Value

Factor Chaos

The November 9th Pfizer vaccine news compressed an entire Momentum reversal into one historic day. Factor performance easily broke records looking back over our entire history of data. While great news for the general public, it was awful news for Momentum indicators.

Research Preview: Rotating Away From Growth

This study examines Value, Small Cap, and Emerging Markets to see if they do, in fact, behave in a correlated manner when viewed as alternatives to Large Growth. The goal is to determine whether this trio of rotational favorites can be considered as broadly-equivalent replacements for LG.

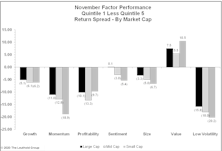

Momentum’s Terrible, Horrible, No Good, Very Bad Day!

.jpg?fit=fillmax&w=222&bg=FFFFFF)

If Momentum and Growth investors thought they were escaping 2020 unscathed, they learned otherwise on Monday. Pfizer’s promising news about a COVID-19 vaccine was met with universal excitement and investors rearranging portfolios—taking gains in long-term winners and plowing into beaten-down cyclical stocks.

VLT’s Struggles Are Telling Us Something

Our Very Long Term (VLT) Momentum algorithm has been a very good “confirmatory” market tool over the years, especially at the onset of a new cyclical bull market. But VLT has proven to be of little to no value in navigating this year’s gyrations. VLT’s latest flip-flops reinforce our view that the market leaderboard is set to be rearranged.

Election—Another Chance For Value

.jpg?fit=fillmax&w=222&bg=FFFFFF)

As we Chinese watch the elegant display of the western democratic process this election season, we can’t help but think there are indeed people less fortunate than us “commies.” Worse yet, some of these people are Value investors.

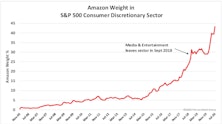

Consumer Discretionary: Neither Fish Nor Fowl

The combination of rebounding economic activity and a surging (peaking?) enchantment with mega cap growth stocks is pressing investors to make an important tactical call: whether to take profits in some highfliers and shift assets to sectors with more cyclical exposure and better valuations.

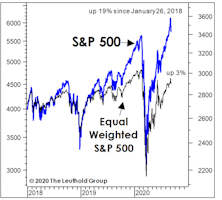

Back To The Brink

Despite equal-weighted measures’ long-time underperformance, all valuation ratios we monitor for the median S&P 500 stock have returned to their top historical deciles. Even worse, our new equally-weighted “Valuation Composite,” based on these measures, closed August at a 98th percentile reading.

Research Preview: Not Your Parents’ “Discretionary”

The combination of rebounding economic activity and a surging enchantment with mega-cap growth stocks is pressing investors to make an important tactical call: whether or not to exit some highfliers and shift assets to sectors with more cyclical exposure.

Profiting From Mighty Mites

One of the signature traits of the U.S. small cap market is the prevalence of money losing companies. A recent tally indicated that prior to Covid, 38% of small caps were reporting trailing year losses despite the widespread economic strength of 2019.

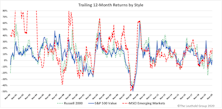

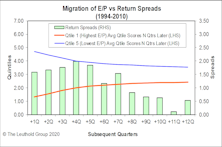

Why Value Failed—Top-Down & Bottom-Up Views

From a top-down view, since 2003, Value’s performance has been much more closely tied to various asset markets and macro drivers. From a bottom-up perspective, we believe the change in Value’s migration behavior might be the key to its failure. We believe macro tailwinds and positive surprises are both necessary for a true Value revival.

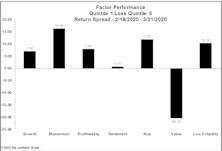

Factor Performance: Value Crushed

The selloff has served to amplify secular style-trends that were in place going into this debacle. Large Cap Growth has continued to outperform everything else, with the underperformance of Value stocks accelerating alongside market losses.

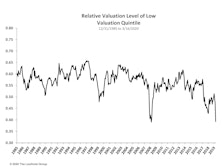

Valuation Dispersions Reach 2009 Levels

The recent market turmoil has only served to exacerbate equity style trends that have been in place for years, with Value, Small Caps, and High Beta all underperforming relative to Growth / Momentum, Large Cap, and Low Volatility, respectively.

The King Is Dead: A Global Chartbook

Last year we published a report titled Price to Book: The King is Dead (available on the Leuthold Research website) with the objective to better understand the decade-long struggle of the value style. Our findings showed that indexes based on the Price to Book ratio have indeed lagged since 2007 but that other measures of value performed significantly better until just recently.

The Case Of The Flipping Factors

Equity market themes have been boringly consistent of late; growth beating value, large beating small, and domestic beating international. In the factor world, Momentum and Low Volatility have been investor favorites for most of 2019 while Value resided in last place – the same old, same old. Then, something remarkable occurred on September 9th.

Horse Trading In The Factor Zoo

Smart beta ETFs have become an immensely popular investment tool, attracting billions of dollars in AUM by providing investors with targeted exposure to factors such as Value, Momentum and Quality. Characteristics such as these have been shown to generate alpha over time, and investors understandably wish to have focused positions in these return-generating styles.

Factor Performance: Momentum Saves The Day (Year); Value Is Awful

Momentum has made a furious comeback after a rough start to the year, posting an +11% spread in both May and August. Value continues to get crushed and there has been nowhere to hide: The pain is equally distributed between cheap and expensive, and it’s happening in every sector.

Value Turns Positive

Value finally performed well during July, turning in its best month of 2018 on a spread basis. While the factor category is still deep in negative territory for the year, almost 85% of its underperformance is coming from the worst quintile outperforming the universe; meaning Value has mostly struggled because of expensive stocks outperforming, not cheap stocks lagging.

Value Style’s 100-Year Flood

Value is the philosophical cornerstone of many legendary portfolio managers and is widely recognized as one of the most robust quantitative investment factors. Yet, despite its compelling conceptual merits and long-term record of superior returns, recent years’ underperformance of Value has lasted long enough to weigh on even 10-year performance records.

Muster Drill: To The Value Lifeboats

.jpg?fit=fillmax&w=222&bg=FFFFFF)

While we’re not calling for an imminent market top, we are keeping a diligent watch from the crow’s nest for signs of a coming market correction.

Bridesmaid Strategy: Low P/E Sector: Annual Results

Table 5 shows annual performance results for the Cheapest Sector strategy under all four rebalancing frequencies, along with the lowest P/E sector for the annual version of the strategy.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue