Macro Monitor

All Crowded Trades Are Vulnerable—Even The Yield-Curve Flattener

Bond market volatility picked up quite a bit in May but the higher-low/higher-high pattern in the 10-year yield is still intact, indicating the primary uptrend has not reversed.

Risk Aversion Index: Stayed On “Higher Risk” Signal

Volatility among non-equity asset classes has gone up noticeably while the VIX dipped lower. We still expect volatility to stay high and continue to play defense within fixed income.

Risk Aversion Index: Stayed On “Higher Risk” Signal

We expect volatility to stay high and still recommend defensive positions within fixed income.

Rates & Credit At A Major Crossroads—A Few Things To Watch

April saw a valiant attempt by the U.S. 10-year yield to crack the upper band of the multi-decade downtrend channel (around 3.0%-3.05%).

Trade War & Libor—More Bark Than Bite?

Isn’t a trade war more bark than bite? We think a full-blown trade war may be eventually negotiated away but the process is not necessarily painless to investors.

U.S. Investment Grade Corporate Bonds: Maintain Neutral

Our overall view toward credit has turned decidedly cautious over the last couple months and that includes our long-term favorite.

Risk Aversion Index: Stayed On “Higher Risk” Signal

While concerns about a trade war might be easing and the credit market has been largely unaffected by the surge in Libor rates, we have to recognize the fact that Trump’s policy focus has become increasingly market-unfriendly while global central banks are in a liquidity-reducing mode.

U.S. Rates: Looking For A Dip

The U.S. 10-year ended the month 15 bps higher but non-U.S. bonds fared much better with bond yields in Europe and Japan 4-5 bps lower.

More On The Dollar Bear Market

A potential trade war (not quite there yet) is not good for the dollar as it will inevitably invite retaliation and sour sentiment toward dollar assets.

Risk Aversion Index: A New “Higher Risk” Signal

While the late rebound in risky assets pared back earlier losses, weakness was observed in all major risk asset classes. We continue to recommend defense for the time being.

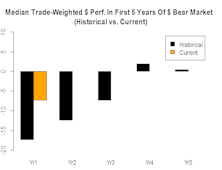

Anatomy Of A Dollar Bear Market

With the dollar index breaking below the 2017 low, we believe the dollar bull market that started in 2011 (based on the trade-weighted dollar index) is most likely over.

Risk Aversion Index: Turned Higher But Stayed On The “Lower Risk” Signal

Our Risk Aversion Index turned higher last month but stayed on the “Lower Risk” signal as of the end of January. The first few days of February brought a big surge in this index and would suggest a “Higher Risk” stance for the near term.

Four Divergences—A Steepening Correction

While we still believe flattening is the more likely scenario over the medium term, we do feel the recent flattening move is a bit overdone and there are several divergences that suggest a short-term steepening correction is in store.

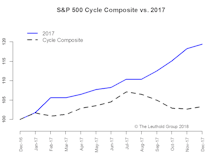

2018 Time Cycle—Beware A Fall Correction

The most common 2018 time-cycle pattern among major markets is a fall correction, with the U.S. and Japan faring better than their European counterparts.

Risk Aversion Index: New “Lower Risk” Signal

Our Risk Aversion Index turned lower in December and reached an all-time low. We remain favorable toward higher quality credit within fixed income.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue