Articles by Chun Wang Director of Multi-Asset Strategies

Inflation Picture Is More Muddled

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Both the headline and Core CPI were largely in line with expectations. The dollar’s recent weakness has served to support higher inflation as well as easier financial conditions. Our Scorecard suggests that the possibility of inflation staying persistently high is increasing.

Risk Aversion Index: Stayed On “Lower-Risk” Signal

Seasonality is still an advantage, and financial conditions have eased. Within fixed income, we remain favorable toward both Treasuries and higher-quality investment-grade corporate bonds. We maintain a neutral stance on the yield curve.

Soft Landing Or Recession? A Dashboard Update

The weight of evidence clearly leans more toward a recession, but the wild card is the recent dovish turn of global central banks, which can significantly boost confidence from investors, consumers, and businesses.

Inflation- In Line But Sticky

Both the headline and Core CPI were in line with expectations.

Sticky ex-Shelter CPI has rolled over and EM inflation surprises are negative now.

Disinflation remains the dominant theme but some inflationary pressure can be quite sticky.

Risk Aversion Index: Stayed On “Lower-Risk” Signal

While seasonality remains favorable, the risk of a severe recession looms large in the medium term. We are favorable toward high-quality corporate credit and Treasuries.

2022 Surprises & 2023 Time Cycles

We updated our time-cycle composite for 2023. Overall, while the patterns suggest a year of smooth sailing for most markets, the actual paths forward could be much more volatile.

Inflation—Giving Way To Recession Concerns

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Both the headline and Core CPI were weaker than expected. Wealth effect and employment indicators also suggest lower inflation. Inflation pressure should ease further as recession becomes the dominant concern.

Risk Aversion Index: Stayed On “Lower-Risk” Signal

The market has responded quickly to global central-bank pivots, and favorable seasonality can carry the rally a bit further in the near term. However, the risk for a severe recession still looms in the medium term.

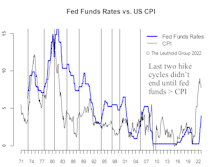

Fed Funds Rate Above The CPI—Inflection Point Likely

Stock market bulls hope for an end to the tightening cycle in the not so distant future. However, the last two rounds didn’t end until the fed funds rate was raised above the prevailing rate of CPI.

Risk Aversion Index: A New “Lower-Risk” Signal

Given depressed market sentiment and favorable seasonality, near-term prospects look better for risky assets.

Six Themes Around A Full Yield-Curve Inversion

The main yield curve drivers—fiscal and monetary policies—might be suggesting a steepening move is coming soon, while bank stock performance may also be hinting at a turn in the curve. However, a durable selloff in the U.S. dollar would be needed to support a steeper yield curve, so the tightening pain could last a while longer.

Inflation Should Ease Fairly Soon

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Both the headline and Core CPI are a tad hotter than expected. While shelter contributed the bulk of the upside surprise, it’s set to slow in the coming months. Our Scorecard indicates that inflation pressure should begin to ease a bit fairly soon.

Risk Aversion Index: Stayed On “Higher-Risk” Signal

The market seems very eager to price in peak central-bank hawkishness; but only time will tell if the BoE pivot marks the beginning of a global pivot cycle. Caution is still recommended.

Midterm Elections—Not A Typical Year

While midterm elections are not typically big market movers, there is really nothing typical about 2022.

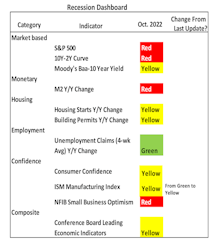

Recession Dashboard Update—More Deterioration

The latest ISM Manufacturing numbers resulted in a downgrade to that factor from “green” to “yellow.” Unemployment claims is the lone component with a green light on the dashboard. Overall, the various measures we track suggest the risk of a “real” recession is high—better than 50%.

The Great British Pivot

The latest BoE and RBA pivots fueled the market’s hope that global central-bank hawkishness has possibly peaked. We believe the market is likely to be lured by the prospect of a Fed pivot in the near term, only to be disappointed as that hope fades away.

Risk Aversion Index: Stayed On “Higher-Risk” Signal

The risk of a policy error is the top concern as the Fed doubles the pace of Quantitative Tightening, even with the U.S. technically in a recession. Caution is recommended.

Fed-Pivot Watch—Pivot Pushed Further Out

Since our July report, market action felt like the pivot had already occurred. However, according to our latest update, numerous measures have moved away from levels that would support a pivot. In other words, the eagerly-awaited Fed pivot has been pushed further out.

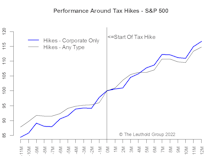

Inflation Reduction Act—Corporate Tax Hike Implications

We take a look at the impact of past corporate-only tax hikes versus tax hikes of any type (personal income, corporate, capital gains). The gist is, there isn’t much difference at all.

More Signs Of Peak Inflation

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Both the headline and core CPI are better (lower) than expected. We see more signs of peak inflation as oil prices, supply chain issues, wage pressure and capacity utilization start to moderate.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue