and now couldn’t be more stark.

A “Fed” Conundrum

“Don’t fight the Fed” has been great advice for stock market investors over the last nine months. For 2021, that won’t cut it. It should be: “Don’t believe the Fed.”

Liquidity: As Good As It Gets?

Stock market manias thrive on buzzwords, and if there’s a single one that captured the essence of the late 1990s’ boom it was “productivity.” In today’s version, our top candidate is “liquidity”—and we doubt anyone would argue.

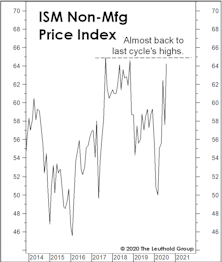

Inflation In The Wrong Places?

Long before policymakers’ extreme response to the COVID collapse, we feared that the Fed’s interventions were suppressing important signals from the stock and bond markets. But we now suspect that hyper-expansionary policies are suppressing price signals from the “real” economy as well.

Inflation: Looking Beyond The CPI

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The Fed is hell-bent on generating inflation of 2% or higher in an over-supplied world that we think should probably be experiencing mild deflation. Their success or failure at this mission will be critical for asset allocators. For equity managers who must remain fully invested, however, the more important question might be not whether the Fed can generate higher inflation, but where.

An Unwelcome Surprise?

Several measures of U.S. economic “surprises” have soared to all-time highs in the last couple of months, showing that even economic forecasters have finally learned to play the corporate game of “under-promise then over-deliver.” Mind you, that’s only 30 years after most industrial firms eliminated the role of “staff economist.”

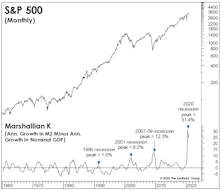

Can Money Growth Trump All Else?

In 2019 and 2020, our regard for time-tested valuation tools resulted in tactical portfolios being underexposed to stocks during a pair of tremendous rallies. Now, the critique is that we don’t appreciate the brilliance of today’s policymakers and their miraculous ability to pivot just when the stocks (and, in the latest case, the economy) need it most.

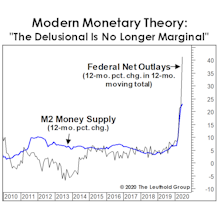

The Tab For “Freebies” Keeps Escalating

There’s an underlying faith that bureaucrats at the Fed and Treasury will keep good and bad businesses, alike, afloat—and overvalued. We’re still trying to unearth a single historical analog that merits such confidence.

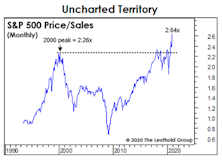

Musings On A Manic Market

Officially, those quick to pronounce the move off March lows as a new bull market have been proven correct with new S&P 500 all-time highs. Fundamentally, though, there’s enormous risk in Large Cap valuations, regardless of where one believes we are in the economic cycle.

A New Proposal To The Fed: Buy Bank Stocks!

While most economic numbers have been positive, the fly-in-the-ointment was the latest Senior Loan Officers’ Survey. Banks have tightened their lending standards across the board.

Measuring The Cost Of “Free”

The S&P 500 and NASDAQ have lately traded as if the hybrid “Fed/Treasury put” entails no cost at all. But dollar alternatives—like forex, precious metals, and crypto-currencies—are saying, “Not so fast!”

Free For All?

The weekly covers of The Economist do a pretty good job of capturing the zeitgeist of global financial affairs, but there’s so much packed into every issue (and enough to do around our shop) that sometimes all we see are the covers. But we have to admit we’re disappointed in The Economist for the week ended July 31st. The “Free Money” theme is at least four months too late!

Stimulus Gone Wild!

Market perma-bulls deserve high marks for their persistence, yet, despite all that’s transpired in 2020, their case is exactly the same as six months ago: Extreme stimulus won’t “allow” a significant stock market drop, nor any further economic deterioration.

Keep An Eye On What Your Stocks Will Buy

.jpg?fit=fillmax&w=222&bg=FFFFFF)

News that the Bureau of Labor Statistics may have undercounted the May unemployment rate by six percentage points should remind investors of the danger of taking government economic reports too seriously. Regardless of the figure, though, unemployment is no doubt near its peak for the downturn.

NASDAQ Goes “Parabolic?”

From now ’til eternity, bullish market pundits will always be able to argue that the global spread of the coronavirus “caused” the current global recession and bear market. While the pandemic was certainly the final catalyst, these pages had been detailing the emerging cracks for over a year.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue