Sentiment

Odds & Ends

Here are some brief follow-up notes on topics covered in recent months’ Green Books.

Are You Really A Contrarian?

The need to sound contrarian has become a borderline obsession among market pundits. Media opportunities for talking heads have exploded in the last decade, forcing those who hold the safest consensus views to falsely portray themselves as lonely and misunderstood market mavericks.

Leuthold Quick Takes: Getting Sentimental

This issue of Leuthold Quick Takes reviews the conflicted nature of investor sentiment as seen by Doug Ramsey (Chief Investment Officer) and Jim Paulsen (Chief Investment Strategist).

Building The Wall?

One of the more impressive feats that bullish pundits have pulled off is their successful portrayal of themselves as lonely and misunderstand contrarians even as the eleventh year of a cyclical bull market grinds on.

1999 Redux

As the market rebound has extended, we’ve noted its striking similarities with the rally of 1999—one that might have been the most speculative in U.S. history.

You Call That A Panic?

Christmas Eve came not with snowfall but a market freefall which was the worst-ever recorded for that date.

Market Observations

.jpg?fit=fillmax&w=222&bg=FFFFFF)

It’s been one of the worst years on record for diversification, with our hypothetical All Asset No Authority (AANA) portfolio down 7.2% YTD through yesterday. That’s the second-worst year for AANA since 1972, and there’s probably not enough time left for performance to undercut 2008 (-24.9%) for the bottom spot.

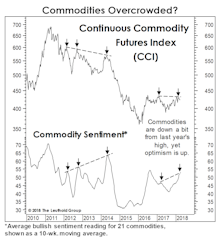

Time To Get Contrary With Commodities?

After a strong 2016 and a “Bridesmaid” (i.e., sector runner-up) performance in 2017, the Materials sector seemed primed to benefit from the “late cycle” character of the economy in 2018.

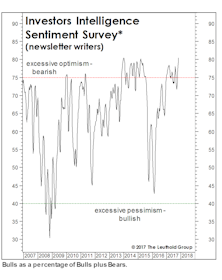

Investor Temperament And The “Tape”

In the first week of October, the share of newsletter bulls topped 61% just as the NYSE percentage slid to 41%. Maybe it’s a seasonal thing… the last time that happened was October 2007.

A Troublesome Commodity Pattern...

During each of the last five months, the U.S. economy has shown a broadening array of “late-cycle” characteristics.

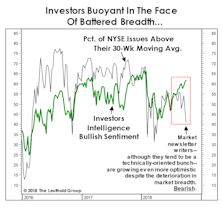

“What, Me Worry?”

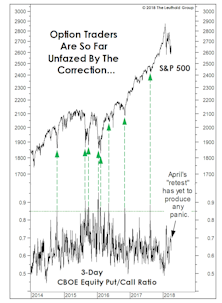

Our shortest-term put/call measure has yet to reflect the level of fear usually triggered by a correction of this size. Meanwhile, the market setback has done almost nothing to stymy the optimism of either market newsletter writers or mutual fund timers.

A Long-Term Take On Sentiment

We impatiently published this study two months ago instead of properly waiting for full-year numbers.

A Long-Term Take On Sentiment

Tax cuts, a strong economy, and daily stock market records have lifted measures of investor sentiment to levels not seen in two decades. But sentiment is only a slightly better timing tool than valuations (which is not saying much), and there’s plenty of room for excitement to build before a final top is at hand.

Not A Tipping Point, But A “Toggle” Point?

Evidently, being a bull in a bull market is no longer good enough.

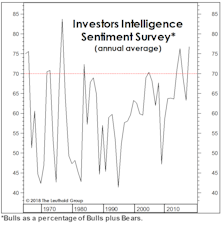

A Longer-Term Take On Sentiment

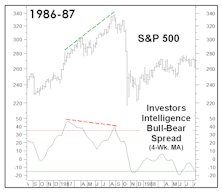

Stock market bears had a field day when the latest Investors Intelligence sentiment survey (Chart 1) saw the percentage of bullish newsletter writers spike to its “highest level since 1987.”

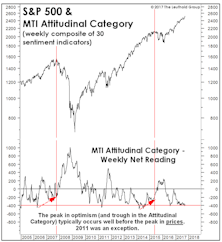

Thoughts On Sentiment

The MTI’s Attitudinal category has held stable over the last several months, an impressive (and contrarily bullish) feat considering the steady onslaught of new bull market highs.

A “Good Year” To Start The Year

The S&P 500 was up 6.4% YTD through March 3rd, a bit above its average annualized gain of 5.9% since 1926. In other words, 2017 would be a good year if the books were closed today.

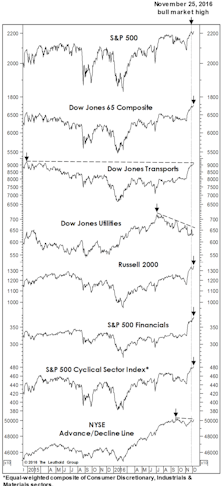

Stock Market Observations

We revisit our “Red Flag Indicator” of prior bull market tops versus today. Usually most of these internal market measures will deteriorate in advance of the final bull market peak. At the latest S&P high, three of the seven leading measures had raised Red Flags, by not confirming, but two of them (DJ Transports and the NYSE A/D Line), are within just ticks of new bull market highs.

Bond Bubble Spills Into Equities

The S&P 500 once again remains on the verge of a new bull market high, thanks in large part to the bubble in another asset class: Bonds.

EM: Improved Sentiment But Macro Risks Still Dominate

Positive forces may be transient. Be wary of EM’s high correlation to commodities and Chinese stocks.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue