Total Returns

Revisiting The Y2K Highs

Bobby Knight thought coaching would be perfect “if it weren’t for those damned games.”

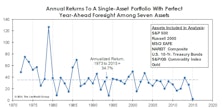

How To Double Your Money In Ten Years

Before the markets punish an irresponsible act, they must first reward it.

Spoiler Alert! The Bond Bear Is Already Here...

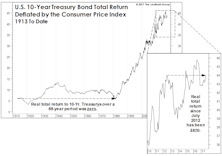

Bond investors residing in the Lower For Longer© camp no doubt feel vindicated by the summer rally that’s taken yields on 10-year Treasury bonds to as low as 2.06% in early September.

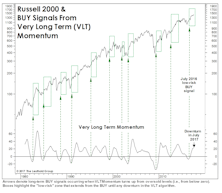

VLT Goes “Quiet”

Last year’s “low-risk” BUY signals from our Very Long Term (VLT) Momentum algorithm have proven very profitable, but enough time has elapsed that they should no longer be considered an important bullish factor.

How To (Almost) Double Your Money In Under Ten Years

Buying the S&P 500 on one of the worst possible days in history ultimately yielded a total return of +87.4% (+6.8% annualized) through the end of April 2017...darn, sounds like an advert for Vanguard!

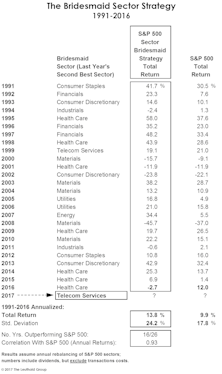

Bridesmaid Sector Track Record

Table 4 shows the annual sector selection and accompanying performance results for the Bridesmaid approach dating back to 1991.

Bridesmaid Track Record

U.S. 10-Year Treasury Bonds—last year’s Bridesmaid holding—eked out a 1% gain in 2016, a disappointing result but one that preserved a streak of positive annual returns dating back to 2001 (Table 2).

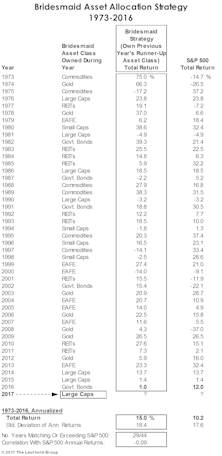

Asset Allocation: Buy Strength Or Weakness?

The turn of the calendar seems to bring out the inner contrarian in some investors—those who will peruse last year’s list of lagging asset classes looking for rebound candidates.

Real Bond Returns: Set To Flatline?

While a plunge into a recession could always result in a final “blow-off” phase to the 35-year secular bull market in bonds, any youthful, long-term buyer of 10-Year Treasurys should weigh that exciting possibility against the odds that bonds do no more than match the inflation rate over the next 30-50 years.

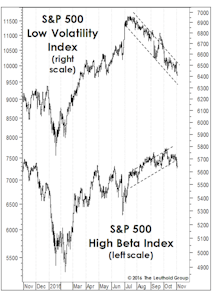

The “Low Vol” Unwind: Just The Beginning?

In mid-summer we suggested that attaining new market highs would probably require a rotation away from the long-time Low Volatility market leaders and into High Beta areas like Technology and industrial cyclicals.

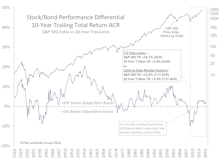

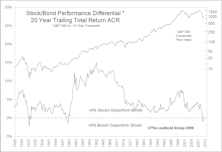

A Stock/Bond Relationship Revisited

Herein we further explore this month’s theme of “point-in-time relationships” and subsequent market returns. We review and update a study we initially conducted and published in June 2009.

Foreign Stocks Set For A New “Bear”-ing?

Based on comparative valuations alone, one could have made a case for investing in foreign stocks over domestic ones as early as 2010—when EAFE’s valuations sunk to an historical low, relative to the S&P 500. Today, that gap remains extreme.

Asset Allocation: No Upside In 2015

Hedge funds have shuttered by the dozen in the past few weeks, with the worst carnage among those focused on Emerging Markets and commodities. But the problem is broader.

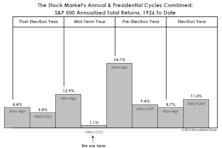

The Worst Of The “Window” Is Upon Us

Three months ago, our “Of Special Interest” section reviewed the historically pronounced effect of the well-known “Sell In May” phenomenon during mid-term years of the presidential election cycle.

Small/Mid/Large Caps

Small Cap Premium Continues Upward To 23%. Large Caps Lead On The Downside In January

Small/Mid/Large Caps

Small Cap Premium Continues Upward To 21%. The red-hot equity market of 2013 was especially good for Small Caps with a +38.8% total return.

Risk Premium for Stocks Making a Comeback…

Andy Engel revisits our Stock/Bond Performance Differential study which examines rolling stock/bond spreads over various time periods and subsequent asset class returns. It appears that trends are finally reverting slowly toward the norm.

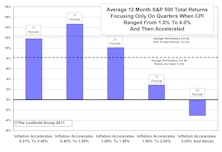

Accelerating Inflation And Stock Returns

Periods of accelerating inflation generally lead to lagging stock market performance.

Current Deflation Fears Are Unwarranted

Don’t fear deflation. Leuthold historical studies show mild deflation can actually be a good environment for the stock market.

Update On Our Stock/Bond Performance In Focus Special Study

Despite strong stock market returns relative to 10-year Treasuries, the “generational anomalies” still exist. Stocks should outperform bonds going forward.

Perception for the Professional

March 2026 Issue

Featured Articles

Sector Navigator

March 2026 Issue