Inside The Stock Market ...trends, cross-currents, and outlook

NASDAQ Now, Financials Next?

We wouldn't be surprised if the S&P 500 Financials require a recovery period just as long as NASDAQ's.

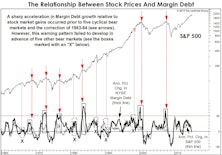

Margin Debt Revisited

Stock market Margin Debt enjoyed a brief phase of notoriety when it eclipsed its 2007 high just over a year ago, then it retreated into obscurity. Now it may finally be telling us something.

A Quick Check On Global Fundamentals

The Street’s most clever invention is “12-month forward operating earnings” because the stock market invariably appears cheap on the basis of such inflated estimates.

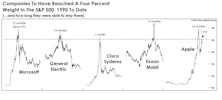

Apple: Back In The Club!

While we own Apple stock across all of our quantitative long equity strategies, we’ll admit to having mixed feelings when the company shot up to an S&P 500 index weighting of just over four percent last month (4.04%).

Losing Our Voice

In a cyclical bull market as long and strong as the current one, it’s certainly possible the topping process will be proportionally lengthy and deceptive.

2015 Leadership: An Early Take

Last year’s economically defensive winners held their grip on stock market leadership in January. This action is consistent with our view that the bull market is an aged, overvalued one that has begun a final “distribution” process that will eventually erupt into a cyclical bear.

Early Thoughts On The Next Bear

We expect a “garden variety” cyclical bear market to break out this year or early next year and present a chart demonstrating the potential path of decline. In the context of the last two decades’ market action, a decline of this variety does not “look” all that significant.

Millions Of Citizens Become “One-Percenters…”

While the collapse of Swiss government bond yields into negative territory was January’s bond market stunner, our “G7” composite 10-year government bond yield reached its own milestone when it closed the month below 1.0% for the first time in post-WWII history.

Capex, Capacity And The Dollar

We’ve been highlighting the overinvestment (or malinvestment) risks in commodity-oriented equity sectors for the past three years, but we certainly did not foresee those risks exploding the way they have in the oil market over the last seven months.

Topping Out… But Patience Required

Weight of the evidence suggests the bull market is in a broad topping process, likely begun in late-July. The duration, however, may be proportionate to the tremendous five-plus year upswing that preceded it.

Sentiment: Frothier Than You Think

Last year will certainly go down as the bull market year in which investors were finally retrained (as they usually are, late in every bull market) to buy the dips. Most of our Attitudinal measures—ranging from option activity and bear fund assets, to surveys of investor sentiment—show retail investors finally shaking off the worry that gripped them for most of the bull market’s first five years.

2015: An “Anomaly?”

We’ve written periodically about the Presidential Election Cycle in relation to stock prices, sheepishly acknowledging both the persistence of the pre-election year effect and its pervasiveness across many markets

Two For The Price Of One?

Think the bull market is long in the tooth at almost six years of age? Maybe not.

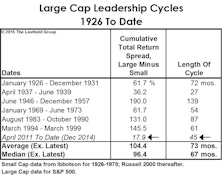

Small Caps: A New Ratio!

Small Caps lagged the S&P 500 by almost ten percentage points in 2014, but their underperformance streak technically dates back to April 2011. Nonetheless, their cumulative, 45-month underperformance in relation to the S&P 500 (now about –18%) is still modest enough that any mention of the current “Large Cap Leadership Cycle” is bound to draw a few head scratches.

A Good Year For Leuthold Industry Group Scores

Last year was a solid one for the Group Selection (GS) Score approach, with the Attractive list delivering a total return of +13.1%—more than 500 basis points above The Leuthold Group Universe average, which gained only +7.9%.

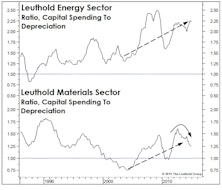

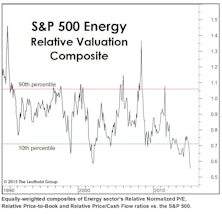

Thoughts On Energy

The recent Energy sector decline has accomplished the feat of wiping out all of the upside gains achieved during its “Third Act” played out in the 2006-2008 surge.

Industry Group Dreams And Nightmares

For more than a quarter century, The Leuthold Group has tracked hypothetical industry group portfolios composed of the previous year’s “Dreams” (best performers) and “Nightmares” (worst performers). The former is a gauge of a simple, trend-following investment strategy, while the latter is a crude form of industry group “bottom-fishing.” Sticking with tradition, the following pages detail how the 2013 Dream and Nightmare portfolios faired in 2014, and we reveal which industries qualify in the Dream and Nightmare portfolios of 2014.

High Quality Cycle In Force; Ideas For High Quality Energy Stocks

In early October 2014, we noted the momentum reversal of Low Quality stocks and a few signs of the likelihood of transitioning to another phase of the quality cycle. The official numbers of Q4 have confirmed this.

Perception for the Professional

May 2026 Issue

Featured Articles

Sector Navigator

May 2026 Issue