Breadth

The Market Is On Fire… Unless It’s Ice

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Yesterday’s S&P 500 new all-time high triggered a few simple internal studies we’ve used to help shape second-half expectations for the stock market.

Are New Lows The Key To New Highs?

Last year’s market decline was one of the largest to have occurred without a lengthy-preceding period in which breadth narrowed and Small Caps significantly underperformed.

A High-Risk Rally

During the market bounce over the last few weeks, we reminded ourselves and others of the old maxim that “bear market rallies look better than the real thing.” Evidently, the stock market overheard us and took the advice as marching orders.

Odds Of Outperforming?

In September, the percentage of S&P 500 stocks outperforming the S&P 500 index fell to 40.7%, the lowest reading since mid-2012. Breadth has followed a conventional path over the course of this unconventional bull market; in the current phase, the odds of outperformance are steadily diminishing.

Investor Temperament And The “Tape”

In the first week of October, the share of newsletter bulls topped 61% just as the NYSE percentage slid to 41%. Maybe it’s a seasonal thing… the last time that happened was October 2007.

Technical Difficulties

Traditional breadth measures have yet to show end-of-cycle thinning of the ranks, but some secondary measures suggest that process may be underway.

A Market Breadth Mystery

It’s difficult to knock a stock market in which Small Caps and major breadth measures are making frequent new highs, however, there are performance anomalies that suggest liquidity is no longer sufficient to “float all boats.” Recent underperformance of the Equal Weighted S&P 500 is a case in point, at the same time, the current dichotomy in market breadth pales in comparison to the 1999-2000 episode.

The Bulls And Bears Agree!

Yes, bulls and bears now hold their respective positions for the same reason—i.e., the U.S. economy is exceptionally strong. The stock market is accommodating this rare bipartisanship with sufficient reason to support either position.

Is Market Breadth Misleading?

The stock market has narrowed, but not in the way we envisioned—nor in a way that’s consistent with most historical bull market tops. Small Caps and market breadth measures are traditionally the first to wilt when monetary tightening begins to hit the stock market. Instead, they are the leaders.

Breadth Is Great— Except Where It Matters The Most

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Last week’s piece challenged the now popular view that new highs for the Russell 2000 are a decisively bullish factor for the stock market in the near term. To our surprise, we found that market returns during periods of well-defined Small Cap leadership are significantly lower than when Smalls are laggards.

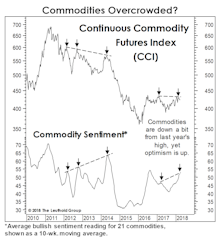

A Troublesome Commodity Pattern...

During each of the last five months, the U.S. economy has shown a broadening array of “late-cycle” characteristics.

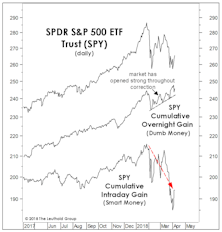

Assessing The Selling

While the January 26th bull market high illustrated none of the hallmarks of a major cyclical top, there are secondary signs that a stealthy distribution process may be underway, such as an overwhelming bias toward opening market strength followed by intraday weakness.

Most Likely Just A Correction

So, what happened to the January Barometer—the old analyst’s maxim that a market gain in January portends a gain for the full year?

Seasonality And Market Breadth

While the FANGs—and, lately, the Dow stocks—are the market’s undisputed leaders, it’s difficult to argue the market has narrowed in a fashion that’s indicative of a “distribution” phase.

Stock Market Observations

We remain bullish on stocks but with very limited visibility into 2018.

Market Breadth Has Yet To “Lie” Down

We shouldn’t bite the hand that feeds us, but it’s easy to lie with charts.

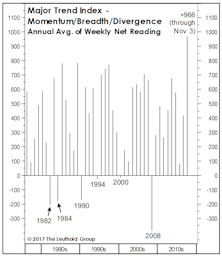

Bonds, Breadth, And Leadership: A Simple Model

Hard-core statisticians might be disappointed to learn that the 140-ish inputs in our Major Trend Index (MTI)aren’t entirely “independent and uncorrelated.”

Stock Market Observations

Second-half results showed the U.S. emerging from the 2015-2016 profit recession, and our early read is that the first quarter should show more of the same.

Stock Market Observations

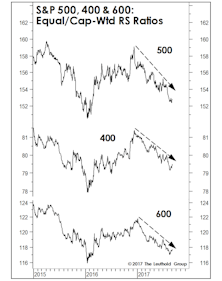

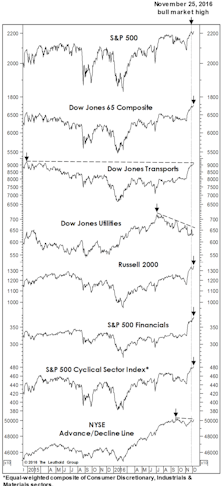

We revisit our “Red Flag Indicator” of prior bull market tops versus today. Usually most of these internal market measures will deteriorate in advance of the final bull market peak. At the latest S&P high, three of the seven leading measures had raised Red Flags, by not confirming, but two of them (DJ Transports and the NYSE A/D Line), are within just ticks of new bull market highs.

Charts: Beware Of Myopia

Despite a two-month stall in the blue chips, the breadth and momentum behind the market’s rally off mid-February lows remain hard to deny.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue