Inside The Stock Market ...trends, cross-currents, and outlook

Technical Troubles

In 2023, the U.S. economy has continued to grow despite recessionary warning flags, while stocks have shrugged off the most aggressive monetary tightening since Paul Volcker’s reign. Impressive.

Bull Or Bear? Our Cop-Out Answer

The recent rebound in Small Caps still leaves their entire gain off the lows at a fraction of what a typical bull would have delivered. In the long term, that’s an opportunity; in the short term, it’s a warning.

Fasten Your Seatbelt

Richard Russell, who wrote Dow Theory Letters for 58 years until his death in 2015, would sometimes say, “The stock market always does exactly what it is supposed to do, but never when.”

A Plot Twist In The “Tale Of The Tape”

We still believe the U.S. economy will suffer a recession in 2024, and it’s also possible the official business-cycle peak will be identified (long after the fact) as having occurred in one of these final months of 2023.

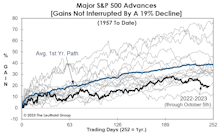

A Low-Key Anniversary...

We think Small Caps’ severe underperformance is an economic distress signal that’s been amplified throughout 2023 by the action of financial stocks—and banks in particular. On the same day the Russell 2000 violated its 2022 bear market low, the S&P Financials sector came within 4% of doing the same.

Housing: Shelter In Place

At the pre-COVID business-cycle peak of February 2020, the qualifying income for a median-priced home was $47,232. As of September 2023, that level had surged exactly $60,000—to $107,232! How many households have enjoyed a pay boost of even one-third that amount in the last four years?

It Won’t Be Long Now…

Stock market-liquidity is critical piece of the “weight of the evidence,” and its continued deterioration is a reason the Major Trend Index couldn’t break above its Neutral zone thus far in 2023—even at mid-year, when the Technical backdrop was at its strongest (… which was not very strong at all).

Putting The “Sahm Rule” To The Test

In January, the “inventor” of the yield-curve indicator—Campbell Harvey of Duke University—suggested that the inversion of the 10Y/3M spread was “flashing a false signal,” and a U.S. recession would be avoided.

Good Job Market News Of A Different Kind

The move higher in the unemployment rate is ominous, but in the last couple of quarters there’s been a surprising development that could—if it continues—cushion the blow to profits from a downturn.

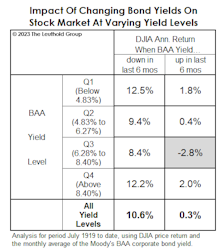

Bonds: What’s Old Is New Again

We’re surprised the recent surge in bond yields hasn’t produced any high-profile casualties (… well, aside from three of the four-largest U.S. bank failures in history—but that was back in March).

More Small-Cap Troubles

With Small Caps still down 30% from their cycle peak, and now undervalued on many of our measures, we’d expect them to be more “levered” to a continuing economic expansion than the more diversified and internationally-exposed Large Caps. But no.

Valuation Checkup

With the S&P 500 back to near 10% of its January 2022 all-time high as of early November, it might be worth considering the bear market in time since mid-2021.

Pause, Or Paws?

The one-year anniversary of the 2022 bear-market low occurs on October 12th, yet—after all this time—we’re not confident enough to declare it as the bull’s first birthday.

We’re interested to see whether or not CBNC breaks out new baseball caps for the occasion, as they did in the late 1990s for “Dow 10,000.”

Feeble Bull Or Hibernating Bear?

At last October’s lows, we had yet to see any manner of economic, monetary, and valuation “reset” that would clear the path for a resilient cyclical bull. And, in the 51 weeks since that bottom, U.S. economic, monetary, and valuation conditions have only deteriorated further.

Yelling “Fire” In A Crowded Theater?

The latest market down-leg triggered one of our short-term breadth oscillators into super-oversold territory. While “oversold” may sound bullish to most contrarians, when SPX becomes as internally weak on a 10-day basis as it did in early October, there’s usually another shoe to drop.

Groupthink?

Question: While hopes for an economic soft landing have ticked up a bit, the consensus view among economists still seems to be for a recession in 2024. Does having so much company concern you?

Response: Of course!

Yields Up, Economy Down?

Based on past experience, steepening in the curve from deeply inverted levels, as it has done recently, means a recession should be fairly close at hand. Worse, the fact that this move is of the “bear-steepening” variety should further depress economic prospects over the next 12-18 months.

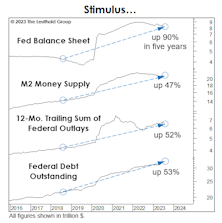

Has The Tsunami Of Stimulus Been Worth It?

Federal outlays, federal debt, and M2 have each jumped ~50% in five years, while the Fed’s balance sheet soared by 90%. The “reward”: Real GDP cumulative growth per capita of 1.6% per year (a good chunk of which will be reversed during a recession).

Can The Treasury Afford A Recessionary Bear?

In recent years, stock market swings have become a more reliable predictor of tax receipts than the economy, itself. If both were to roll over, deficits in the “teens” as a share of GDP—and Fed efforts to deal with them—are unavoidable.

The Small-Cap Year That Wasn’t

Consensus calls for a recession in 2023 have been off the mark, but that doesn’t mean all recession-oriented portfolio bets have necessarily gone awry.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue