Normalized P/E

Small Caps: A New Ratio!

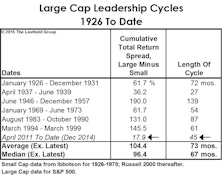

Small Caps lagged the S&P 500 by almost ten percentage points in 2014, but their underperformance streak technically dates back to April 2011. Nonetheless, their cumulative, 45-month underperformance in relation to the S&P 500 (now about –18%) is still modest enough that any mention of the current “Large Cap Leadership Cycle” is bound to draw a few head scratches.

High Quality Cycle In Force; Ideas For High Quality Energy Stocks

In early October 2014, we noted the momentum reversal of Low Quality stocks and a few signs of the likelihood of transitioning to another phase of the quality cycle. The official numbers of Q4 have confirmed this.

U.S. Versus Foreign Stocks: More Of The Same

Long before the U.S. dollar began to rebound, the current bull market in global stocks had already favored “provincial” portfolio managers focusing solely on U.S. stocks.

Small Cap Premium Finally Shrinks—But Remains Historically Extreme

July’s Russell 2000 -6% rout finally deflated some of the Small Cap valuation premium we’ve been grousing about in recent years.

How Long Can Small Caps Lead?

The Russell 2000 is about five points ahead of Large Caps YTD, and is approaching its April 2011 long-term relative peak. We view this outperformance as their leadership’s last gasp and not a new cycle.

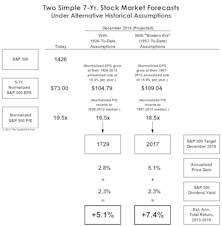

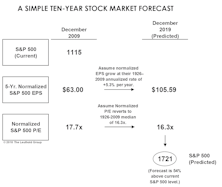

A Peak At The Rear-View Mirror!

We’ve lately made it a January tradition to publish a “Rear View Mirror” forecast for S&P 500 returns out to the end of this decade.

Leuthold Stock Quality Rankings: Starting To Favor Low Quality

Our Stock Quality Ranking work currently shows stocks with low quality rankings outperforming those with high quality rankings.

Major Trend Index Fading As “That Time Of Year” Looms

With “That Time Of Year” approaching and the Major Trend Index not too far above the neutral zone, we review nine factors impacting the stock market from a glass-half-empty perspective.

Stay Bullish

It’s April once again… Are we due for yet another market top? Some perspectives on the possibility of attaining a new all-time market high in the current cyclical bull, and what may drive the upside.

Leuthold Stock Quality Rankings

Leuthold Stock Quality Ranking work is currently showing that High Quality stocks outperformed during 2011. More upside for High Quality stocks going into 2012?

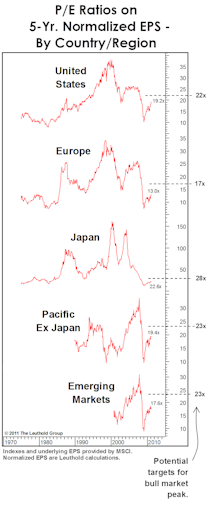

Valuations: The Good And The Bad

S&P Normalized valuations are already in the zone that have defined many important bull market tops.

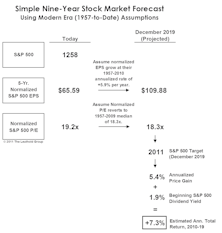

2011 In 2019?

Year-ahead stock market forecasts are now in hot demand, but of course are notoriously off the mark most years. Very long term forecasts (say, out to the end of the decade) are in virtually no demand, but are considerably easier to get close to the mark for those armed with the right tools.

A “Quality” Opportunity?

Low quality stocks led out of the past bear market, as typically occurs. Despite being the clear winners from the 2009 lows, it looks like the lower quality stocks can continue to outperform given current valuations and momentum.

Quick Takes From The Valuation Dashboard

Stock market valuations no longer cheap, but they are also not yet truly expensive. Eric Bjorgen isolates several valuation measures to show just where they rank historically

Our Outlook For 2019 (...2010 To Come Later)

While most are content to make annual predictions at this time, leave it to Doug Ramsey to bite off an even bigger piece…predicting the next DECADE.

U.S. Stocks: What If The New Decade Is “Normal”?

While most are content to make annual predictions at this time, leave it to Doug Ramsey to bite off an even bigger piece…predicting the next DECADE.

Valuation Constraints?

There is a potential valuation ceiling confronting U.S. stocks. 2002 S&P valuation lows may be the point that this cyclical bull market tops out.

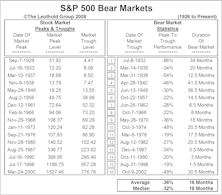

The Beginning Of The End.....Yes, We’re Talking About The Bear Market

September was a horrible month for the stock market, but now is not the time to be selling stocks. We believe a market bottom is close at hand, and this month’s “Inside The Stock Market” section presents several of our “big picture”, historical market studies to provide support for this belief.

What If We Don't Bottom Around Median Levels?

While we continue to believe in our market bottoming thesis, we thought it may be useful to examine those periods when the P/E ratios continued to fall to the 10x to 12x earnings levels.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue