Valuations

The Many Faces Of Mo

Momentum is one of the most widely accepted alpha-generating factors, used by quantitative and fundamental managers alike. Its biggest drawback, however, is high turnover. Herein we explore momentum from the perspective of sector weights.

The Case Of The Disappearing Value Premium

Market history teaches us that investors behave differently in groups than they do as individuals.

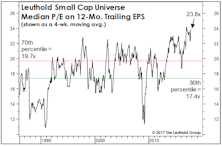

Small Cap Valuation Check

We don’t have a strong capitalization-bet recommendation, other than to remind readers that Small Caps have been especially responsive to the favorable seasonal window that began November 1st (and which extends through April 30th).

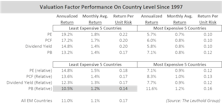

Valuation-Based Country Selection/Rotation

Despite cyclicality, over the longer term, investing in lower valuation countries ekes out better performance in an EM portfolio, and Dividend Yield showed the most consistency in terms of value factor effectiveness.

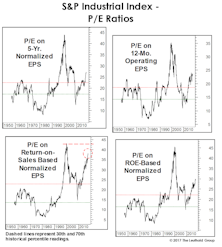

Dialing In On Downside Risks

Question: Your “Estimating The Downside” section shows the S&P 500 would lose 26% if it reverts to its 1957-to-date median valuation level. The downside estimate for the S&P Industrials Index, however, is almost -40%. Why such a huge difference?

How To Double Your Money In Ten Years

Before the markets punish an irresponsible act, they must first reward it.

A Harbor In The Tempest

Our Major Trend Index (MTI) recently fell from “positive” toward stocks to a “neutral” reading, leading us to trim bullish equity positions in our tactical portfolios.

Valuation-Based Country Rotation: EM Vs. DM

Many studies have evaluated momentum factors for over/underweighting country exposures within a portfolio, but few have considered valuation factors for country rotation within the Emerging Market space.

A Contrarian “Late-Cycle” Play?

The Amazon Effect masks both the underperformance of the average Discretionary stock and the relative value that’s been reestablished across the sector. “Discretionary ex-Amazon” is a better contrarian pick than Energy.

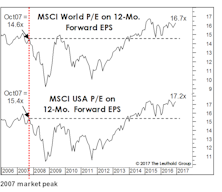

Global Valuation Checkup

Foreign equities beat the U.S. in the first quarter, but the performance gap that’s opened up since the 2007 market highs remains astounding. While foreign equity valuations (especially within EM) have rebounded from February 2016 lows, the bounce has done little to close the enormous P/E discounts relative to the U.S. market.

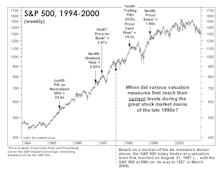

The Valuation “Time Clock” Revisited

Based on a median of six measures, today’s S&P 500 valuation profile equates to the one prevailing on August 31, 1997. From there, the S&P 500 rallied >60% over the next 2 1/2 years before peaking. However, the same can’t be said of valuation readings for the “typical” or median stock.

What’s Ailing Small Caps?

While the Russell 2000 loss during the 2015-16 correction was almost double that of the S&P 500, the decline did not fully erase the P/E premium Small Caps have enjoyed since the middle of last decade. The premium might need to be entirely erased before a multi-year Small Cap leadership cycle can begin.

Estimating The Upside: Another Angle

A look at the potential upside for the median S&P 500 stock, based on the theory that each of four valuation ratios reaches its individual all-time high set during the last phase of the 1990s’ market mania.

Trump Inherits Poor ‘Initial Conditions’

We think that stocks in Trump’s current term will fall short of Obama’s gains, mostly reflecting a valuation starting point that’s almost twice as high as Obama’s was. “Managing expectations” doesn’t seem like Trump’s style, but in the case of the stock market it might not be a bad idea.

Apologizing in Advance for Trump

While Wall Street is extremely well represented in the new administration, we doubt that Wall Street’s performance under Trump will come close to that enjoyed under Obama.

An Obligatory Rant Over High Valuations

We remain cyclically bullish, but it would be intellectually dishonest to try to make a serious valuation case for the stock market here.

Safety In Numbers?

The S&P 500 closed the first week of January at a new cycle high, up 9.2% from the pre-election low made on November 4th.

“Changes In Attitudes, Changes In Latitudes”

The above caption—and Jimmy Buffett song title—comes from the “View From The North Country” section in the first-ever Green Book published in November 1981. Not much has changed in 35 years.

Has The Fed Already Hit Stocks?

One never appreciates what he or she has until it’s gone. In our case, during the many years it was freely available, we failed to appreciate the zero interest rate. Now that it’s gone, we already feel pressured to join a game where we (and very few others) have any edge: Fed-watching. Our real edge is that we recognize this.

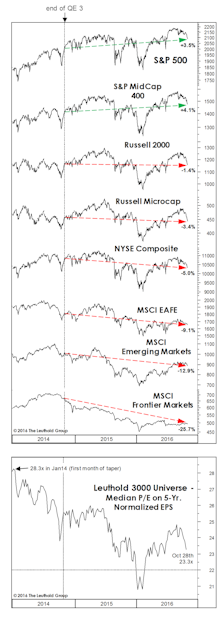

Small Caps: Growing Into Their Valuations

Fed tapering of its QE3 asset purchase program ended two years ago this month, yet we don’t believe this episode has received appropriate recognition for the role it’s played in the relatively flat stock market environment that’s followed the onset of tapering in January 2014.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue