Equity Strategies Group-Level Analysis Of The Equity Markets

The Growing Popularity of Sector Rotation

Too many institutions are playing the sector rotation game. Typical portfolio turnover has increased considerably, and popularity has rotated faster than the rotary engine in a Mazda RX7. For the last year or so, our own sector strategies have been undergoing a change, becoming increasingly narrow. This is a significantly different approach than the broad economic sector approach that is now so popular.

Gilt Edged Growth Vs. Cyclical

During May, cyclical stocks fell almost 10.5%, while our Gilt Edged Growth stock index fell 7.4%. Thus, again on a relative basis, growth was better. Momentum now clearly favors growth and we think growth stocks have regained the upper hand.

A Timing Move from Cyclical to “Gilt Edged Growth”

Last issue we discussed the strong possibility of this transition. Now we are pretty sure it has taken place. The equity model portfolio is adjusted accordingly, eliminating the remainder of our Super Cyclical holdings and building positions in “Gilt Edged Growth Stocks.” We have also constructed a new index by which to track and evaluate 25 of the best.

Updated Screens: High Growth, “Cheap” Growth and…..“Undervalued”

We have just updated three of our quantitatively screened sectors, “Consumer High Growth Stocks,” “The Growth Bargain Basket” and the “Undervalued & Unloved.” A great number of new stocks have qualified. This section describes the screens, presents the past performance and lists the additions and deletions for each.

High Tech Stocks

Our “High Tech Thirty” index on Feb. 23 was down 45% from the June 1983 peak. That, coincidentally was the target set by us in summer 1983. The worst might be over for these battered and beaten stocks. A few are starting to look interesting.

What About the Oils Now?

The last of the tactical “Oil Patch Recovery” play initiated in early 1983 has been closed out. What now? We expect oil stocks to be underperformers for at least six months. $25 crude prices would not be a surprise in 1984. And on a long-term basis, we still expect oil prices to erratically decline in real dollars for the rest of the century.

New Leadership from “Industrial Tech”?

Many high tech stocks have probably “had it” in terms of potential market leadership, especially the Office Tech stocks and Info Tech stocks. But we think Industrial Tech stocks have considerable potential. This “In Focus” feature explains why, reviewing market action of high tech stocks (including our High Tech Thirty Index).

Health Care Today and Tomorrow....And One Specific Investment Opportunity Area

In recent years health care stocks have developed a bad case of two tier-ism. Health care service issues have been hot numbers while more traditional health care issues, primarily the big ethical drug issues languished. From now on it may be the other way around.

“Let’s Get Competitive”: A Conceptual Investment Theme

Capital spending to improve manufacturing and industrial productivity may be much higher than anticipated over the next three years. Management confidence is growing, and attitudes are changing: “Yes, we can compete with our overseas rivals.” Here are the stocks and industries that should be the major beneficiaries of this projected development.

What’s New with Investment Concepts?

This update on our research presents three areas of potential interest and also explains why we don’t put much (if any) stock in the fast, coming into vogue “demographic plays.”

Up with The OiIs

We have increased our Oil Patch holdings by 5%, now 14% of Equity Portfolio assets. The recent spot oil price trends now seem to confirm our preliminary conclusion that crude price declines are over…..at least for a while.

Cyclical Stocks May Be Better Than Growth Stocks

During March, the cyclicals outperformed the growth stocks. Growth stocks were clearly superior from mid-1981 through November 1982. But since December, momentum has shifted in favor of the cyclicals. The long-term trend appears to have reversed in favor of the cyclicals.

Consumer Growth Stocks

The new computer screen produces 49 candidates for purchase and a new quantitative evaluation formula tells us “buy the numbers” which are “best.” Two of these “best” were added to model portfolio this issue, Walgreen and Alberto Culver.

Productivity Plays – A New Look

This conceptual area, even though now widely recognized, still looks attractive. We may soon again be increasing holdings here from current 10% levels. With this issue, we have refined our approach, separating Science & Technology Productivity Plays from Non-Science & Technology. The S&T components may be most attractive. A new index is introduced to track this segment more closely.

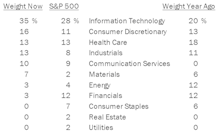

Financials Improve; Commodities Tumble

While it was a small jump, from #6 to #5 in the sector composite ranks, Financials might be seeing the start of overall improvement. Conversely, Materials and Energy continued to drop in the latest ratings, as fundamental measures deteriorated.

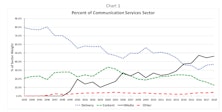

A Prehistory Of The Communication Services Sector

The new GICS Communication Services sector being introduced late-September will include members that add considerable buoyancy to the growth rates and valuation ratios of this traditionally defensive, high yield, slow growth industry. As a newly-invented sector, Communication Services has no financial history, and we felt it was important to fill that void.

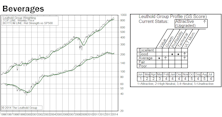

Current Attractive & Unattractive Groups and Highlights

Beverages, Tobacco, Department Stores, and Diversified Banks.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue