Breadth

Stock Market Breadth: So Good We’re Suspicious

Market breadth measures have been so strong since the February low that we wonder whether something might be wrong with them.

Stock Market Observations

Commentators now label this cyclical advance the “seven-year bull market,” but that won’t be semantically true until the S&P 500 closes above its May 2015 peak of 2130.82.

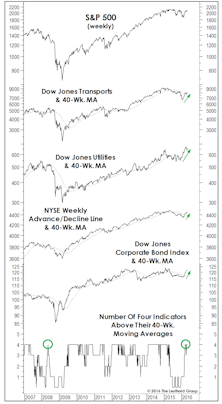

“Four On The Floor”

Leadership, breadth, and corporate credit all staged intermediate-term breakouts, rising above their respective 40-week moving averages. In this formation, historically, S&P 500 annualized return is +15%.

Sizing Up The Rally

While our MTI became bullish in mid-April, we can’t rule out that the rebound from February lows could be an impressive bear market rally. However, this rally sports impressive technical credentials.

“Top In” Or “Topping Out?”

The stock market rally has carried far enough to flip some of our trend-following work bullish, lifting the Major Trend Index to a low-neutral reading. The improvement prompted an increase in asset allocation portfolios’ net equity exposure to 42% (up from 36% previously).

On High Alert

August is “National Eye Exam Month,” but this is the rare year we can confidently recommend that you skip it.

Stock Market Observations

The U.S. stock market has largely shrugged off the latest round of worries related to China’s stock market collapse, the new down-leg in crude oil, a more hawkish tone in Fed-speak, and sizable second-quarter declines in S&P 500 sales and earnings.

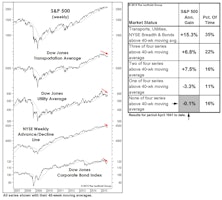

Weakening Foundation

Over the last few months, we’ve presented a couple of simple quantitative studies meant to encapsulate the factors driving our Major Trend Index to the brink of bear territory. The chart and table might provide the best summary yet.

Fed Watching For The 21st Century

Deteriorating stock market breadth and worrisome leadership trends both suggest liquidity has already tightened; whether the Fed follows suit in September may now be just a formality.

Two Takes On Market Breadth

Market technicians continue to argue that a bull market peak is unlikely to form with the majority of U.S. stocks (and global ones, for that matter) still participating in the new highs of the blue chip indexes.

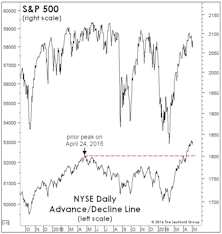

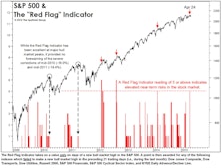

Flying By Instruments

The safest highs to sell in the stock market are “lonely” new highs. Fortunately, the April 24th bull market high in the S&P 500 was anything but, as that index enjoyed a varied swath of Large Cap, Small Cap, and foreign company (although the DJIA was a mysterious no-show).

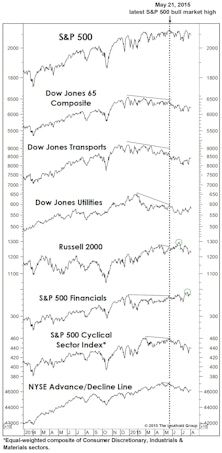

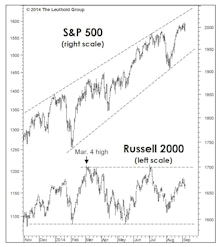

Two Takes On The Ticker Tape

Conventional breadth measures show the U.S. market to be healthy, with key indexes confirming the April 24th S&P 500 high. However, sector leadership is behaving in a way that’s consistent with an approaching market top.

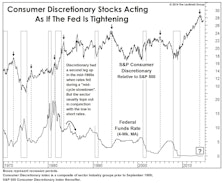

What The Market Tells Us About Fed Policy

Poor performance in 2014 by two typical victims of Fed tightening—Consumer Discretionary and Small Caps—corroborated our argument that “tapering” is tightening.

Elevated Short-Term Risks

The S&P 500 and NASDAQ Composite moved to new bull market highs in early September, but our quantitative work continues to warn there’s a least a short-term speed bump ahead for the stock market.

Market Breadth And Leadership

While the lagging action of Small Caps should be monitored, persistent strength in most stock market breadth measures makes it difficult to argue the stock market has entered a true “distribution” phase.

Stock Market Valuation Check

Stocks might look superficially cheap relative to bond yields, but they continue to offer little appeal in an “absolute” valuation sense.

Why We Think Tapering Is Tightening

We believe the first move toward tighter policy occurred in January when the Fed first reduced the rate of its monthly bond purchases by $10 billion to $75 billion.

Premature Inflation Fears

With commodity prices falling in recent months and consumer prices in the Eurozone almost flat over the latest 12 months, we’re surprised that inflation fears continue to climb the list of U.S. investor worries.

Share Buybacks: They’re Not For Everyone...

Share repurchase activity in the S&P 500 dropped off in the second quarter, after first quarter buybacks challenged the all-time high levels seen in the second and third quarters of 2007 (a window of history that should ring a bell).

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue