Macro Monitor

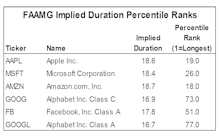

Do You Know Your Stocks’ Duration?

Most people agree that growth stocks have longer duration than value, but few bother to back this up with numbers. Our implied equity-duration study says the conventional wisdom is right: Growth stocks do have longer duration. But... the devil is in the details.

Risk Aversion Index: Stayed On A “Lower Risk” Signal

The talk of taper has started to resurface. In this context, higher inflation might become a negative for credit. For now, we remain favorable toward TIPS but turn cautious toward credit.

To Whom This May Concern

Economic numbers were red hot in April but a funny thing happened when the awesome data rolled in—bond yields actually went lower. Expectations have trended upward, and “whisper” numbers have set the bars even higher.

Risk Aversion Index: A New “Lower Risk” Signal

The reflation trade continued with higher breakeven rates and lower real yields, a favorable make-up for risky assets.

U.S. Dollar—A 2018 Redux?

The price action in the DXY Index over the last year shows an uncanny resemblance to the 2017-18 period, both in duration and magnitude. Overall, we believe the dollar could strengthen in the near term, but the longer-term bearish trend remains intact.

Risk Aversion Index: Stayed On “Higher Risk” Signal

The reflation theme continues to be supported by the powerful policy mix and a successful vaccine rollout. Within fixed income, we are favorable toward TIPS and short-term high-yield credit.

Reflation Trade Or Real-Yield Tantrum?

The market focus has started to shift from a reflation trade to a real-yield tantrum. We compare the latest real-yield tantrum with four prior episodes where rate increases were driven by higher real yields, while breakeven rates were flat to lower: 2005, 2013, 2015, and 2018.

Risk Aversion Index: A New “Higher Risk” Signal

While mechanical signals generated from extremely low RAI levels can be noisy, extended valuations on most assets suggest we err on the side of caution.

Will The Populist Game Stop?

We look at the recent short squeeze and examine how these populist movements affect the market performance in populist vs. establishment countries, and dig deeper into the regional versus sector effect.

Risk Aversion Index: Stayed On “Lower Risk” Signal

We remain favorable toward credit including investment grade and high yield corporates.

2021 Time Cycle — A Year Of Two Halves

We’ve updated our time-cycle composite for 2021 and it looks like it will be a year of “two halves,” with a low-vol bull-market extension in the first half of the year, followed by a much more volatile second half. This also appears to extend outside the U.S.

Risk Aversion Index: Stayed On “Lower Risk” Signal

We remain favorable toward credit and recommend both investment grade and high yield corporates.

Risk Aversion Index: A New “Lower Risk” Signal

With election risk largely in the rear-view mirror, volatility has come down across most asset classes, contributing to the drop in the RAI.

Popular Trades — No “No-Brainers”

We studied several “popular trades” and there are good reasons to be on board with most of them, but none can be viewed as a no-brainer.

Weight Watcher—Another Look At Sector Valuation

There are numerous ways to measure sector valuation, but we found the simplest one: sector weights. Overall, using simple sector weights, we arrive at the same conclusions about sector valuation as one would using conventional valuation metrics.

Risk Aversion Index: Stayed On “Higher Risk” Signal

We are cautious near term and recommend playing defense through duration reduction within corporate credit (including both investment grade and high yield).

Markets & Election—Any Clear Result Will Do

We believe the worst outcome would be a drawn-out, contested presidential election that ends up in the Supreme Court. We review historical market patterns under several election-result scenarios.

Risk Aversion Index: New “Higher Risk” Signal

Treasuries’ ability to provide downside protection has weakened; a better way to play defense is probably through duration reduction within corporate credit (including both investment grade and high yield).

A New Proposal To The Fed: Buy Bank Stocks!

While most economic numbers have been positive, the fly-in-the-ointment was the latest Senior Loan Officers’ Survey. Banks have tightened their lending standards across the board.

Risk Aversion Index: Stayed On “Lower Risk” Signal

The breakeven rates capture the spirit of the overall risk rally and continue to provide support. The change in the Fed’s policy goals means it will remain accommodative for even longer.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue