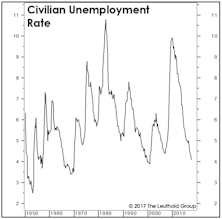

Unemployment

Assessing The Cyclical Risks

With all the excitement over the Fed’s shift in rhetoric and the excellent subsequent market action, there’s a danger of losing sight of the broader cyclical backdrop for U.S. stocks. Remember, the economy is still operating beyond government estimates of its full-employment potential, and it’s not as if the Fed has actually eased policy—as it did successfully at a similar late-cycle juncture in the fall of 1998 and (ultimately unsuccessfully) in the summer of 2007.

Too Soon To Expect Economic Weakness?

We believe stocks have begun to discount a major inflection point in the economy and corporate profits for 2019 and 2020.

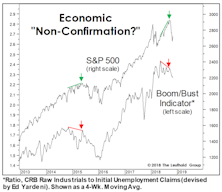

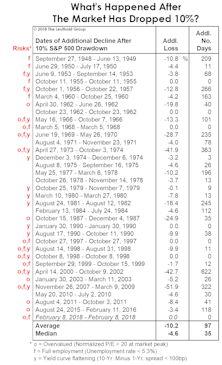

Assessing The Correction

How do today’s cyclical conditions stack up with those accompanying other stock market declines?

Inflation Warning Flags?

After yet another benign figure on wages for June, the idea that inflationary pressures might be a problem for the stock market seems far-fetched.

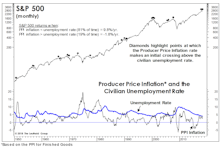

Full Employment And Rising Prices Aren’t Stock-Friendly

.jpg?fit=fillmax&w=222&bg=FFFFFF)

Annual Producer Price Inflation rose to 4.0% in May, a key threshold above which the S&P 500 has historically delivered essentially flat returns. But the fact that this reading occurs against a backdrop of full employment is cause for even more concern. Context is key...

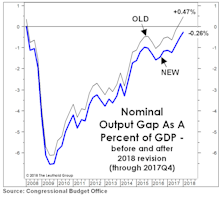

The Gap Is Back!

We celebrated the official closure of the GDP Output Gap in December, but that milestone was revised away in April by the statisticians at the CBO through a downward adjustment to the estimated rate of “full employment.”

The “Gap” Is Gone. Now What?

In Q3, the CBO’s Nominal Output Gap swung to positive for the first time since the last business cycle peak. This type of move has historically meant the cyclical peak in profit margins is close at hand.

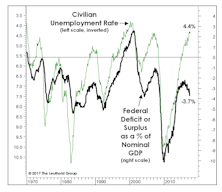

Tax Reform Or Not, The Budget Is Already Busted

In 2010 and 2011, we were sometimes chastised for not paying more attention to exploding federal deficits, which at the time were running between 8% to 10% of GDP. We argued that a substantial share of these budget shortfalls was cyclical in nature, and would eventually be reversed by an improving economy.

Two Curves, One Theme

Our data shows the traditional Phillips Curve relationship between the unemployment rate and wage inflation still holds.

Don’t Look Now, But...

We recognize it’s uncultured to discuss federal debt and deficits during a multi-year bull market, but in economics and investing it frequently pays to worry when others don’t, and to stop worrying when others do.

A New Take On The Labor Market

Politicians bemoan the lack of “good-paying jobs,” but what’s the current perspective of employers? According to a simple measure developed by economist Edward Renshaw many decades ago, employers see a lack of “unused labor capacity” in the U.S. that should lead to yet another year of disappointing GDP growth in 2017.

How Much Slack?

By now it’s consensus that the Fed missed the ideal window for the first rate hike (if one ever existed) by at least a year and a half. We don’t disagree…

Navigating The First Rate Hike

Our current view is the lift-off will be December or later. Assuming inflation will pick up and the Fed hikes the rate by the end of 2015, stocks will perform relatively well, with international stocks a better bet than U.S. stocks.

The Economy In 2014: Solid But Unspectacular

This year should be a solid but unspectacular one for the U.S. economy, with real GDP growth of about +2.5%. We expect the Consumer Price Index to rise just 1.5%. Unemployment should continue to fall.

Global Yield Curve Confirms “Muddle Through” View

The global yield curve is in a sideways range bound pattern, indicating anemic demand for credit. An examination of developed and emerging countries confirms our “muddle through” view.

“Just Another” Soft Patch

MTI studies of market values, investor psychology and price action have (so far) overwhelmed the economic “elephants in the room.” A few thoughts on those elephants.

Deciphering The Real Message In The Employment Figures

It’s a big mistake to react to the headline reports of employment, and an even bigger mistake to make investment decisions based on them.

Update On Non-Farm Payrolls....Buy Signal Likely With November Data

Non-farm payroll data is poised to register a buy signal for the stock market in early December. Using the year over year rate of change has historically been very effective in identifying recession-related market bottoms.

Employment Data Continues To Deteriorate

At the risk of beating the “we’re in a recession” theme into the ground, we thought some analysis of the hot-off-the-presses March employment data would be worthwhile.

Jobs/Consumer Data Flashing Recessionary Signals

Optimists have continuously cited low unemployment and the ever resilient U.S. consumer as two “pillars of strength” that will help keep the economy afloat. It has become considerably more difficult to make this case in recent months, as jobs and spending data have weakened to levels associated with recessions.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue