Recession

Recession Dashboard Update—Low Recession Risk

The stock rally and associated wealth effect make an imminent recession less likely (data that corroborates our Up/Down Earnings figures). Yet, things can change quickly when so much is riding on the market. Employment is still the biggest threat.

Slowdown Or Recession? Watch The S&P 500 Index!

Uncertainty surrounding Trump’s second term and the risk of escalating tariffs have shifted market focus from inflation to growth, raising fresh concerns about a potential recession. Our updated Recession Dashboard shows a delicate balance, with risk now slightly above 50%—driven largely by weakness in equities and full-time employment. While some indicators have improved, the market remains the most important signal to watch. A sharp selloff could tip the economy from slowdown into recession territory.

Three Themes To Watch: Recession, Inflation, The Election

Is the market overreacting to recent economic data? Concerns about a growth slowdown are replacing the optimistic outlook of early 2024. Our Recession Dashboard shows increased risks, with notable declines in housing, employment, and consumer confidence. Despite this, equity and credit markets remain resilient. As we navigate these uncertain times, discover how upcoming elections and potential economic policies could shape the future.

A Delayed Day Of Reckoning?

Today, the recession / no-recession call dominates daily market debate probably more than any time since the spring of 2008 (when the economy had been in recession for 4-5 months). We fully expect the U.S. economy to roll over in the next several months.

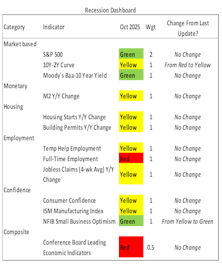

Soft Landing Or Recession? A Dashboard Update

The weight of evidence clearly leans more toward a recession, but the wild card is the recent dovish turn of global central banks, which can significantly boost confidence from investors, consumers, and businesses.

Goodbye Inflation, Hello Recession?

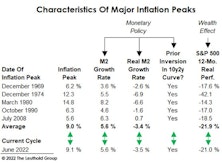

Unlike the five prior cycle peaks, this year’s inflation peak materialized during an ongoing economic expansion. That implies the “post-peak” monetary policy has never been tighter than today—making a soft landing even more improbable.

How This Year’s Inflation Peak Differs From Its Predecessors

Our studies of economic and stock market history are meant to provide perspective, not an investment roadmap. But occasionally a current trend will resemble the past so closely it’s eerie.

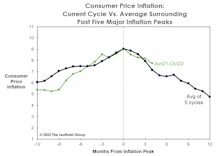

Take the current inflation cycle. If (as we believe) June’s CPI inflation rate of 9.1% represents the peak for this business cycle, then many of its characteristics have lined up almost perfectly with the “average” of past inflationary episodes.

The World As Powell Sees It

When the economy falls into recession, labor market measures will be among the last to tell us. We can’t resist watching them anyway, for two reasons. First, we know that the Fed’s self-proclaimed data dependency is unduly reliant on lagging data points, like the monthly employment report. We want to see what the policymakers are seeing, even if that sometimes means using the same, fogged-up rearview mirror.

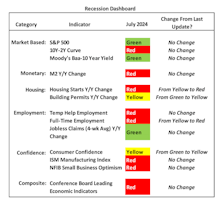

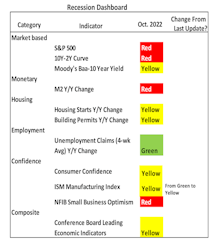

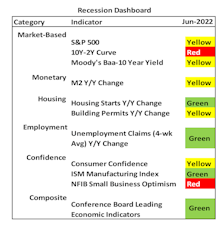

Recession Dashboard Update—More Deterioration

The latest ISM Manufacturing numbers resulted in a downgrade to that factor from “green” to “yellow.” Unemployment claims is the lone component with a green light on the dashboard. Overall, the various measures we track suggest the risk of a “real” recession is high—better than 50%.

#51 - Yield Curve Inversion

Our recession indicators have continued to deteriorate. Given the stagflation backdrop, the Fed’s tightening cycle is very likely to end in a recession.

Recession Dashboard Update—Real Recession More Likely Than Not

Our recession indicators have continued to deteriorate. Given the stagflation backdrop, the Fed’s tightening cycle is very likely to end in a recession.

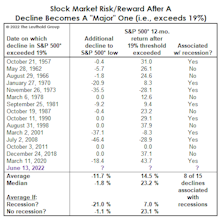

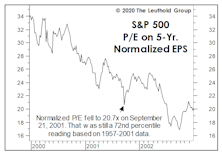

“Recessionary” Valuations?

The bear was a mere cub back in March when we examined the historical record of buying S&P 500 dips in the -10% to -12% range. “Blindly” buying them turned out to have mediocre returns, but we illustrated that the positions of various business-cycle indicators could help one determine whether or not catching the proverbial “falling knife” was warranted.

Recession Dashboard Update—More Warning Signs

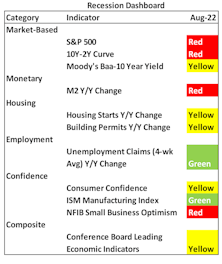

Overall, there are now more warning signs, but it still doesn’t suggest a recession is imminent.

Does An Economic Rebound “Inoculate” The Stock Market?

The 2020 decline exhibits a strong resemblance to the “incomplete” bear market of March 2000-September 2001—in that neither decline sufficiently deflated the extreme valuations of the preceding bull, and each was followed by an immediate rebound in reliable valuation measures to top decile levels.

Back Breaker?

With the wavering state of consumer and business confidence, even a modest stock market correction of 8-10% might deliver the fatal blow to confidence—and therefore to the U.S. economic expansion.

Cross-Asset Cross Currents—All About The Recession Call

September was an emotionally exhausting month for investors as reversals in major themes produced wide-ranging repercussions. Movements in various markets have been increasingly tied to bonds—the market that is most sensitive to recession outlook.

Recession Evidence: How Much Is Enough?

Over a 12-month horizon, we now believe a U.S. recession is very likely, but aren’t confident enough to make the call when the forecast window is cut in half. Second-half stock returns could be decent if the business-cycle peak is still a year away. Then again, there’s peril in waiting for “too much” confirmation of recession.

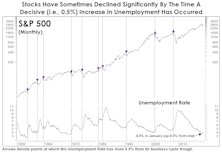

Unemployment And The Point Of No Return

We’ve done extensive work on the yield curve, but until now had entirely overlooked an employment-based recession indicator that’s lately come into focus.

The Rate Hike Carnage Is All Around Us

Taking a cue from the White House, today’s market pundits seem more prone to declarative, unsubstantiated statements than we can ever remember.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue