Inside The Stock Market ...trends, cross-currents, and outlook

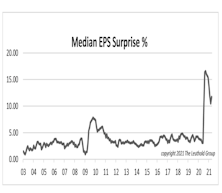

“Surprise” Or “No Surprise?”

Navigating the investment landscape over the past year has been a journey full of surprises. No data other than “earnings surprises” can better demonstrate how unpredictable companies’ financial performance has become.

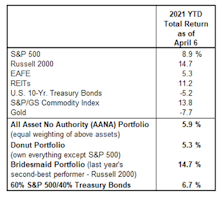

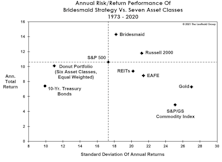

Time For A “Donut” Break?

Despite a resurgence in Small Cap stocks and Commodities, it still feels like an “S&P 500 World” for asset allocators. The financial media remain obsessed with S&P 500 targets, S&P 500 earnings, and S&P 500 stocks. And why wouldn’t they be?

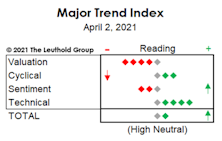

Reading The Short-Term Tea Leaves

The stock market’s technical backdrop remains pretty hard to assail, as evidenced by the current +4 reading on the revamped MTI’s Technical category. But there are a few short-term cracks that bear watching.

Introducing The “New” MTI

We launched a revamped version of our Major Trend Index. The objective of the new methodology is to increase the flexibility, and even the subjectivity of the MTI. This approach recognizes the “subjective reality,” without forcing us into the tedium of re-weighting sub-factors if they become more or less critical as market dynamics evolve.

The “New” MTI Debuts At High Neutral

Read this week's Major Trend.

A Pricey Alternative To The S&P 500?

This month we focus on the valuations of the MSCI USA Index—which is nearly identical to the S&P 500. This is worth following mainly because the folks at MSCI are kind enough to provide us with much longer-term histories of Cash Flow and Book Value Per Share.

EAFE And EM: Long Past Their “Peaks?”

We applied the “Peak Cash Flow” valuation methodology to the EAFE and MSCI Emerging Markets Index and found them both priced at only about one-half of today’s MSCI U.S. multiple. However, the ratios are already above anything achieved during the 2009-2020 global bull market.

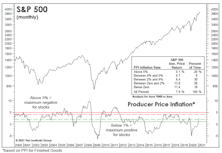

Still Heating Up…

The Fed’s reflationary efforts are showing up everywhere except in the measure that’s engineered specifically to minimize them—the Consumer Price Index. It’s a virtuous circle, until it is not

Putting More And More On Margin

In one year, the bull market has persuaded investors to do something they were reluctant to do near the end of an almost eleven-year bull: Lever Up. Year-over-year growth in Margin Debt reached 49% in February and should catapult far above the “conventional” 50% danger threshold with March’s results.

Snack Time?

As discussed elsewhere in this section, we had a novel idea for asset allocators tired of chasing the S&P 500: Hop off the treadmill and take a “Donut” break!

Equity Financing On The Rise In Some Market Segments

With the equity market at all-time highs and abundant liquidity in the economy, it is probably not surprising to see that CEOs are taking note: Equity issuance is on the rise, especially for small-cap companies.

Bureaucratic Bull

Twenty-one years ago, the bullish bets were on publicly-traded businesses (especially ones with dot-coms after their names). In contrast, today’s bulls seem more beguiled by bureaucrats—the central bankers who, having saved markets and the economy from catastrophe in the last year, are assumed to have mastered the business cycle.

Ruminations On The Fed, Past And Present

If the “Maestro’s” image was dinged from being the “original bubble-blower,” imagine what will happen to Jay Powell’s if stock valuations mean-revert alongside interest rates and inflation over the next few years.

More On The “Rate-of-Change” In Rates…

The liquidity and interest-rate backdrop for stocks has been favorable to such an extreme that we’ve cautioned any minor diminution in this condition could trip up the stock market. On that score, the monetary aggregates and the Fed’s balance sheet don’t pose much concern. On the other hand...

Higher Prices Shouldn’t “Surprise” Us

The Fed has communicated it’s inflation target in uncharacteristically-plain English. Maybe they need to dumb it down more, because it’s the investors in English-speaking countries who have been the most surprised by the recent pickup in the inflation numbers!

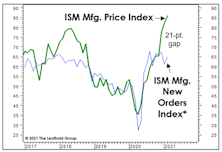

NOPE And NOPE!

The calendar would say the U.S. economic recovery and bull market are very young, yet there’s an astounding array of “late-cycle” activity occurring on both Main Street and Wall Street. In the manufacturing economy, bottlenecks have reached levels that have historically been troublesome for stocks.

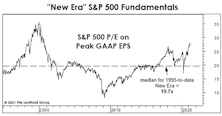

A “New-Era” Look At The Future

Young readers sometimes give us a not-so-subtle roll of the eyes when we discuss any sort of stock market history that occurred before their date of birth, but it takes experience to appreciate that “there’s nothing new under the sun—least of all in the stock market.”

If You Like TINA, You Should Love “SAMARA!”

Equity investors have had a multi-year love affair with TINA—the belief that “There Is No Alternative” to stocks in a world of ridiculously-low interest rates. This TINA romance has carried on so long that the S&P 500 is nearing valuations last seen in the Tech bubble’s final inning. If the fling with TINA has become prohibitively expensive, we’d like to introduce “SAMARA.”

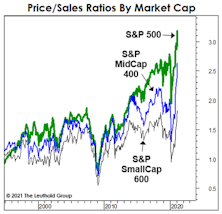

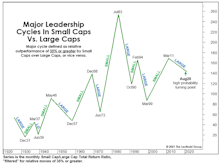

Small Caps: It’s Still Early

Technical analysts continue to be aghast at the relentlessly “overbought” readings generated by Small Cap stock indexes. However, last month we noted that such extremes had previously presented themselves only at the early or middle phases of a Small Cap leadership cycle—never at the end of such cycles.

Bond Yields “Take Down” An Old Favorite

The “lower for longer” interest-rate thesis propped up the S&P 500 Low Volatility Index for more than a decade. Rising bond yields have since helped drive this former darling to an 18-year relative-strength low. Yet, assets in the S&P Low Volatility ETF are still five-times larger than its High-Beta counterpart.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue