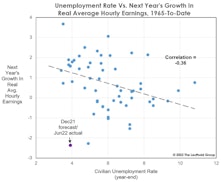

Wages

Labor: Snatching Defeat From The Jaws Of Victory

This year it’s been popular to say the Fed will hike interest rates until it “breaks something.” Has that not already happened? Pull up charts of the Japanese yen, the British pound, and the euro, among others. And stateside, the Fed has broken one of economists’ favorite toys: the Phillips Curve.

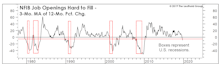

Lagging From Behind?

As Yogi Berra might have quipped, it’s not just the leading indicators that are lagging… the lagging ones are, too.

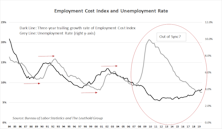

Labor Cost Observations

We take a look at different data sets reflecting labor costs. The main finding is that using Unit Labor Cost as the measurement for the true cost suggests that the labor market is very tight in terms of affordability for businesses.

Margins Prove Capitalism Still Works

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Corporate profits were outstanding last year, but even the benefit of a 40% cut in the top income-tax rate wasn’t enough to lift the net profit margin back to the all-time high of 10.6% established in early 2012. Still, the latest 10.0% figure is more than a percentage point above the 2007 cycle high and about two points better than any other cycle high.

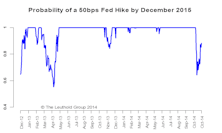

Interest Rates Range Bound—Can’t Be Too Bearish

The sell-off in risky assets in early October promptly led to expectations of a more dovish Fed.

Second Half 2007: Inflation Acceleration Expected

CPI inflation accelerated again in March. As we see it, the important development is that inflation has broadened out.

Inflation Outlook: Worrisome

CPI and PPI monthly inflation kicked up a bit with February readings and could do so again when March results are released.

Inflation Still A Potential Threat

Inflation trends are a mixed bag at present.

Inflation Trends Are A Mixed Bag

Twelve month rates of change for both CPI and PPI have been trending down over the past fifteen months, and seem to be less of an immediate threat. But, the Core CPI seems to be in an uptrend.

Inflation Is A Potential Threat

Inflation prospects are especially unclear. While many inflation gauges seem to be slowing, the threat of an inflation flare-up remains.

Inflation Still A Potential Threat

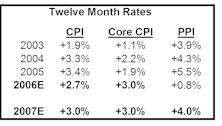

Looking ahead, CPI twelve month rate of inflation is likely to be in the +2% area for the first half of 2007.

Inflation Concerns

Inflation expectations seem to be on the rise.

Inflation Watch

CPI on a twelve month basis still expected to decelerate over the next three months. The final 3 months of the year, however could be another story, with CPI twelve month inflation accelerating.

Inflation Watch

Major reason for lower inflation forecasts is expectation of slowing economy (recession?) in 2006.

The Consumer: Still Chugging Along

Consumer spending may have finally peaked in this cycle, but a consumer collapse is far from imminent. Consumers can be expected to remain supportive of economic growth.

Inflation Watch

After a brief dip, project twelve month CPI to accelerate to about +3.8% by year end.

Inflation Watch

We continue to be more optimistic about the dollar than most, and believe the post election U.S. dollar weakness was overdone.

Inflation Watch: 2005 Outlook

Further U.S. dollar weakness could certainly be an inflation negative (higher import prices), but we are more optimistic about the dollar than most.

Inflation Watch: 2005 Outlook

For now the economic expansion remains healthy, but could fade some in the second half of the year.

2005 Outlook: High Energy Prices Will Show Up In Next CPI & PPI Reports

We estimate +3.3% real GDP growth in 2005, after weakening in the second half of the year.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue