Value

2013 Factor Performance Review

2013 ended up being a good year for quantitative strategies, particularly those that focus on using Momentum

Growth/Value/Cyclicals Market Internals

Growth Stocks Lead YTD In All Three Cap Categories.

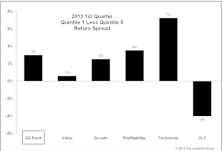

2013 Factor Performance: What Worked? What Will Keep Working?

Momentum and Value worked in 2013. Materials and Financials were the easiest sectors to exploit; Discretionary and Tech the most difficult. Momentum works in December; Value and Small Caps at the start of the year.

Large Cap Growth Bounces Back The Past Two Months

Growth stocks are now all above their historical average valuation levels. Value stocks are all solidly overvalued compared to their recorded averages.

Growth Continues Leading In Mid And Small Caps YTD, Large Cap Growth Bounces Back

All three cap tiers of Growth also now ahead for the YTD. Growth stocks are moving towards their his- torical average valuation levels, with Mid Cap Growth now being overvalued. All Value stock segments continue to be solidly overvalued.

Growth Continues Leading In Mid And Small Caps YTD But Lags In Large Caps

Growth’s leadership over Value has only been apparent in Large Caps, but this segment had a big short-term reversal in recent months. Large Cap Cyclicals (+7%) significantly lag Large Cap Growth (+17%) YTD.

Duration: It’s Not Just For Bonds Anymore

We measure the sensitivity of common stocks to changes in interest rates using Implied Equity Duration. Growth-oriented sectors tend to have higher duration than Value-oriented sectors, while regional differences are largely explained by interest rate and risk premium differentials.

Growth Leads In Mid And Small Caps But Lags In Large Caps

Growth’s longer term trend of leadership over Value has only been apparent in Large Caps, but this segment had a big short-term reversal in Q2 and July.

Q1 Review of Group Selection (GS) Scores

After a recent rough patch due to a multitude of factors (macro driven markets, high correlations, etc.), our domestic Group Selection (GS) Scores started seeing more consistent performance during the fall of 2012. This continued through the first quarter of this year, with the Attractive to Unattractive return spread at +3.0% year-to-date.

Correlations And Factor Performance

Value factor performance took off at the end of June last year and never looked back; posting positive Q1 minus Q5 spreads every month since.

Value Vs. Momentum Performance

We see a strong and clear Poor-Value/Strong-Momentum pattern emerging, which could indicate a looming market top. While QE3 could disrupt it, the pattern looks unmistakable.

A Closer Look At Growth And Value Return Differences

Traditional Fama/French analysis shows an exceptionally large 4% per annum return edge favoring Value. Based on Russell 1000 Growth and Value Indexes, however, the edge in favor of Value has been a fraction of that. Current year’s Growth outperformance is also dissected to determine the likelihood this leadership will persist.

The Return Of Value And Growth?

Correlations finally drop during the October market rally. Both Value and Growth factors outperformed during the month. Some momentum factors have diverged… each is an atypical occurrence.

Two Quant Themes With Significant Implications For 2011

Two Quant Themes With Significant Implications For 2011. We revisit studies from the past year that focused on Revenue Growth vs. Earnings Growth, as well as Momentum vs. Value.

Year To Date Update: Momentum Makes A Comeback

YTD the winner is momentum! This is slowly developing to the angst of many model-tweekers. Note though that how one defines momentum can make a difference in what you see.

Revisiting Value & Momentum: Sign Of A Top?

Relationship of Momentum stocks and Value stocks has historically demonstrated that at market tops, Momentum does best while Value lags. That pattern is occurring now, but based on prior history the top would not come until Q1 2011.

Go Back To Basics During An Economic Slowdown: Value & Quality

Given the discussion during August of a weakening economy and a potential double dip, Chun Wang looks at which of our quantitative factors do best during a slowdown.

Popularity, Agreement, And Trust: A Global Perspective Of Investor Preference

Analysts are playing an increasingly important role in today’s market. In this section, we focus on the market’s interpretation of three characteristics related to analysts estimates: Popularity, Agreement, and Trust.

The Value Of Value Investing: A Global Perspective

As one of the oldest investment philosophies, value investing has certainly stood the test of time. The recent market meltdown is no exception.

Stock Market Cheap! ...According To NIPA Profits

Based on NIPA Corporate Profits, the S&P 500 is now relatively cheap based on the prior 1956 to date history.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue