Inflation Watch A mid-month focus on inflation via Traditional Indexes, Commodity Prices, and Labor Costs

Inflation Taking A Pause

June inflation is in line with or slightly lower than expectations. The increase in hourly earnings stalled too. So far the recent bounce-back in inflation has not posed a big enough threat to make the Fed policy more hawkish in the near future. Inflation at producers’ level seems to be taking a pause too.

Inflation Surprised On The Upside

Inflation beat expectations and higher prices were seen across the board. As we expected inflation has been a non-factor in the 1st half of 2014, but will increase moderately in the second half. We expect the Fed to be reactive, instead of pre-emptive, when it comes to inflation, which means the Fed’s tone will remain dovish until inflation becomes a real concern. Inflation at producers’ level seems to be trending moderately higher too.

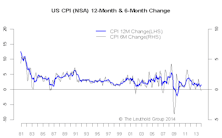

Inflation Beats Expectations Again

Inflation is at the highest level in the last nine months. Without wage inflation, it’s hard to see substantially higher inflation in the near future. Inflation will be a non-factor in the 1st half of 2014, but will increase moderately in the second half. Inflation at producers’ level seems to show some signs of revival.

Inflation Beats Expectations

Inflation increased and beat expectations. Capacity utilization increased more than expected too, a sign that the slack is being worked off. A much more persistent trend in wage inflation is necessary for a sustained inflationary environment and we are still not there yet. Inflation will be a non-factor in the 1st half of 2014. Inflation on the producers’ level is still well contained in a narrow range.

Inflation Still Modest

Inflation is still modest and in line with expectations. Hourly earnings rose, but wage inflation probably has to go much higher to make its impact felt. The U.S. has been importing disinflation from the rest of the world and the import prices reflect that. Inflation will be a non-factor in the 1st half of 2014. Inflation on the producers’ level is modest too despite the recent surge in Crude Materials PPI.

Inflation Pressure Anemic

Inflation is modest and broadly in line with expectations. Labor costs have stabilized, but the global disinflationary trend has not changed. We maintain our view that inflation will be a non-factor in the first half of 2014, but it might increase moderately in the second half. Inflation on the producers’ level is weak, too and the PPI inflation pipeline doesn’t seem to pose any immediate inflationary threat either.

Inflation Pressure Anemic

Inflation measures are broadly in line with expectations, and overall inflation pressure is anemic. We maintain our view that inflation will be a non-factor in the first half of 2014, and it might increase moderately in the second half. Inflation on the producers’ level is weak, too and the PPI inflation pipeline doesn’t seem to pose any immediate inflationary threat either.

Inflation - Still Missing

Inflation measures are going lower still, and the lack of inflation is one of the biggest hurdles for the Fed to start tapering. We maintain our view that inflation will be a non-factor for the next six months, but it will increase moderately in the following six months. We expect weakening inflation on the producers’ level too. Disinflation is consistent across various measures.

Inflation Lower Still

We maintain our view that inflation will be a non-factor for the next six months but will increase moderately in the following six months.

Inflation - Tilting Lower

Inflation measures are tilting lower. The Fed does not see the low inflation reading reverting to a more normal level any time soon. We maintain our view that inflation will be a non-factor for the next six months but will increase moderately in the following six months. Inflation on the producers’ level weakened too. We don’t anticipate a big rise in the near term.

Inflation - Still Going Nowhere

Inflation measures are anemic and mostly lower than expectations. We maintain our view that inflation will be a non-factor for the next six months but will increase moderately in the following six months. Inflation on the producers’ level to be modest too. We don’t see strong evidence for a big rise in the near term.

Near Term Measures Pointing Toward Lessening Of Inflation Pressures

Twelve month rates of change will not rise much from current levels through the rest of 2011.

CPI Expected To Decelerate

CPI inflation measured on a twelve month basis has probably peaked. Looking ahead, inflation should cool off in the first half of 2009 (+3%). Here’s why....

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue