Of Special Interest ...examining a significantly timely topic

Horse Trading In The Factor Zoo

Smart beta ETFs have become an immensely popular investment tool, attracting billions of dollars in AUM by providing investors with targeted exposure to factors such as Value, Momentum and Quality. Characteristics such as these have been shown to generate alpha over time, and investors understandably wish to have focused positions in these return-generating styles.

Can Smart Analysts Generate Smart Beta?

We assess the effectiveness of using Wall Street analyst opinions as factors in a quantitative stock selection model. Watch for the full report coming next week.

Incongruities In High Quality

Quality is one of the most popular and successful of the equity market’s quant factors. It is intuitively appealing and serves as a useful defensive strategy in falling markets. Low Volatility and Dividend Growth are also defensive factors, while Momentum and High Beta are viewed as aggressive or bullish factors. These offsetting behaviors would seem to make for excellent diversification opportunities in equity portfolios, and for the most part, that is true.

An Earnings Bottom...What's Next?

It seems like it’s been ages since investors have been able to get excited about earnings growth, although our October 21st “Chart of the Week” showed that the S&P 500’s current earnings slump has been unremarkable in both depth and duration.

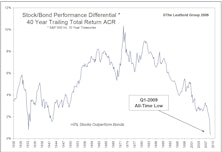

Exploiting Generational Anomalies In Stock vs. Bond Returns

There are two important conclusions about the historical relationship of stock vs. bond returns:

- The current stocks vs. bonds performance differential, over both very short and very long time periods, is at or near historical extremes in every timeframe we examined. This suggests that we are at the threshold of a major (but temporary) market anomaly.

- Historically, periods when bonds have outperformed stocks over very long timeframes have proven to be very opportune times to shift out of fixed income assets and into equities.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue