Macro Monitor

2015 Time Cycle—Giving The Bull The Benefit Of The Doubt?

We are again impressed by the pattern’s predictive ability as most equity markets tracked their respective patterns quite well in 2014. Another banner year seems to be in store for the S&P 500. The exceptionally favorable pre-election year is the main reason, but we cannot be too complacent.

Risk Aversion Index—New Higher Risk Signal

Despite strong performance for stocks, the RAI ended the year at its highest level. While we are in a very favorable seasonal window, we recommend taking a more defensive stance for now.

U.S. 10-Year - All About Inflation

The collapse in oil prices has brought down inflation expectations dramatically. Inflation will likely be the single most important driver of interest rates in the next 6-12 months.

QE Success Limited - A Transmission Channel Check

Perhaps the most important is the credit channel; the substantial curve flattening that happened recently in anticipation of the Fed hike next year has made lending standards tighter for small businesses.

Risk Aversion Index Stays On “Lower Risk” Signal

Continued strength in equities offsets the weakness in credits and commodities to arrive at an essentially flat reading.

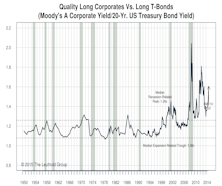

U.S. Investment Grade Corporates: Favorable

Record issuance and oil-related weakness combined to drive the spreads wider but we remain Favorable on these bonds for now.

Interest Rates Range Bound—Can’t Be Too Bearish

The sell-off in risky assets in early October promptly led to expectations of a more dovish Fed.

Risk Aversion Index Fell Sharply—New “Lower Risk” Signal

The dramatic turn-around in risk appetite triggered a new “Lower Risk” signal. It also marks the beginning of a very favorable seasonal window.

Interest Rates & Currencies: It’s Complicated

The recent sudden strength in the dollar is mostly attributable to the divergent central bank policies. This supports a bullish dollar outlook over the medium term.

Mid-Term Election – Favorable For Stocks

General patterns are a weaker dollar, rising stocks and range-bound bond yields.

Risk Aversion Index—Moved Up Again, Stayed On Higher Risk Signal

The hawkish Fed and various geopolitical risks weigh on market sentiment, so caution is highly recommended.

U.S. Bonds

U.S. Quality Corporate Bonds & Munis Rated Favorable; High Yield Bonds Rated Neutral.

Current State Of Stock-Bond Relationship = “Easing”

We define four states of the stock-bond relationship based on the directions of stock price and bond yield movements; stocks fear tightening more than true risks, while bonds are more responsive to Risk-On and Risk-Off.

Risk Aversion Index—Ticked Lower, Still On Higher Risk Signal

New ECB stimulus should support risky assets near term but caution is warranted.

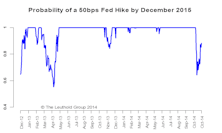

Yield Curve Too Flat? Short Term Maybe, Longer Term Probably Not.

With the Fed policy approaching actual tightening, the market is trying to price in a rate hike in the next year or so. This is a rather typical market response.

A Year Before Tightening - Stocks Will Be Fine

We studied the five previous initial rate hikes and present the average pattern over the one year period prior to these events.

Risk Aversion Index Ticked Up - Still On “Higher Risk” Signal

There have been several cases in the last couple years where credit and/or currency risk-off events never affected equities. We will soon find out if this is just another one of those. Caution is recommended.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue