Fed Policy

Over-Stimulated?

We can’t count the number of times in the last week we’ve heard analysts worry about “what the Fed might know that we don’t.” In the words of John McEnroe, “You cannot be serious!”

The Easy Fed and the “Other” Inequality

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Super-easy monetary policy has been blamed for the rise in income and wealth inequality in recent years, and more recently we’d fault the Fed for performance inequality within the stock market.

Central Planning Makes A Comeback

Bulls who fashion themselves as contrarians argue that the public is nowhere near as infatuated with the stock market as they were in the late 1990s. It may come as a shock to our readers, but we agree with them.

Liquidity Overflow!

Based largely on the bearish trends in our monetary and liquidity measures, we were correctly negative on stocks throughout most of 2018. It’s therefore especially painful for us that 2019’s market rebound has been credited almost entirely to the “pivot” in most of those measures.

The Alternate Ending?

After last year’s spectacularly successful pivot following the December 2018 plunge, the thinking is that future rate hikes are the bull market’s only threat. Perhaps that will be the case; the belief is certainly well-supported by postwar U.S. economic history, but it also reveals a shocking lapse in short-term memory.

Waiting For The Stimulus To Trickle Down...

Last year the Federal Reserve dumped historic stimulus onto a full-employment economy and an already richly-valued stock market. The stock market obviously loved it.

Monetary Musings

Among six major monetary gauges, five are now graded bullish, compared with just three a few months ago, and zero at the end of 2018.

Making Money In The Money-Losers

Despite an economy operating “beyond” full employment for the past seven quarters, more than one-fourth of the companies in the Leuthold 3000 universe are losing money on a 12-month trailing basis. The Fed has subsidized what’s truly become irresponsible behavior.

The Fed Subsidy Is Wearing Off

Earnings results for the second quarter have so far "beaten" expectations (as they always seem to), but that hasn’t changed the calculus for Small Cap companies. About one-third of them have negative earnings over the last twelve months.

When A Cut Is Not Enough

The recent rate cut managed to bring policy uncertainty back into the market by two seemingly harmless words—”mid-cycle adjustment.”

Tariff Man Tampers With Toppy Market

Beware of those who write about stock market history, especially when they speak of cause and effect. The truth is that the “why” can never be known.

Signs Of Spring For Financials

Signs of spring are popping up everywhere in the Financials sector. S&P Financials was easily the top- performing sector in April and several sub-industries have been bubbling higher in our Group Selection discipline.

On The Cutting Edge—End Of Fed Hikes?

The Fed not only signaled no rate hike for the rest of 2019, but also committed to unwinding its balance-sheet reduction program, starting in May and ending in September. The market took it one step further and priced in a rate cut in the second half of 2019.

The Cycle Is Over If Confidence Fades Further

.jpg?fit=fillmax&w=222&bg=FFFFFF)

The “Expectations” component of the Consumer Confidence survey has been wobbly in the last few months, but the latest report, released on Tuesday, showed the first meaningful hit to consumers’ “Present Situation” since the stock market first began to struggle 14 months ago (Chart 1).

Assessing The Cyclical Risks

With all the excitement over the Fed’s shift in rhetoric and the excellent subsequent market action, there’s a danger of losing sight of the broader cyclical backdrop for U.S. stocks. Remember, the economy is still operating beyond government estimates of its full-employment potential, and it’s not as if the Fed has actually eased policy—as it did successfully at a similar late-cycle juncture in the fall of 1998 and (ultimately unsuccessfully) in the summer of 2007.

It Wasn’t Powell Who Panicked

The Fed’s “Christmas capitulation” seems to get most of the credit for the stock market rebound, but we’re not exactly sure how, or even if, the Fed capitulated at all.

Did The Doves Swoop In And Save The Day?

Just a few months ago, Fed Chairman Jerome Powell boasted a reputation as a straight-talking, sound-money banker.

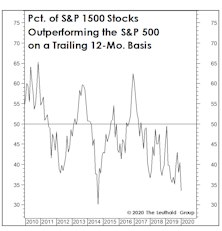

Odds Of Outperforming?

In September, the percentage of S&P 500 stocks outperforming the S&P 500 index fell to 40.7%, the lowest reading since mid-2012. Breadth has followed a conventional path over the course of this unconventional bull market; in the current phase, the odds of outperformance are steadily diminishing.

Beware The Policy “Narrative”

It’s been amusing to watch the narrative surrounding Fed policy evolve as the market has rallied.

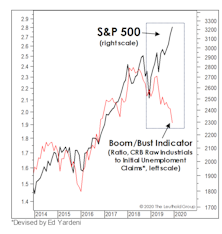

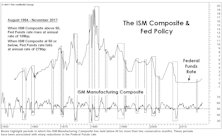

The Chart The Fed Forgot

The Fed has long claimed itself to be “data dependent” while providing less and less information on those data points it considers most relevant. We can’t know what’s on that list, but we certainly know what isn’t: the ISM Manufacturing Composite, which (prior to the current cycle) provided an excellent gauge of the Fed’s policy bias.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue