Quantitative Strategies

Growth Remains Undefeated

What can slowdown the outperformance of Growth stocks? It turns out, the answer to that persistently-unanswerable question is “Not much.” Not even a global pandemic-driven sell-off and swift rebound. From the market high in February through June 30th, Growth handily outperformed every other factor.

Valuation Dispersions At Extremes

Valuation dispersions remain at extreme levels. Dispersions within Large Cap stocks remain above Tech Bubble levels, but are on par with Mid and Small Cap stocks on an absolute basis. Spreads within sectors also present historic stock selection opportunities.

Factor Performance: Value Crushed

The selloff has served to amplify secular style-trends that were in place going into this debacle. Large Cap Growth has continued to outperform everything else, with the underperformance of Value stocks accelerating alongside market losses.

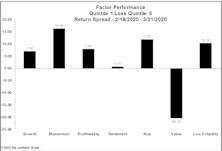

Factor Performance During Sell-Off: Momentum Dominates

Momentum made up for a lackluster 2019 by providing protection during the volatile market correction, while Value continued to be punished. Momentum remains expensive relative to its long-term history, while Value remains cheap, but neither is outside levels seen in recent years.

Tesla: A Short Story

The common, and easy reason given for the recent Tesla move is a short squeeze. We don’t deny that existing shorts are getting “squeezed,” but that’s a result, not a cause, of the recent move. The more likely instigator is speculator FOMO (Fear Of Missing Out).

The Factor Of The Decade Is... Sales Stability?

During a decade characterized by surging equity markets and the proliferation of smart beta products, the best performing quantitative factor was Sales Stability, which isn’t usually associated with either of those trends.

The State Of Momentum

Going forward, high Momentum will depend on an unlikely combination of Information Technology and low Volatility, while low Momentum continues to have outsized exposure to Energy and Materials. Recent weakness only moderately tempered valuations, which could be a headwind.

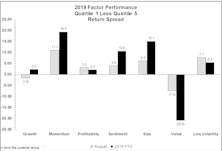

Factor Performance: Momentum Saves The Day (Year); Value Is Awful

Momentum has made a furious comeback after a rough start to the year, posting an +11% spread in both May and August. Value continues to get crushed and there has been nowhere to hide: The pain is equally distributed between cheap and expensive, and it’s happening in every sector.

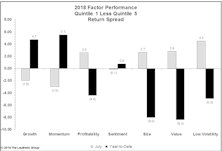

Factor Performance: Has Anything Changed In 2019?

· From a factor performance standpoint, 2019 is looking a lot like 2018, with expensive Momentum names outperforming everything else and Value struggling.

Momentum Negative In Q4, But Positive For 2018

2018 was frustrating for most investors as Value continued to struggle and positive Momentum performance was difficult to capture. Small Caps, Mid Caps, and ADRs also underperformed.

What’s In Momentum Now?

Along with market volatility, the composition of Momentum has changed, becoming more defensive and less exposed to cyclicals and commodities.

October Factor Performance

Most factor categories reversed performance along with the market in October. During the month, Value had solid results while Growth gave up all of its 2018 gains. Profitability also had a nice bounce-back month.

Price Hasn't Mattered

While Momentum continues to work overall, the gains have been skewed to the companies trading at the highest valuation multiples. Extremes, based on both price and valuation, have only been greater a handful of times during the period measured.

Value Turns Positive

Value finally performed well during July, turning in its best month of 2018 on a spread basis. While the factor category is still deep in negative territory for the year, almost 85% of its underperformance is coming from the worst quintile outperforming the universe; meaning Value has mostly struggled because of expensive stocks outperforming, not cheap stocks lagging.

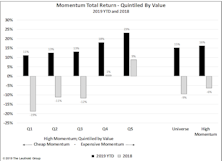

Narrow Momentum Performance Hard To Capture

While Momentum has worked very well during the last year, the best performance has been concentrated among the most expensive securities within the high Momentum group.

Has The Makeup Of Momentum Changed?

The makeup of Momentum has stayed surprisingly steady through the volatility in 2018, with Info Tech and Health Care maintaining overexposure. Energy is sneaking in, though, and could be poised to take a much larger share.

Growth Continues To Crush Value

Value can’t catch a break. Even a bounce in oil can’t jumpstart the traditionally value-oriented Energy sector. We’ve been sticking to our late bull-market thesis that Growth will outperform, but as we see signs that gains may be limited (or non-existent) going forward, a shift to Value could be in the making.

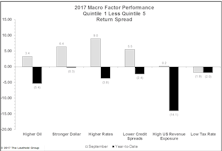

2017 Factor Performance

2017 was a great year for factor performance. We track seven factor categories and Value was the only one to produce a negative return spread.

Tax Reform Hits Factor-Land

Apparently tax reform wasn’t priced in.

Macro Factors Reassert Themselves

There will be occasions when the macro influences are reasserted, which happened in September.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue