Earnings

Signs Of Improving Earnings & Sales

Growth Is Re-emerging: A recurring theme in recent Leuthold Group research is the apparent turn in corporate profits and a general improvement in business results. To monitor corporate sales/earnings trends, we measure the number of companies reporting higher quarterly sales and earnings than a year ago, versus companies reporting lower sales and earnings.

An Earnings Bottom...What's Next?

It seems like it’s been ages since investors have been able to get excited about earnings growth, although our October 21st “Chart of the Week” showed that the S&P 500’s current earnings slump has been unremarkable in both depth and duration.

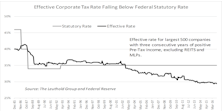

Impact Of Lower Corporate Tax Rate

A stock market wild card in 2017 is the potential for a significant reduction in the corporate tax rate. President-elect Trump’s desire to lower corporate taxes, if implemented, would have multifaceted impacts on businesses.

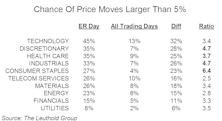

Calendar Effect On Earnings-Release Day Price Movement

Earnings season is not only important for fundamental investors, it can be equally so for quant managers. For quants that incorporate fundamental data, like us, historical trends and changes in consensus estimates may weigh heavily on model output.

Earnings-Release Price Movement Among Sectors/Industries

Earnings season is not only important for fundamental investors, it can be equally so for quant managers. For quants that incorporate fundamental data, like us, historical trends and changes in consensus estimates may weigh heavily on model output.

Four Thousand Companies Can’t Be Wrong!

Scott Opsal’s “Chart of the Week” in mid-October suggested the seven-quarter S&P 500 earnings recession may have run its course.

EPS Touching Bottom?

Early in the third quarter earnings season, S&P 500 companies are providing a glimmer of hope that the long earnings recession may be ending.

Inflation Remains Largely In Line With Expectations

The latest jobs report disappointed but we think it’s a short term aberration as other data still point to a healthy job market. Some of the key market-based inflation drivers, however, have reversed course a bit in the last couple weeks. Patience is still the right strategy.

Taking Earnings At Face Value

We’ve said before that one of Wall Street’s great inventions is the “forward operating earnings” estimate for the S&P 500, because it results in a P/E ratio that invariably sounds reasonable (if not outright cheap). But this already-misleading EPS metric has become even more so in recent years because of the proliferation of non-GAAP “adjusted EPS” reporting practices.

Inflation Exceeded Expectations In April

Inflation exceeded expectations in April. The more durable inflation measures such as wage inflation are also improving. We characterize the recent improvement in inflation as a relief from the threat of deflation but still quite far from being a catalyst for run-away inflation.

Inflation-Patience Recommended

Inflation missed expectations in March. The three key inflation drivers this year - oil, the Dollar and the Chinese yuan, are all going in the right direction. The risk of being too early on the inflation call far outweighs the risk of being too late. Patience is still recommended.

Earnings Momentum

The final month of 2015 earnings reports registered an Up/Down Ratio of 1.07. Once again, we have to go back to the dark days of 2009 to find a lower “three-month” ratio.

Inflation Modestly Exceeds Expectations

Inflation met or modestly exceeded expectations. The three key drivers for inflation (oil, the Dollar and the Chinese yuan) continued to improve. But we are not rushing to declare victory on disinflation. “Organic” inflation, such as sustained wage inflation, has been very elusive so far.

Earnings Momentum

The second month of Q4 2015 earnings reports registered an Up/Down Ratio of 1.12—up from the post- financial crisis low of 1.11 last quarter. With 51% of the observations in February, the “Up” count edged out the “Down,” but barely.

Momentum Trouble

Momentum reversed in February, primarily due to rallying Materials stocks. Value and Profitability both performed well.

Knee Deep In An Earnings Recession

It’s a scary thought but what does 2015 have in common with the infamous years of 2001, 2008, and 2009? An earnings recession for the S&P 500 — and the 2015 vintage certainly has some unique traits.

Earnings Momentum

The second month of Q3 2015 earnings reports registered an Up/Down Ratio of 1.11. On its own, the month of November was particularly weak with a stand-alone Up/Down Ratio of 0.97.

Earnings Momentum

Up/Down Earnings: Worst Start In Six Years

Earnings Momentum

The third and final month of Q2 earnings reports registered an Up/Down Ratio of 1.18. This is the second lowest “three month” reading of the past 23 quarters.

Earnings: What Is Normal?

Corporate profits are notoriously cyclical, and for decades we’ve sought to temper their swings by using a five-year smoothing of S&P 500 EPS in our valuation work.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue