Inside The Stock Market ...trends, cross-currents, and outlook

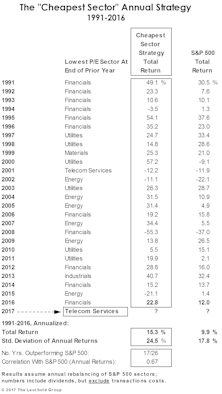

Low P/E Sector: Annual Results

Table 6 summarizes annual sector selection and accompanying performance for the “Cheapest Sector” strategy back to 1991.

2016’s Industry Group Dream & Nightmare Portfolios

For nearly three decades The Leuthold Group has tracked its hypothetical industry group portfolios composed of the previous year’s “Dreams” (best performers) and “Nightmares” (worst performers).

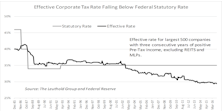

Impact Of Lower Corporate Tax Rate

A stock market wild card in 2017 is the potential for a significant reduction in the corporate tax rate. President-elect Trump’s desire to lower corporate taxes, if implemented, would have multifaceted impacts on businesses.

Putting “Our Spin” On The Positive Spin

Bull markets seem to create their own moods that lead to fundamental developments being viewed in a mostly favorable light.

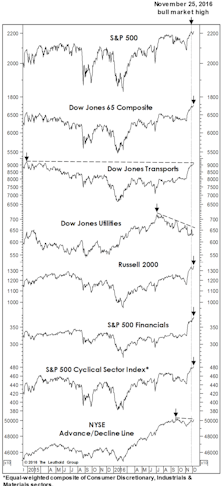

Stock Market Observations

We revisit our “Red Flag Indicator” of prior bull market tops versus today. Usually most of these internal market measures will deteriorate in advance of the final bull market peak. At the latest S&P high, three of the seven leading measures had raised Red Flags, by not confirming, but two of them (DJ Transports and the NYSE A/D Line), are within just ticks of new bull market highs.

Acting Like A “New” Bull Market?

With DJIA and S&P 500 losses in the 2015-16 decline limited to less than –15%, there’s no way we’d argue the episode represented a completed cyclical bear market (and we said so at the time).

Are Bonds Doing Janet’s Job?

One of our most reliable stock market liquidity indicators decided not to wait for Janet Yellen to formally hike interest rates later this month.

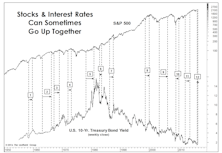

Rising Rates: Not Always A Death Knell

While the Dow Jones Bond Indicator has stood the test of time, history shows that rising bond yields are not always a bearish stock market phenomenon.

Policymakers’ Shell Game

We considered the launch of the QE tapering program in January 2014 as the formal onset of the Fed’s tightening campaign, and that view seemed to be on the mark when High Yield bonds, and then stocks, unraveled over the next couple of years—although the final losses in the DJIA and S&P 500 fell short of what we expected.

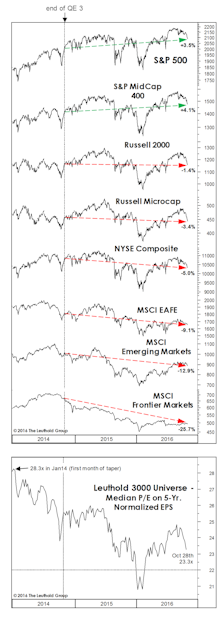

America’s Already First...

Thanks to the U.S. dollar’s recent spike, foreign equities in dollar terms declined during November while the U.S. markets were celebrating a Trump victory. Thirty-nine of the 49 MSCI country indexes are in bear market territory from the perspective of a dollar-based investor.

Does Returning Cash Crowd Out Capex?

Companies are returning cash to investors at a level never before seen. Does the historically high level of cash being returned to shareholders crowd out the use of cash elsewhere? One wide-spread concern is that by shelling out cash through dividends and share buybacks, companies are spending less on capital expenditures. Is that a real concern?

Calendar Effect On Earnings-Release Day Price Movement

Earnings season is not only important for fundamental investors, it can be equally so for quant managers. For quants that incorporate fundamental data, like us, historical trends and changes in consensus estimates may weigh heavily on model output.

Goodbye ZIRP, Hello WIRP

Allow us to put forth yet another theory for this season’s plummet in NFL television ratings: Fed watching is back!

Has The Fed Already Hit Stocks?

One never appreciates what he or she has until it’s gone. In our case, during the many years it was freely available, we failed to appreciate the zero interest rate. Now that it’s gone, we already feel pressured to join a game where we (and very few others) have any edge: Fed-watching. Our real edge is that we recognize this.

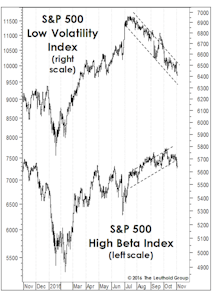

The “Low Vol” Unwind: Just The Beginning?

In mid-summer we suggested that attaining new market highs would probably require a rotation away from the long-time Low Volatility market leaders and into High Beta areas like Technology and industrial cyclicals.

Four Thousand Companies Can’t Be Wrong!

Scott Opsal’s “Chart of the Week” in mid-October suggested the seven-quarter S&P 500 earnings recession may have run its course.

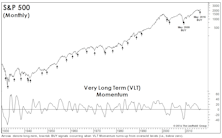

Not Much “Lift” From VLT “BUY”

In the June Green Book, we professed some skepticism surrounding the long-term, “low-risk” BUY signal for stocks that was triggered at the end of May by our Very Long Term (VLT) Momentum algorithm (also known as the Coppock Curve).

Lack Of Confidence Has Been Greatly Exaggerated

While this 7 1/2-year bull market has failed to give rise to anything resembling the equity culture of the late 1990s, we think it’s a stretch to claim—as dozens of commentators over the past five years have—that this bull is “the most hated” in history.

A New Take On The Labor Market

Politicians bemoan the lack of “good-paying jobs,” but what’s the current perspective of employers? According to a simple measure developed by economist Edward Renshaw many decades ago, employers see a lack of “unused labor capacity” in the U.S. that should lead to yet another year of disappointing GDP growth in 2017.

Wanted: A Wrong-Way Economist

The travails of active equity managers have been well-documented throughout the year, but there’s been little attention paid to the 2016 plight of economic forecasters—especially ones unlucky enough to have been accurate.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue