Valuations

Speculating In “The Nebs”

One measure of a bubbly bull market is the degree of speculative fervor embedded in the prices of companies with nebulous, indeterminate, or even nonexistent intrinsic values. Since the bear market low in March 2020, speculative manias have evolved in a menagerie of asset classes including Innovators & Disruptors, SPACs, meme stocks, crypto currencies, and NFTs. Based on the breadth of valuation extremes across numerous and diverse assets, this bull market may rank second to none.

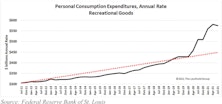

Discretionary Durables: A Bubble In Fun

Extremely loose monetary and fiscal policies during the pandemic have created distortions and disequilibria throughout the economy. The most visible bubbles may be in financial markets, evidenced by the boundless valuations applied to visionary startups and the speculative fascination for digital assets of all types. This report examines a bubble of a different kind; not a financial bubble but rather a real-world bubble in “fun”. Producers of recreational goods are flourishing during the pandemic, posting massive sales gains and a tripling of net income, yet selling for miniscule valuations.

Research Preview: Discretionary Durables

While retail spending has boosted staples and durables alike, we believe that discretionary durables have been the prime beneficiary of changing lifestyles and spending patterns, with skyrocketing sales and inventory outages that may not reach equilibrium even in 2022.

Long-Term Returns: You Wanted The Best, You Got The Best!

In a possible sign we’re not getting enough oxygen at current valuation altitudes, we decided to replace the usual mean-reversion technique with a much friendlier approach that we’ve dubbed “maximum attraction.”

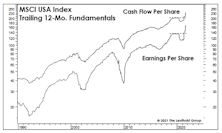

Valuations And The Earnings Recovery

Analysts at Standard & Poor’s will soon confirm what’s been known for several months: The earnings downturn associated with the COVID recession was the shallowest and shortest of any recession-related EPS decline.

Not Overthinking Small Caps

There are some positive cyclical influences for Small Caps, like higher inflation and deeply negative real interest rates. But in our minds, the valuation spread versus Large Caps is more important.

What’s Your “Number?”

Those in their peak earning years (40s and 50s) who’ve also enjoyed the stock market’s windfall gains are very likely to have seen their annual expenses climb much higher than the Consumer Price Index over the last several years.

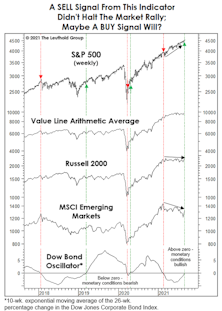

Let Us Add To The Bullish Cacophony

It’s been a heck of a stock market year, and there are still four months left. What else could go right? Monetary conditions, for one thing—at least as proxied by our Dow Bond Oscillator (DBO).

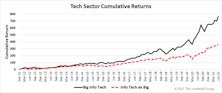

Big Time

Market environments are driven not just by industry preferences, but also by a bias toward the very largest companies. We have developed a new set of groups composed of the 10 largest companies from each sector. With several of these baskets sporting positive rankings, we felt a closer look was in order.

2020 Post-Mortem

This summer marks the first anniversary, not of the COVID-19 stock-market low, itself, but of the much belated “confirmation” of that low.

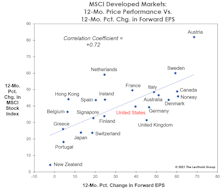

The Global EPS Rebound

For years, we’ve noted the increasing valuation gap between domestic and foreign stocks. And for years, we contended that the most likely catalyst for a narrowing of that gap would be a recession-induced cyclical bear market in stocks. Evidently the 2020 bear market was not big enough to do the job.

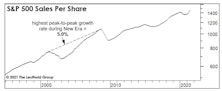

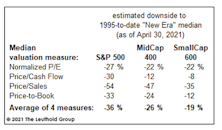

New Era Valuations?

We understand the various rationale for the upward shift in equity valuations seen over the last quarter century or so. Unfortunately, wiping away all market history prior to 1995 does not make stock valuations appear significantly less inflated.

Young Bull, Old Threat

By our count, the current bull market is the 13th of the postwar period. The 88% gain achieved by the S&P 500 in less than 14 months already places this bull sixth in terms of cumulative gains. We considered it a hindrance that this bull commenced from higher valuation levels than any other in history. Instead, they seem to have provided a head-start.

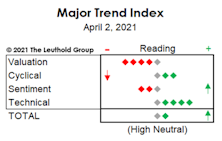

Introducing The “New” MTI

We launched a revamped version of our Major Trend Index. The objective of the new methodology is to increase the flexibility, and even the subjectivity of the MTI. This approach recognizes the “subjective reality,” without forcing us into the tedium of re-weighting sub-factors if they become more or less critical as market dynamics evolve.

Research Preview: The Experiential-Reopening Trade

A strong argument can be made that experiential consumer services was the economic sector hardest hit by the pandemic lockdown. Cruise ships were forbidden to sail, restaurants and theme parks were closed, and air travel and hotel occupancy dwindled—all in an attempt to minimize personal/public interaction. The stocks of experiential companies took a beating in March 2020.

Podcast #31 - Valuation Extremes: Here Be Dragons

Top decile valuations are often the result of unduly positive investor sentiment that leads to inflated multiples. Bullishness comes in varying strengths: optimism, enthusiasm, exuberance, and, at the extreme, the mania of crowds.

A Flight Of Wee Dragons

.jpg?fit=fillmax&w=222&bg=FFFFFF)

In our mid-month Of Special Interest, “Valuation Extremes: Here Be Dragons,” we examined valuation outliers as a measure of market sentiment. The hypothesis was that exuberance is reflected in investors’ willingness to hold stocks priced on an aggressive “vision” of the future; companies that are either habitually unprofitable or trade at a Price/Sales ratio above 15x.

Valuation Extremes: Here Be Dragons

Top decile valuations are often the result of unduly positive investor sentiment that leads to inflated multiples. Bullishness comes in varying strengths: optimism, enthusiasm, exuberance, and, at the extreme, the mania of crowds. Because bullishness manifests itself in aggressive valuations for speculative companies, we believe the prices being applied to such companies - for which intrinsic value is dependent on a future that looks significantly different than today - are an excellent measure of investor sentiment. In that spirit, we examined past cycles of extreme valuations with the goal of understanding how they relate to investor sentiment and what they might tell us about market conditions and relative returns.

Bond Yields “Take Down” An Old Favorite

The “lower for longer” interest-rate thesis propped up the S&P 500 Low Volatility Index for more than a decade. Rising bond yields have since helped drive this former darling to an 18-year relative-strength low. Yet, assets in the S&P Low Volatility ETF are still five-times larger than its High-Beta counterpart.

If You Like TINA, You Should Love “SAMARA!”

Equity investors have had a multi-year love affair with TINA—the belief that “There Is No Alternative” to stocks in a world of ridiculously-low interest rates. This TINA romance has carried on so long that the S&P 500 is nearing valuations last seen in the Tech bubble’s final inning. If the fling with TINA has become prohibitively expensive, we’d like to introduce “SAMARA.”

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue