Quantitative Strategies

Factor Performance: Insider Activity Finally Works; Value Continues To Struggle

Insider Activity measures finally additive in July after six months of negative results; other factors’ performance deteriorated, however.

June 2011 Factor Performance

The month of June brought more of the same, with profitability, size and momentum continuing to work reasonably well.

Factor Performance Since 2009 Lows: Reversals Everywhere

Graphical representation of the difficulty since the March 2009 market bottom. Not many factors have been effective.

April Factor Performance: Talk About Boring

Very little to show for a month of solid market performance. Breaking the market down by capitalization yields some interesting results.

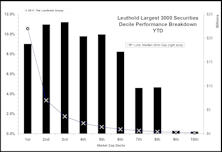

Dow Performance: A Matter Of Weighting...

Are the Dow Industrials benefiting from trivial weighting? Slicing our Leuthold 3000 universe into market cap deciles shows different performance results than commonly followed market indices.

Correlations: Still At Peak Levels

Our calculations show the rise and fall of equity group correlations over time. How does this impact returns both historically and going forward?

March Performance: Factors Continue To Lack Consistency… Except For Momentum

Momentum once again has the best performance. This out-of-favor factor has continued to outperform the rest of the factors.

February Performance: Month Ends On A Whimper

During February, the only quantitative factor producing positive performance was Momentum. All other factors produced negative returns.

Digging Deeper With Group Level Data

This month’s “Quantitative Strategies” section presents a preliminary look at some long term trends in Valuations and Profit Margins for specific industry groups.

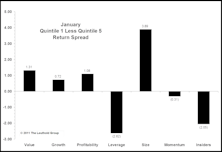

January Performance: Quality and Size Take The Lead...Finally

Quantitative Factor review for January shows Large Caps, Quality, and Profitability factors finally performing well. It’s been over a year since stocks with better Profitability outperformed in an up S&P month.

Earnings Revisions Stay Positive For Now

Quant implications for earnings revisions. Revisions tend to follow actual earnings, not lead them. Better economy now producing upside surprises, which has good short term implications.

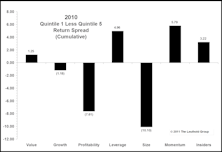

Year In Review: Inconsistency Among Traditional Factors

Factor performance during 2010: A review of traditional quantitative factors and their performance for the year.

Two Quant Themes With Significant Implications For 2011

Two Quant Themes With Significant Implications For 2011. We revisit studies from the past year that focused on Revenue Growth vs. Earnings Growth, as well as Momentum vs. Value.

Market Action Signals Further Room To The Upside

Factor analysis shows that Momentum continued to be effective in November. Also, aggressive equity sectors have been outperforming the defensive ones. Both of these factors bode well for a continuation of the bull market.

The Impact Of Quantitative Easing On Style Factors

Chun Wang examines QE I & II in Japan, along with the initial QE in the U.S., to see how various quantitative factors have reacted in the past. While some factors may prove effective, the main difference between these past QE experience and the latest round is the macro conditions of the market.

Year To Date Update: Momentum Makes A Comeback

YTD the winner is momentum! This is slowly developing to the angst of many model-tweekers. Note though that how one defines momentum can make a difference in what you see.

Commodities vs. Style Factors: A Risk Perspective

Chun Wang uses the CRB Index as a risk proxy to test the effectiveness of a range of quantitative factors in various environments. Commodity prices have become an increasingly important measure of risk, since higher commodity prices indicate a greater risk appetite and vice versa.

Revisiting Value & Momentum: Sign Of A Top?

Relationship of Momentum stocks and Value stocks has historically demonstrated that at market tops, Momentum does best while Value lags. That pattern is occurring now, but based on prior history the top would not come until Q1 2011.

Month In Review: The Quality Trade Returns

Quantitative factor performance throws yet another curve ball. Momentum works with Growth and Profitability for first time this year.

Market Correlation And Group Rotation Strategy

New data series confirms unprecedented correlations in equity markets.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue