Macro Monitor

The Great British Pivot

The latest BoE and RBA pivots fueled the market’s hope that global central-bank hawkishness has possibly peaked. We believe the market is likely to be lured by the prospect of a Fed pivot in the near term, only to be disappointed as that hope fades away.

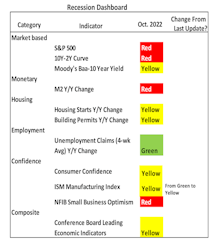

Recession Dashboard Update—More Deterioration

The latest ISM Manufacturing numbers resulted in a downgrade to that factor from “green” to “yellow.” Unemployment claims is the lone component with a green light on the dashboard. Overall, the various measures we track suggest the risk of a “real” recession is high—better than 50%.

Midterm Elections—Not A Typical Year

While midterm elections are not typically big market movers, there is really nothing typical about 2022.

Risk Aversion Index: Stayed On “Higher-Risk” Signal

The market seems very eager to price in peak central-bank hawkishness; but only time will tell if the BoE pivot marks the beginning of a global pivot cycle. Caution is still recommended.

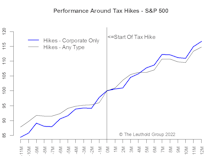

Inflation Reduction Act—Corporate Tax Hike Implications

We take a look at the impact of past corporate-only tax hikes versus tax hikes of any type (personal income, corporate, capital gains). The gist is, there isn’t much difference at all.

Fed-Pivot Watch—Pivot Pushed Further Out

Since our July report, market action felt like the pivot had already occurred. However, according to our latest update, numerous measures have moved away from levels that would support a pivot. In other words, the eagerly-awaited Fed pivot has been pushed further out.

Risk Aversion Index: Stayed On “Higher-Risk” Signal

The risk of a policy error is the top concern as the Fed doubles the pace of Quantitative Tightening, even with the U.S. technically in a recession. Caution is recommended.

Yield Curve Inversion—Count Down To A Bull Steepener

Now that the yield curve has inverted, its dynamic is apt to change from bear flattening (higher rates, flatter curves) to bull steepening (lower rates, steeper curves) fairly soon.

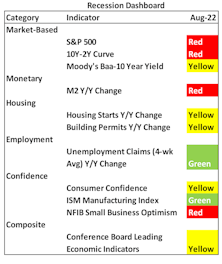

Recession Dashboard Update—Real Recession More Likely Than Not

Our recession indicators have continued to deteriorate. Given the stagflation backdrop, the Fed’s tightening cycle is very likely to end in a recession.

Risk Aversion Index: Stayed On “Higher-Risk” Signal

The risk of a policy error is extremely high as the Fed stays on an aggressive tightening path even with the U.S. in a “technical” recession. Caution is recommended.

Additional Factors

The six-week rally that started mid-June featured advances from AAPL (+25%), AMZN (+30%), and TSLA (+39%), which accounted for one-fourth of the S&P 500’s gain. Despite the recent preference for Value, a spike in interest rates, and the bear market, the index’s concentration in the top-five firms is still near it’s all-time high set in August 2020.

Bond Yields - More Room on the Downside

We have seen the high in bond yields this year and expect a volatile grind lower in rates over the summer: Bearish Treasury positions remain significant, the Copper/Gold ratio fell sharply, and the Citi Economic Surprise Index implies more downside.

Fed Pivot Watch

The late 2018 policy error and subsequent pivot of Chairman Powell’s rookie year is probably the best case-study for today’s pivot debate. Here we evaluate the current status of key pivot triggers and compare them to the readings of late 2018. Given the political environment and backward-looking nature of the Fed, we think the bar is higher for a pivot than the market hopes.

Risk Aversion Index: Stayed On “Higher-Risk” Signal

The risk of a policy error is elevated as the Fed stays on an aggressive tightening path even though growth materially slows. Caution is recommended.

From Tighter Lending To Margin Pressure

Intuitively, what happens in the credit market is usually echoed by lending activities. This was a key concern when the credit market joined the stock-market rout in May. Another big leg up in real interest costs, through higher rates and/or lower growth, will surely create more headwinds for profit margins.

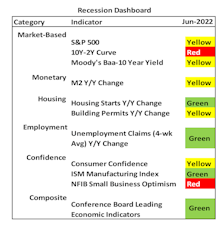

Recession Dashboard Update—More Warning Signs

Overall, there are now more warning signs, but it still doesn’t suggest a recession is imminent.

Risk Aversion Index: Stayed On “Higher-Risk” Signal

While inflation might have peaked, a material slowdown looks more certain as the Fed stays on an aggressive tightening path. Caution is warranted.

U.S. Dollar—Drivers & Impacts

Most U.S. dollar drivers point to a stronger dollar: attractiveness of U.S. assets; policy differentials; real interest-rate differentials; terms of trade; weaker Yuan; and capital flows/hedging activity. Speculative positioning, however, is a negative and suggests the dollar rally might at least take a pause in the near term.

Risk Aversion Index: A New “Higher-Risk” Signal

As long as the Fed stays on the current aggressive tightening path, caution is highly recommended.

Yield Curve—Focus On More Reliable Themes

Predicting a recession is a very tall task, let alone using a single yield-curve indicator with long and highly variable lead time. Instead, we would rather focus on some of the more reliable themes: The macro-policy setting; U.S. dollar; and Bank stocks.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue